Catalysts

About PATRIZIA

PATRIZIA is an investment manager focused on real estate and infrastructure across smart real assets for institutional clients.

What are the underlying business or industry changes driving this perspective?

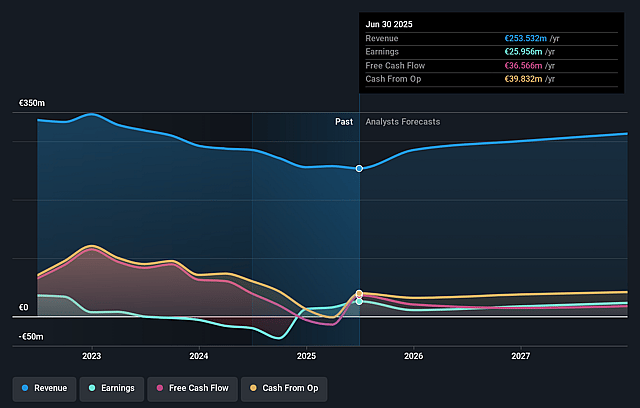

- The integrated real estate and infrastructure platform, with management fees already more than covering total operating expenses and EBITDA margin at 22.1%, positions PATRIZIA to convert any future AUM growth more directly into EBITDA and earnings.

- Client capital is clearly rotating toward energy transition and digital infrastructure, and PATRIZIA is already active here with assets such as the Nordic district heating platform of over €300 million and data center exposure, which can support higher management fees and potentially more stable revenue streams.

- Long-term demand for modern living assets, including affordable housing, student housing, co living, micro living and senior living, aligns with PATRIZIA’s 40 year focus on the sector and can support fee bearing AUM growth and higher recurring revenues.

- Rising equity raising momentum, with €0.8 billion raised in 9 months and a higher quarterly run rate in Q3 plus €1.1 billion of open equity commitments, points to a stronger pipeline of future investments that can feed through into management fees and co investment earnings.

- Cost efficiency measures are already visible in a materially lower cost base and improved EBITDA, and management still sees room for further efficiencies, which can support EBITDA margin and net margins even if market driven fees such as performance and transaction fees remain volatile.

Assumptions

This narrative explores a more optimistic perspective on PATRIZIA compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

- The bullish analysts are assuming PATRIZIA's revenue will grow by 3.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 15.1% today to 9.9% in 3 years time.

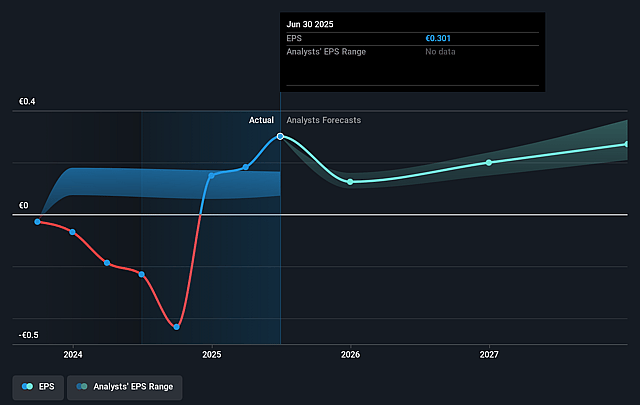

- The bullish analysts expect earnings to reach €28.5 million (and earnings per share of €0.34) by about January 2029, down from €39.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €17.2 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 65.8x on those 2029 earnings, up from 18.9x today. This future PE is greater than the current PE for the GB Real Estate industry at 10.6x.

- The bullish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.5%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The company’s focus on real estate and infrastructure means it is tied to a cycle that management itself describes as slower, tougher and bumpier than previous ones. If client risk appetite remains subdued and fixed income continues to attract capital, equity raising and transaction activity could fall short of expectations, which would pressure fee based revenue and delay earnings growth.

- The more optimistic long term AUM ambition of €100b is described as a North Star that is reassessed every year. Recent guidance for 2025 AUM has already shifted down to a €56b to €60b range, so if market momentum, revaluations and client demand do not materialise as hoped, the gap to that aspiration could remain wide, limiting operating leverage and earnings.

- Management fees currently more than cover operating expenses, helped by cost efficiency measures and one off catch up fees of about €2.5m in the third quarter. If further cost cuts are harder to realise and temporary items roll off while market driven fees such as performance and transaction fees stay under pressure, EBITDA margin and net margins could come under strain.

- The business model relies on balance sheet co investments and seed investments, including rental income from owned assets of roughly €12m this year and exposure to platforms such as Dawonia and the Nordic district heating investment. If disposal timing, asset values or rental performance do not support recycling of capital as planned, this could weigh on future earnings, liquidity and the quality of recurring income.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for PATRIZIA is €12.2, which represents up to two standard deviations above the consensus price target of €10.46. This valuation is based on what can be assumed as the expectations of PATRIZIA's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €12.2, and the most bearish reporting a price target of just €8.2.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be €288.0 million, earnings will come to €28.5 million, and it would be trading on a PE ratio of 65.8x, assuming you use a discount rate of 7.5%.

- Given the current share price of €8.5, the analyst price target of €12.2 is 30.3% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on PATRIZIA?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.