Last Update 08 Jul 26

Fair value Decreased 7.92%MTX: Execution Risks And Defence Alliance Prospects Will Shape Future Returns

The analyst price target for MTU Aero Engines has been reduced from about €419 to roughly €386, as analysts factor in a higher discount rate, slightly softer revenue growth and profit margin assumptions, and a modestly higher future P/E multiple.

Analyst Commentary

Recent Street research on MTU Aero Engines reflects a mixed view, with some analysts adjusting price targets and ratings while others initiate coverage with a more positive stance. For you as an investor, the key themes center on how much you are willing to pay for the stock relative to its earnings, and how confident you are that MTU Aero Engines can deliver on its operational and growth plans.

Bullish Takeaways

- Bullish analysts initiating coverage see long term earnings potential at MTU Aero Engines that, in their view, supports a positive stance, even after recent price target cuts by others.

- Supportive views point to an earnings profile that, in their view, can justify a higher future P/E multiple than currently embedded in some models.

- Optimistic commentary implies confidence that MTU Aero Engines can execute on its plan well enough to work through current concerns embedded in more cautious research.

- Some bullish analysts appear comfortable that current valuation already reflects several identified risks, which they see as limiting further downside from execution missteps.

Bearish Takeaways

- Bearish analysts have downgraded MTU Aero Engines and lowered price targets, which points to concerns around the balance between expected earnings power and the current share price.

- Lower targets from multiple research houses suggest a more conservative view on revenue and margin assumptions feeding into valuation models.

- Cautious analysts appear less willing to ascribe a premium P/E multiple to MTU Aero Engines, given perceived uncertainty around the timing and reliability of future earnings.

- The cluster of downgrades and target reductions signals that some in the market are focused on execution risks and the possibility that previous expectations for the stock were too optimistic.

What’s in the News for MTU Aero Engines

- MTU Aero Engines is part of a proposed alliance called Team Gen 6, alongside Airbus Defence and Space, Autoflug, Diehl Defence, Hensoldt, Liebherr, MBDA and Rohde & Schwarz, according to the Financial Times.

- The alliance aims to develop a German led European alternative to the previously discussed Franco German fighter jet project, based on a letter sent to the offices of German Chancellor Friedrich Merz and defence minister Boris Pistorius, as reported by the Financial Times.

- Team Gen 6 is expected to be formally announced at the ILA Berlin Air Show, with MTU Aero Engines positioned as one of the core aerospace and defence partners in the group, according to the Financial Times.

Valuation Changes for MTU Aero Engines

- Fair Value: The estimated fair value has fallen slightly from €419.32 to €386.10.

- Discount Rate: The discount rate applied in the model has risen slightly from 5.66% to 6.21%.

- Revenue Growth: The assumed long term annual revenue growth rate has eased slightly from 10.05% to 9.70%.

- Net Profit Margin: The projected net profit margin has moderated from 10.61% to 10.19%.

- Future P/E: The assumed future P/E multiple has risen slightly from 22.34x to 23.62x.

Key Takeaways

- Strong demand for fuel-efficient engines and expanding aftermarket services drive recurring revenue, while MTU's technological leadership secures future growth opportunities.

- Diversification across commercial, military, and strategic partnerships enhances stability and positions the company for resilient margins despite geopolitical and regulatory uncertainties.

- Heavy reliance on key new engine programs, supply chain fragility, and rising geopolitical and R&D costs threaten margins, profit stability, and financial flexibility.

Catalysts

About MTU Aero Engines- Engages in the development, manufacture, marketing, and maintenance of commercial and military aircraft engines, and aero-derivative industrial gas turbines in Germany, other European countries, North America, Asia, and internationally.

- The surge in global air travel demand and robust order intake for new, fuel-efficient engines like the GTF (highlighted by record deals with airlines such as Wizz Air, Frontier, and LOT) are expected to continue driving strong OEM and MRO revenue growth and expanding order backlog, translating to higher long-term revenue and earnings visibility.

- Airlines' fleet modernization efforts and the growing focus on fuel efficiency and lower emissions support multi-decade replacement cycles; MTU's leadership in advancing geared turbofan technology and joint R&D for hydrogen-powered propulsion positions the company for continued margin expansion and future revenue streams from next-generation platforms.

- Expansion of high-margin aftermarket and MRO services, with capacity enhancements at facilities like EME Aero and the Fort Worth site, will support recurring revenue and improved net margins as narrow-body and wide-body engines enter heavy maintenance cycles, leveraging ongoing fleet utilization growth.

- The company's growing footprint in both commercial and military engine programs (with ramp-ups in EJ200 and T408 engines and involvement in strategic European defense collaborations) provides resilient, diversified revenue streams that reduce cyclicality and underpin stable long-term earnings.

- Heightened focus on supply chain localization, operational excellence, and European partnerships improves MTU's strategic value during an era of geopolitical and regulatory uncertainty, supporting more stable contract flows and potential margin resilience even amid rising protectionist risks.

MTU Aero Engines Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

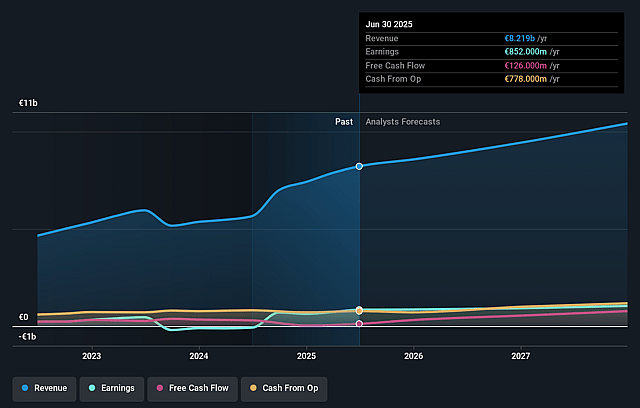

- Analysts are assuming MTU Aero Engines's revenue will grow by 9.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 11.2% today to 10.2% in 3 years time.

- Analysts expect earnings to reach €1.2 billion (and earnings per share of €22.26) by about July 2029, up from €992.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €1.4 billion in earnings, and the most bearish expecting €992.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 24.0x on those 2029 earnings, up from 20.0x today. This future PE is lower than the current PE for the GB Aerospace & Defense industry at 47.9x.

- Analysts expect the number of shares outstanding to grow by 3.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Increasing geopolitical tensions and evolving U.S./EU tariff regimes pose a significant, unpredictable risk, with management explicitly unable to quantify the ultimate impact of U.S. tariffs and potential countermeasures; escalation could disrupt MTU's market access, increase costs, and compress profit margins, thereby threatening both revenue growth and net margins over the long term.

- High revenue concentration in next-generation engine programs, particularly the GTF (PW1100G) engine family, exposes MTU to heightened operational and financial risks if material availability issues, technical failures, or warranty/compensation costs persist, which could erode net margins and dent earnings stability for years.

- Large, front-loaded profits in H1 are tied to exceptionally strong sales of spare and lease engines, with management warning of a normalization (decline) in these sales in H2 and beyond; this creates a risk of margin compression and volatile earnings as extraordinary contributions fade, potentially leading to lower profit growth or unexpected shortfalls.

- Ongoing supply chain fragility, including recent shortages stemming from incidents (e.g., SPS facility fire) and persistent delays for spare parts of mature platforms, underline MTU's vulnerability to long-term inflationary pressures, production bottlenecks, and the risk of future delivery shortfalls, all of which could constrain revenue and free cash flow.

- Rising R&D and capacity expansion costs-such as the USD 120 million investment in Fort Worth, 30-year license payments for LEAP engine access, and intensified commitments in hydrogen technology-raise the risk that high, recurring capital outlays may outpace cash generation if market uptake slows or competitive dynamics worsen, thereby pressuring net margins and reducing financial flexibility.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €386.1 for MTU Aero Engines based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €530.0, and the most bearish reporting a price target of just €275.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €11.7 billion, earnings will come to €1.2 billion, and it would be trading on a PE ratio of 24.0x, assuming you use a discount rate of 6.2%.

- Given the current share price of €368.1, the analyst price target of €386.1 is 4.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on MTU Aero Engines?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.