Last Update 08 Jan 26

Fair value Decreased 12%WOOF: Q3 Profitability Upside Will Counter Softer Traffic And Store Closures

Narrative Update on Petco Health and Wellness Company

Analysts have trimmed their implied fair value estimate for Petco Health and Wellness Company from about US$5.14 to roughly US$4.53 per share. This reflects updated views that factor in reduced price targets around US$3.75 and US$3.00, ongoing competitive pressures, weaker macro conditions, and concerns about traffic softness and potential market share erosion.

Analyst Commentary

Recent Street research around Petco reflects a mix of caution on traffic and market share, alongside some constructive signals tied to Q3 performance and refreshed models. While price targets sit close to current trading levels, the commentary helps frame how the risk and reward are being weighed.

Bullish analysts are acknowledging ongoing macro and competitive headwinds, but they are also pointing to Q3 upside in profitability metrics and updated long term estimates as reasons to stay engaged rather than step away entirely.

Bullish Takeaways

- Some bullish analysts are using Q3 upside as a base to lift long term adjusted EBITDA and EPS estimates, which can support the case that current valuation already reflects a lot of bad news.

- The raised US$3 price target from US$2.75, even with an Underperform rating, signals that at least one bearish view on downside risk has moderated, which can matter for sentiment around downside scenarios.

- Equal Weight ratings, alongside trimmed price targets such as the move to US$3.75 from US$4.50, indicate that not all coverage is outright negative and that there is still room seen for execution to support current pricing.

- Q3 upside cited by bullish analysts, even with concerns around same store sales and traffic, suggests that management actions on costs and profitability are being recognized in models and could provide a cushion if topline trends remain choppy.

What's in the News

- Petco plans to close about 20 stores in fiscal 2025, pointing to a smaller physical footprint and potential consolidation of underperforming locations (Key Developments).

- The company issued earnings outlook for Q4 2025, guiding for net sales to be down low single digits year over year, which sets expectations for softer top line trends in the near term (Key Developments).

- For full year 2025, Petco expects net sales down 2.5% to 2.8%, indicating management is planning around a year of lower revenue versus the prior year (Key Developments).

Valuation Changes

- Fair Value: trimmed from about US$5.14 to roughly US$4.53 per share, a reduction of around US$0.61.

- Discount Rate: adjusted slightly higher from 12.32% to 12.5%, implying a modestly stricter hurdle rate.

- Revenue Growth: revised upward from about 176.3% to roughly 190.3%, reflecting a higher growth assumption in the model.

- Net Profit Margin: reduced from about 189.7% to roughly 154.6%, indicating lower expected profitability in the updated assumptions.

- Future P/E: moved from about 17.96x to roughly 19.26x, suggesting a higher multiple being applied to forward earnings in the updated framework.

Key Takeaways

- Integrating services, premium product leadership, and experiential retail strategies could unlock higher customer loyalty, market share, and margin expansion across channels.

- Enhanced supply chain efficiency, accelerating digital transformation, and growth in pet wellness trends provide multiple levers for sustained earnings and industry outperformance.

- Heavy dependence on physical stores, rising costs, and demographic headwinds threaten Petco's growth as competition and shifting consumer trends challenge profitability and margin expansion.

Catalysts

About Petco Health and Wellness Company- Operates as a health and wellness company, focuses on enhancing the lives of pets, pet parents, and its Petco partners in the United States, Mexico, and Puerto Rico.

- While analyst consensus already views Petco's focus on in-store veterinary and grooming services as a margin driver, this narrative may actually underappreciate the extent of cross-sell and share-of-wallet potential unlocked by integrating services, with data showing that services customers have significantly higher lifetime value and repeat visit frequency-supporting an upside surprise to both long-term revenue and net margin growth.

- Analyst consensus recognizes product assortment resets and premiumization as a top-line catalyst, but the real impact could be more dramatic given Petco's emerging ability to act as a trendsetter in premium, health-focused categories and human-pet crossover products, positioning the company to gain disproportionate market share and boost gross margins as consumer preferences increasingly favor high-margin wellness and specialty offerings.

- Petco's reimagined in-store experiences, powered by emotional marketing and unique event programming, are creating a differentiated omnichannel brand community that could drive a step-change in traffic, basket size, and customer retention, catalyzing outsized revenue gains by deeply capitalizing on millennials' and Gen Z's desire for experiential retail.

- Ongoing supply chain and inventory optimization has set the stage for sustained SG&A leverage and free cash flow generation, while new leadership in e-commerce-with a focus on personalization, repeat delivery, and digital loyalty-positions Petco to accelerate online growth and improve profitability far above current expectations.

- The broader long-term increase in pet ownership and the humanization of pets, combined with a national push into underpenetrated wellness services (from training to pharmacy and insurance), gives Petco a multi-pronged growth runway that could drive secular earnings expansion well in excess of industry averages as average spend per pet rises and high-frequency categories become recurring, supporting robust top-line and EBITDA growth.

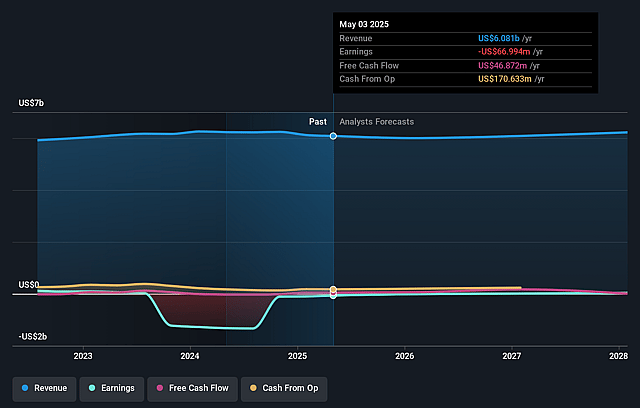

Petco Health and Wellness Company Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Petco Health and Wellness Company compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Petco Health and Wellness Company's revenue will grow by 1.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -0.5% today to 1.9% in 3 years time.

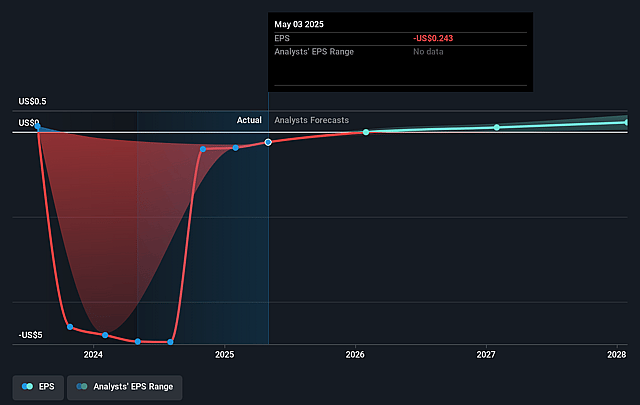

- The bullish analysts expect earnings to reach $120.9 million (and earnings per share of $0.42) by about September 2028, up from $-28.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 18.0x on those 2028 earnings, up from -36.0x today. This future PE is lower than the current PE for the US Specialty Retail industry at 19.3x.

- Analysts expect the number of shares outstanding to grow by 2.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.32%, as per the Simply Wall St company report.

Petco Health and Wellness Company Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The continued consumer shift toward e-commerce and direct-to-consumer models risks eroding the relevance and profitability of Petco's heavy brick-and-mortar store base, as evidenced by ongoing store closures and soft performance in the online segment, which could suppress net margins and limit long-term earnings growth.

- Increasing competition from online-first pet retailers and mass-market chains places pressure on Petco to discount or increase promotional activity, as seen in their need to eliminate "empty calorie promos" and clean up unprofitable sales, which risks compressing gross margins and impacting overall revenue growth.

- Industry-wide tariff headwinds, logistics costs, and the risk of rising animal healthcare expenses were flagged as becoming sequentially more meaningful, potentially raising average costs and reducing consumer discretionary spend on higher-margin items, which may limit gross margins and impede future earnings.

- Demographic headwinds such as a flat or shrinking number of pet families in the U.S., combined with urbanization trends, risk shrinking Petco's available customer base over the coming decade, which could restrict growth in sales and revenues even if operational improvements are made.

- Petco's dependence on new merchandising initiatives, private-label and exclusive products, and services to drive differentiation comes with execution risk; rapid shifts in consumer preference or supply chain disruptions could lead to inventory write-downs or inability to capture category growth, negatively impacting revenues and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Petco Health and Wellness Company is $5.14, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Petco Health and Wellness Company's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $5.14, and the most bearish reporting a price target of just $2.72.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $6.4 billion, earnings will come to $120.9 million, and it would be trading on a PE ratio of 18.0x, assuming you use a discount rate of 12.3%.

- Given the current share price of $3.62, the bullish analyst price target of $5.14 is 29.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Petco Health and Wellness Company?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.