Key Takeaways

- Rising regulatory costs and difficulty competing with global giants threaten profitability and sustainable revenue growth as market conditions become tougher.

- Rapid expansion risks straining cash flow, while limited differentiation and past reliability issues may hinder customer retention and long-term earnings.

- Rising demand for sovereign cloud, ongoing innovation, operational efficiencies, international expansion, and strong ESG credentials are driving sustained growth and reinforcing OVH Groupe's market position.

Catalysts

About OVH Groupe- Provides public and private cloud, shared hosting, and dedicated server products and solutions worldwide.

- Rising operational complexity and compliance costs due to strict data sovereignty and regulatory requirements in Europe and globally are likely to erode OVH Groupe's margins in the medium to long term, pressuring EBITDA and net earnings despite strong current demand for sovereign cloud offerings.

- Intensifying competition from deep-pocketed US and Asian hyperscalers is expected to create persistent pricing pressure, potentially slowing OVHcloud's revenue growth and making sustainable double-digit top-line increases harder to maintain as market share gains become more difficult.

- The company's ambitious pace of international expansion, including the rapid rollout of Local Zones and new data centers, risks overextension and may drive elevated long-term capital expenditure, straining free cash flow and limiting capacity for R&D in value-added, higher-margin services.

- Ongoing industry commoditization of core cloud and hosting products is set to compress gross margins, exacerbated by OVHcloud's inability to differentiate sufficiently in leading-edge technologies like AI-native or edge computing, which could dampen future revenue growth and net profitability.

- OVH Groupe's past legacy infrastructure issues-including major technical incidents-and limited scale versus industry giants raise concerns about platform reliability and security, which may result in higher customer churn and necessitate continual, costly investments in upgrades, ultimately impacting both revenue retention and long-term earnings.

OVH Groupe Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on OVH Groupe compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

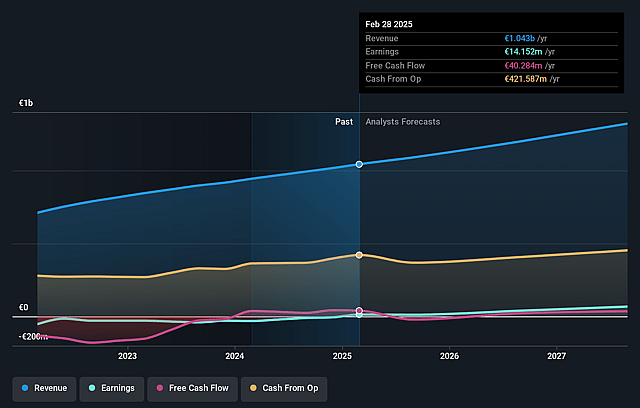

- The bearish analysts are assuming OVH Groupe's revenue will grow by 10.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 1.4% today to 4.5% in 3 years time.

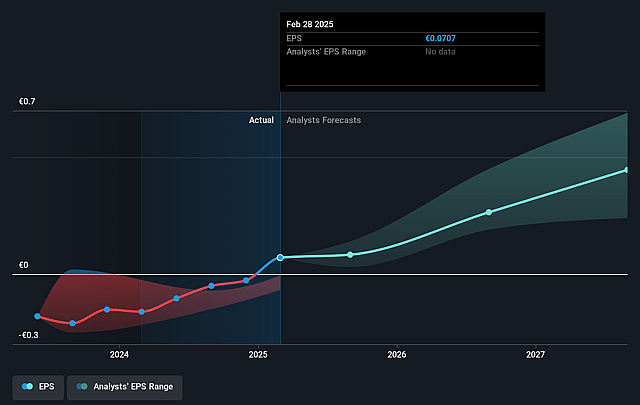

- The bearish analysts expect earnings to reach €62.0 million (and earnings per share of €0.49) by about September 2028, up from €14.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 30.2x on those 2028 earnings, down from 106.9x today. This future PE is greater than the current PE for the FR IT industry at 14.9x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.99%, as per the Simply Wall St company report.

OVH Groupe Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- OVH Groupe is benefiting from strong, ongoing demand for data sovereignty and cloud infrastructure in Europe, supported by regulatory trends favoring local providers, which may continue to drive revenue growth and increase OVH's market share.

- The company's expansion of innovative offerings, such as AI compute solutions, Public Cloud products in new Availability Zones, and sovereign cloud services, allows OVH to move up the value chain, supporting higher net margins and boosting revenue per customer over the long term.

- Energy-efficient, vertically integrated data center operations and proprietary water-cooling technology are reducing OVH's cost base, leading to structural improvements in EBITDA margins and enhancing overall company earnings.

- OVHcloud is diversifying geographically, especially in high-growth regions like Asia, the Middle East, and the United States, which offers a substantial runway for sustained revenue growth and buffers against local market downturns.

- Heightened ESG performance and successful access to green financing, such as the EU Taxonomy-aligned Green Loan, position OVHcloud as a leader in sustainable cloud operations, attracting environmentally conscious customers and supporting long-term profitability and client retention.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for OVH Groupe is €7.4, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of OVH Groupe's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €15.9, and the most bearish reporting a price target of just €7.4.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be €1.4 billion, earnings will come to €62.0 million, and it would be trading on a PE ratio of 30.2x, assuming you use a discount rate of 11.0%.

- Given the current share price of €9.98, the bearish analyst price target of €7.4 is 34.8% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.