Last Update 07 Jun 26

CNXC: Margin Expansion And Buybacks Will Support Repriced Upside Potential

Analysts have reduced their price targets on Concentrix by $12 to $25, citing updated views on the company’s outlook. They maintained their fair value estimates and kept key model inputs such as discount rate, revenue growth, profit margin, and future P/E broadly unchanged.

Analyst Commentary

Recent research reports show a cluster of price target cuts on Concentrix, with reductions in the range of $12 to $25. While headline targets moved lower, the underlying commentary points to a mix of confidence in the core business and caution around execution and valuation.

Bullish Takeaways

- Bullish analysts kept key valuation inputs such as discount rate and P/E assumptions broadly unchanged, which signals that they still view the long term earnings profile as intact even with lower price targets.

- The decision to maintain revenue growth and profit margin assumptions suggests confidence that the business model can continue to generate the cash flows currently embedded in their models.

- By reducing targets but not fair value estimates, bullish analysts appear to be accounting for nearer term uncertainty while still seeing the stock as broadly aligned with their long run valuation work.

- The tightening of price targets without major model changes can be read as a recalibration of expectations rather than a fundamental reset of how the business is expected to perform.

Bearish Takeaways

- Bearish analysts cutting targets by as much as $24 to $25 highlight concerns around the company’s ability to execute cleanly against prior expectations, even if headline model inputs stay the same.

- The size of the target reductions indicates that some analysts see a wider gap between current market pricing and what they are comfortable underwriting on execution and visibility.

- Keeping discount rates unchanged while lowering targets points to a view that risk is more about company specific delivery and less about broad market or macro drivers.

- With revenue growth and margins left broadly intact in models, these lower targets imply more conservative views on what investors might be willing to pay for the stock versus prior P/E multiples.

What's in the News

- Q1 2026 earnings transcript highlights that Concentrix is focusing on winning what it describes as the right business, shifting its revenue mix, and using AI powered solutions, including its proprietary iX suite, as a core part of its offering. (Source: Concentrix Q1 2026 Earnings Transcript, 2 Jun 2026)

- The company reports that Q1 2026 revenue and profitability were in line with guidance, while also taking steps to manage debt and invest in growth initiatives. (Source: Concentrix Q1 2026 Earnings Transcript, 2 Jun 2026)

- Management indicates an expectation of sequential margin expansion for the remainder of 2026, supported by cost reduction actions, revenue growth, and scaling of transformational deals. (Source: Concentrix Q1 2026 Earnings Transcript, 2 Jun 2026)

- From 1 Dec 2025 to 28 Feb 2026, Concentrix repurchased 1,000,000 shares, representing 1.62% of shares, for US$42m, completing a total buyback of 8,431,613 shares, or 13.91%, for US$556.18m under the program announced on 27 Sep 2021. (Source: Company buyback update)

- Concentrix issued unaudited guidance for Q2 2026 and full year 2026, with expected Q2 reported revenue between US$2.460b and US$2.485b and operating income between US$128m and US$138m, and full year reported revenue between US$10.035b and US$10.180b with operating income between US$636m and US$686m. (Source: Company guidance)

Valuation Changes

- Fair Value: Held steady at $41.25 with no change in the underlying fair value estimate.

- Discount Rate: Unchanged at 12.46%, indicating the same required return is being applied in the valuation work.

- Revenue Growth: Adjusted only fractionally, from 2.28% to 2.28%, effectively keeping the long term growth outlook the same in the model.

- Net Profit Margin: Tweaked slightly, from 16.03% to 16.03%, signaling a virtually unchanged profitability assumption.

- Future P/E: Left effectively unchanged at 1.89x, suggesting no material revision to the multiple applied to future earnings in the model.

Key Takeaways

- Integrating AI solutions and iX Hello products is expected to drive revenue growth and earnings by enhancing client offerings and operational efficiency.

- The Webhelp acquisition synergies, capital allocation, and share repurchases aim to improve margins and EPS, supporting profitability and shareholder returns.

- Concentrix's growth and profitability are at risk due to modest revenue growth, integration challenges, currency risks, high debt, and client concentration issues.

Catalysts

About Concentrix- Designs, builds, and runs integrated customer experience (CX) solutions worldwide.

- Concentrix is focusing on integrating AI solutions across its operations and client offerings, which is expected to drive revenue growth as it becomes a trusted provider for AI solutions in the market. The adoption of its GenAI platforms is positioned to increase revenue by expanding the share of wallet with current clients.

- The company is monetizing its iX Hello products, designed to be accretive to earnings by the end of fiscal 2025. The transition from pilot phases to deployments is expected to positively impact earnings growth.

- Concentrix is experiencing revenue growth from partner consolidation. By expanding its business solutions and becoming a leading provider of integrated AI and business services, it is positioned to capture more client spending, impacting revenue and potentially improving net margins due to increased efficiency.

- The synergies from the Webhelp acquisition and integration are expected to yield margin expansion, with anticipated savings boosting non-GAAP operating margins over time. This contributes to both profitability and cash flow improvements.

- Concentrix’s capital allocation strategy involves share repurchases, which are likely to enhance EPS as the company takes advantage of perceived undervaluation. This strategy also includes investing for long-term growth while managing debt, enhancing net margins, and maintaining shareholder returns.

Concentrix Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

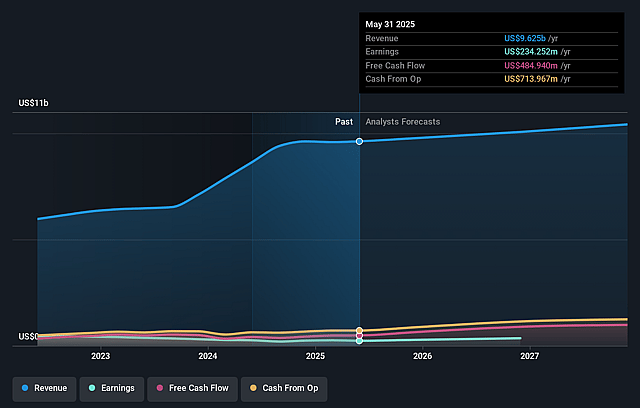

- Analysts are assuming Concentrix's revenue will grow by 2.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -13.4% today to 16.0% in 3 years time.

- Analysts expect earnings to reach $1.7 billion (and earnings per share of $27.66) by about June 2029, up from -$1.3 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $1.3 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 1.9x on those 2029 earnings, up from -1.3x today. This future PE is lower than the current PE for the US Professional Services industry at 19.7x.

- Analysts expect the number of shares outstanding to decline by 3.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Although Concentrix experienced a modest revenue growth of 1.3% year-over-year, a low growth rate could indicate potential challenges in maintaining or accelerating revenue growth, particularly if macroeconomic conditions do not improve, impacting future revenues.

- The pressure to integrate and harmonize Webhelp's operations and synergies could lead to increased costs and potential disruptions if not managed effectively. This could impact operating margins and net income if anticipated synergies are not realized timely.

- Concentrix faces potential currency exchange rate risks, with ongoing revenue guidance assuming up to a 135 basis point negative impact on full-year results. This could affect both reported revenues and net earnings.

- The company has a significant debt burden, with total debt standing at $4.9 billion. Rising interest rates or refinancing challenges could increase interest expenses, affecting net income and cash flow available for dividends or reinvestment.

- Dependence on a limited number of top clients, whose revenue growth outpaces the rest of the business, presents concentration risk. Any downturn in a major client's business could materially affect Concentrix's revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $41.25 for Concentrix based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $55.0, and the most bearish reporting a price target of just $32.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $10.6 billion, earnings will come to $1.7 billion, and it would be trading on a PE ratio of 1.9x, assuming you use a discount rate of 12.5%.

- Given the current share price of $27.82, the analyst price target of $41.25 is 32.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Concentrix?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.