Last Update 20 Jul 26

Fair value Increased 32%OVH: Sovereign AI Infrastructure Push Will Still Restrain Earnings Outlook

Analysts have raised their price target for OVH Groupe to €11.33 from €8.59, citing updated assumptions on fair value, discount rate, revenue growth, profit margins and future P/E levels.

What’s in the News for OVH Groupe

- Scality expanded its technology partnership with OVHcloud, introducing a sovereign, cyber-resilient storage platform aimed at demanding AI workloads, combining high-performance object storage with cloud-native infrastructure and full data control. Source: Key Developments

- The joint Scality and OVHcloud solution offers deployment in a 100% dedicated sovereign cloud or on premises via the OVHcloud OPCP On-Prem Cloud Platform, with backup replication across multiple availability zones for higher resilience. Source: Key Developments

- The alliance focuses on helping organizations keep control over sensitive data in tighter regulatory conditions, while providing private infrastructure intended to support intensive artificial intelligence workloads, including model training and inference on mission-critical data. Source: Key Developments

- Scality RING and ARTESCA are integrated with OVHcloud OPCP to deliver S3-compatible object storage on customer premises, alongside managed services, orchestration and deployment automation that are independent of foreign public cloud providers. Source: Key Developments

- A dedicated storage offering on OVHcloud Bare Metal infrastructure via the HGR-STOR range enables off-site backups with private S3 compatibility, using tools such as Veeam and Commvault, and is positioned to support business continuity plans in which workloads can fail over to OVHcloud infrastructure if a primary site is disrupted. Source: Key Developments

Valuation Changes for OVH Groupe

- Fair Value: Updated from €8.59 to €11.33, representing a material upward revision in the estimated value per share.

- Discount Rate: Reduced from 11.43% to 10.68%, indicating a slightly lower required return in the updated model.

- Revenue Growth: Adjusted from 7.34% to 8.36%, reflecting a modestly higher assumed growth rate for € revenue.

- Net Profit Margin: Revised from 3.84% to 5.59%, representing a sizeable step up in expected € profitability relative to sales.

- Future P/E: Adjusted from 27.70x to 27.19x, a small decrease in the multiple applied to projected earnings.

Key Takeaways

- OVHcloud's focus on data sovereignty and strategic autonomy could capture growth due to increased demand for secure data solutions amid geopolitical tensions.

- Innovation with new products like the Bare Metal Pod and public cloud enhancements could drive higher revenue per customer and support earnings growth.

- OVHcloud's strong revenue growth, strategic product rollouts, and solid financial positioning suggest sustained profitability and potential future revenue growth amid shifting geopolitical demands.

Catalysts

About OVH Groupe- Provides public and private cloud, shared hosting, and dedicated server products and solutions worldwide.

- OVHcloud's commitment to data sovereignty and strategic autonomy positions it to capture growth opportunities as geopolitical tensions increase demand for secure and local data solutions, potentially driving future revenue growth.

- The continued development of Public Cloud offerings, including enhancements in artificial intelligence solutions and new product rollouts in their Availability Zones, could support future revenue growth by meeting growing customer demands.

- OVHcloud's investment in setting up infrastructure, like their upcoming data center in Milan and expansion into new Local Zones, implies plans for future growth, suggesting potential revenue expansion as these come online.

- The shift towards longer-term customer engagements through the success of their Savings Plan offers can enhance predictability and stability in revenues, potentially supporting future margin and earnings growth.

- The introduction of new products such as the ultra-secure Bare Metal Pod signals an ongoing innovation strategy, which could lead to higher ARPAC (Average Revenue Per Active Customer) and subsequently bolster earnings and margins.

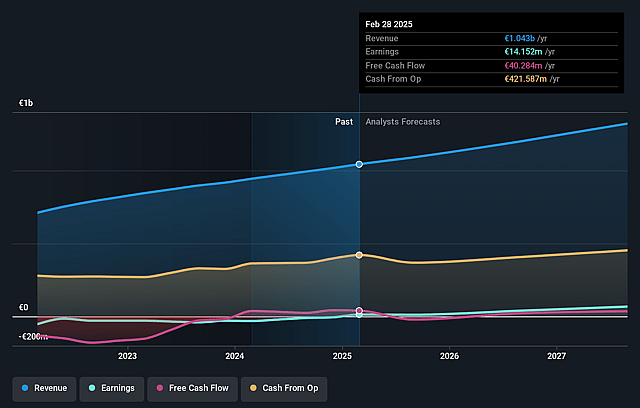

OVH Groupe Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming OVH Groupe's revenue will grow by 8.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.1% today to 5.6% in 3 years time.

- Analysts expect earnings to reach €78.6 million (and earnings per share of €0.27) by about July 2029, up from -€900.0 thousand today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €168.7 million in earnings, and the most bearish expecting €43.7 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 27.2x on those 2029 earnings, up from -2398.1x today. This future PE is greater than the current PE for the FR IT industry at 14.6x.

- Analysts expect the number of shares outstanding to decline by 1.93% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.68%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- OVHcloud experienced a solid revenue growth of 10.2% like-for-like, fueled by continued demand for Public Cloud and data sovereignty offers, suggesting that their revenue might remain strong.

- The company achieved an adjusted EBITDA margin of 40%, demonstrating strong operating leverage, which could sustain their profit margins.

- Successful refinancing with a €500 million bond and a €450 million green loan suggests a stable financial position, which may secure long-term earnings.

- OVHcloud continues to strengthen its market position by rolling out new Public Cloud and AI products, potentially leading to increased revenues from these innovative offerings.

- Demand for data sovereignty and strategic autonomy solutions positions OVHcloud well in a shifting geopolitical environment, offering potential for future revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €11.33 for OVH Groupe based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €19.0, and the most bearish reporting a price target of just €6.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €1.4 billion, earnings will come to €78.6 million, and it would be trading on a PE ratio of 27.2x, assuming you use a discount rate of 10.7%.

- Given the current share price of €14.35, the analyst price target of €11.33 is 26.6% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on OVH Groupe?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.