Last Update 10 Jul 26

Fair value Decreased 8.40%PAX: Secondary Fund Commitments And Fee-Paying AUM Plan Will Support Upside

Analysts have reduced their average price target on Patria Investments from about $17 to roughly $15.57, citing updated models that reflect recent revisions to growth, profitability and valuation assumptions, including cuts to targets such as $16 to $15 and a further $2 reduction from other coverage.

Analyst Commentary

Recent Street research on Patria Investments gives you a mixed picture, with updated models leading to lower price targets but not wholesale changes in fundamental views. The shift from about $17 to roughly $15.57 suggests analysts are reassessing how growth, profitability and valuation assumptions align with current execution.

Bullish Takeaways

- Bullish analysts still see enough support in Patria Investments' fundamentals to maintain coverage and formal price targets, rather than stepping away from the stock.

- The updated models, including those behind the $15 target from JPMorgan and the $2 reduction cited by Goldman Sachs, indicate that Patria Investments remains within a range where analysts consider its valuation measurable and grounded in current information.

- Maintaining a Neutral stance at JPMorgan suggests that, even with reduced targets, the risk and reward profile for Patria Investments is viewed as balanced rather than skewed to the downside.

- Ongoing model revisions signal that analysts continue to monitor Patria Investments closely, which can help investors track how expectations for growth and profitability evolve over time.

Bearish Takeaways

- Bearish analysts point to the sequence of target cuts, such as the move from $16 to $15 and the additional $2 reduction elsewhere, as a sign that prior growth and profitability assumptions for Patria Investments may have been too optimistic.

- Lower targets imply that analysts see less upside in the stock's valuation relative to earlier models, which may reflect more cautious expectations around execution or earnings power.

- The clustering of revised targets near the mid teens suggests analysts are re-basing what they consider a reasonable valuation range for Patria Investments, reducing room for error if performance falls short of forecasts.

- For more cautious investors, the step down in price targets can be a reminder to scrutinize the underlying drivers in these models, such as fee growth, operating margins and capital deployment, before assuming a strong growth profile for Patria Investments.

What’s in the News for Patria Investments

- Patria Investments closed its Secondary Opportunities Fund V with over US$670 million in commitments, more than 30% above its initial US$500 million target, with capital from institutional investors, family offices and private wealth channels across North America and Europe. (Source: recent fund closing announcement)

- The SOF V vehicle is focused on private equity secondary opportunities in mid market deals across Europe and North America, using Patria Investments' industry relationships and portfolio insights to pursue secondary acquisitions. (Source: recent fund closing announcement)

- Patria Investments is no longer a constituent of the Russell 2000 Dynamic Index, following its removal from that benchmark. (Source: index reconstitution update)

- The company reported a quarterly dividend of US$0.1625 per share, with an ex date and record date of May 18, 2026 and a payment date of June 11, 2026. (Source: dividend announcement)

Valuation Changes for Patria Investments

- Fair Value: updated from about $17 to roughly $15.57, a modest reduction in the modeled central estimate.

- Discount Rate: nudged higher from 7.88% to about 8.05%, reflecting slightly stricter assumptions in Patria Investments' valuation model.

- Revenue Growth: revised from roughly 14.77% to about 11.80%, indicating a smaller projected expansion in revenue, measured in dollars, than previously modeled.

- Profit Margin: adjusted from around 38.47% to about 40.61%, pointing to a slightly higher expected share of earnings, measured in dollars, on each dollar of revenue.

- Future P/E: moved from about 15.09x to roughly 13.61x, suggesting a lower earnings multiple being applied to Patria Investments in updated forecasts.

Key Takeaways

- Shifting investor appetite for alternative assets and inflation-resistant strategies is fueling strong fundraising, improved asset mix, and higher margins for Patria.

- Strategic expansion in Latin America and global diversification efforts position Patria to capture increasing institutional flows and sustain long-term revenue growth.

- Exposure to fee compression, regional instability, rapid acquisitions, and expansion risks could constrain margins, slow growth, and challenge Patria's profitability and operational resilience.

Catalysts

About Patria Investments- Operates as a private market investment firm.

- The accelerating global shift of institutional capital towards alternative assets, particularly private equity, infrastructure, and credit, is directly driving robust organic fundraising growth, reflected in Patria's repeated upward revision to annual fundraising guidance and rate of net new fee-earning AUM inflows; this underpins long-term revenue and earnings expansion.

- Increasing investor demand for inflation-resistant, high-yield strategies (such as infrastructure and credit) amid global macro uncertainty and high interest rates has led to outsized fundraising traction in these segments. This trend is poised to continue, improving both asset mix and margins as Patria allocates new capital into higher-fee, resilient strategies.

- Sustained economic development and a growing middle class in Latin America, alongside swelling pension fund pools (e.g., in Mexico), are expanding the firm's addressable market for alternatives. Patria's established regional presence positions it to capture a disproportionate share of local product launches and institutional allocations, supporting consistent AUM and fee revenue growth.

- Global investors are rotating capital into regions perceived as less exposed to U.S. trade and geopolitical risks, with Latin America and Europe benefiting. Patria is gaining incremental flows from Asian, Middle Eastern, and European LPs seeking portfolio diversification and new markets, which should accelerate fundraising and revenue diversification.

- The company's ongoing expansion into new strategies, products, and geographies (including recent acquisitive moves in Brazilian and Mexican real estate and GPMS European platforms) further diversifies fee revenues and enhances operating leverage, thus supporting higher sustainable margins and earnings compounding as scale advantages take hold.

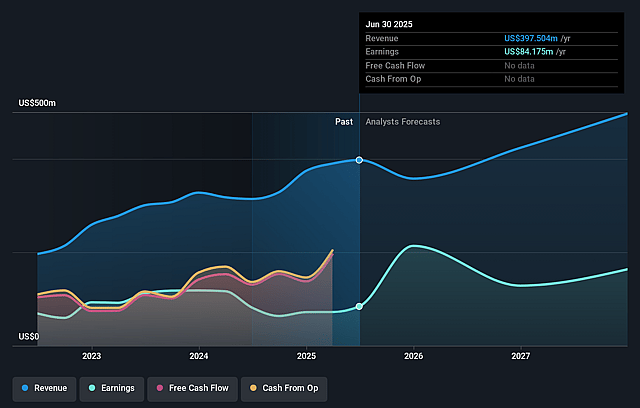

Patria Investments Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Patria Investments's revenue will grow by 11.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 18.1% today to 40.6% in 3 years time.

- Analysts expect earnings to reach $226.6 million (and earnings per share of $1.2) by about July 2029, up from $72.3 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.7x on those 2029 earnings, down from 24.7x today. This future PE is lower than the current PE for the US Capital Markets industry at 40.9x.

- Analysts expect the number of shares outstanding to decline by 0.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.05%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company faces potential fee compression as new fund strategies diversify its asset mix-management explicitly guides the average fee rate to decline from 95 basis points to 92–94 basis points in coming quarters; this long-term industry trend and evolving product mix could reduce net margins and slow overall earnings growth.

- A significant portion of Patria's fundraising and AUM is still anchored in Latin America (~30% of invested assets in Brazil, with further exposure in Chile, Colombia, and Peru), exposing the firm to cyclical regional political and macroeconomic instability (including tariff battles and elections); volatility or adverse outcomes here could lead to fundraising slowdowns, AUM outflows, or deterioration in asset performance, affecting revenues and profitability.

- Rapid expansion through acquisitions (e.g., multiple Brazilian REITs and entry into Mexico) may lead to operational complexity and integration challenges, especially as the firm increases its reliance on inorganic growth; if not managed effectively, this can result in rising expenses, lower operating leverage, and ultimately constrain future earnings growth.

- The company's business model, with 80% of fee-earning AUM locked in non-permanent vehicles (and a pending AUM pipeline tied to capital deployment), introduces some risk if investment opportunities slow or if any underlying asset classes (such as LatAm infrastructure or credit) see a cyclical downturn; delayed deployment or weaker performance could result in a lull in fee generation, directly impacting revenues and distributable earnings.

- Entrance into markets like Mexico, while gradual, involves material regulatory and competitive risks; attempts at further internationalization and product innovation may increase exposure to oversight, compliance costs, and competition with global players in both established and emerging markets-which could erode market share, pressure fees, and weigh on margins and long-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $15.57 for Patria Investments based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $558.0 million, earnings will come to $226.6 million, and it would be trading on a PE ratio of 13.7x, assuming you use a discount rate of 8.0%.

- Given the current share price of $11.06, the analyst price target of $15.57 is 29.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Patria Investments?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.