Catalysts

About Johnson & Johnson

Johnson & Johnson is a global health care company that develops and sells pharmaceuticals and medical devices across Oncology, Immunology, Neuroscience, Cardiovascular, Surgery and Vision.

What are the underlying business or industry changes driving this perspective?

- Scaling across 28 platforms or products, each generating at least US$1b in annual revenue, with multiple brands such as DARZALEX, TREMFYA, CARVYKTI, ERLEADA and SPRAVATO already at high run rates, supports a broad base for potential future revenue and earnings growth rather than reliance on a single product.

- Heavy investment in drug discovery and deal making, with more than US$32b in 2025 allocated to R&D and M&A plus 51 approvals, 32 submissions and 11 new Phase III programs, sets up a sizeable pipeline that could feed future revenue and help sustain or expand net margins as higher value products mature.

- Growth in complex therapies that address high unmet medical need, including multiple myeloma treatments (DARZALEX, CARVYKTI, TECVAYLI, TALVEY), ICOTYDE in Immunology, and CAPLYTA and SPRAVATO in Neuroscience, positions J&J in areas where pricing power and treatment duration can be supportive for long term revenue and earnings.

- Rapid expansion in Cardiovascular and electrophysiology, with Abiomed, Shockwave, VARIPULSE and a planned cadence of at least one new pulsed field ablation catheter each year plus regular CARTO mapping upgrades, supports procedure growth and a richer mix of MedTech revenue that can lift segment margins and total company operating margin.

- Advances in Surgery and Vision, including MONARCH’s move into urology, the OTTAVA robotic surgery system, and premium eye products like TECNIS Odyssey and TECNIS PureSee along with ACUVUE OASYS MAX, target procedure efficiency and premium categories that can support higher average selling prices, contributing to revenue growth and improved earnings leverage.

Assumptions

This narrative explores a more optimistic perspective on Johnson & Johnson compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

- The bullish analysts are assuming Johnson & Johnson's revenue will grow by 7.1% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 28.5% today to 22.6% in 3 years time.

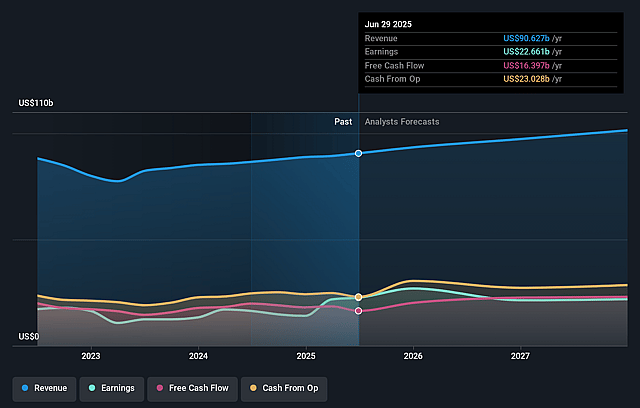

- The bullish analysts expect earnings to reach $26.2 billion (and earnings per share of $11.19) by about January 2029, down from $26.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 29.9x on those 2029 earnings, up from 19.8x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 19.8x.

- The bullish analysts expect the number of shares outstanding to grow by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.96%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The long term reliance on a small group of blockbuster drugs and devices, such as DARZALEX at over US$14b in annual sales and other multi billion dollar brands, increases exposure to patent expiries, biosimilar or generic competition and competing therapies. This could pressure revenue concentration and weaken earnings if replacement assets do not scale quickly enough.

- Ongoing and emerging pricing pressures, including U.S. government agreements to improve access and lower medicine costs, Part D redesign effects on products like ERLEADA and STELARA, and volume based procurement in China across Surgery and Orthopaedics, create a structural headwind for drug and device pricing. This could compress net margins and slow earnings growth.

- Higher structural cost burdens from tariffs in MedTech, a higher average debt balance that has already reduced net interest income, and continued heavy R&D and capital investment including new U.S. manufacturing facilities, increase the fixed cost base and financial risk if revenue growth slows. This could limit operating margin expansion and free cash flow.

- Large scale acquisitions and pipeline bets, including Intra Cellular Therapies, Halda Therapeutics and the portfolio of high cost late stage programs, carry integration, execution and clinical risk. Any underperformance, delays or safety issues could mean the acquired assets do not offset losses from products facing loss of exclusivity, putting pressure on long term revenue and earnings.

- Persistent legal and regulatory exposure, highlighted by the talc litigation and higher litigation costs of US$0.9b in Q4 2025 as well as the planned separation of the Orthopaedics business, could lead to additional settlements, adverse rulings, higher compliance costs or stranded costs. These outcomes would directly affect net income and constrain capital available for growth investments.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Johnson & Johnson is $265.0, which represents up to two standard deviations above the consensus price target of $224.09. This valuation is based on what can be assumed as the expectations of Johnson & Johnson's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $265.0, and the most bearish reporting a price target of just $155.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $115.7 billion, earnings will come to $26.2 billion, and it would be trading on a PE ratio of 29.9x, assuming you use a discount rate of 7.0%.

- Given the current share price of $220.14, the analyst price target of $265.0 is 16.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Johnson & Johnson?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.