Last Update 18 Apr 26

Fair value Increased 9.56%ABX: Reko Diq Review And Project Delays Will Shape Future Upside

Analysts have raised their CA$ fair value estimate for Barrick Mining from about CA$65.36 to about CA$71.61, citing updated assumptions around discount rates, revenue growth, margins, and a slightly lower future P/E multiple that together support the higher price target.

Analyst Commentary

Analysts are updating their views on Barrick Mining in the context of broader sector research that has recently featured valuation resets and rating changes for peers. Even when commentary is directed at other names, the themes around price targets, rating shifts, and expectations on execution can be useful reference points for how Barrick might be assessed.

Bullish Takeaways

- Bullish analysts see room for higher fair value estimates when they are comfortable adjusting assumptions for discount rates, revenue growth, and margins. This supports the recent lift in Barrick's CA$ fair value estimate.

- A slightly lower future P/E multiple used in the latest work suggests some optimism around the underlying business and cash flow outlook, while still incorporating a degree of valuation discipline.

- Research showing that peers can sustain target prices even after strong share price moves points to an appetite to reward solid execution. This can support Barrick's valuation if it delivers on its operational plans.

- Recent sector work indicates that analysts are willing to revisit targets rather than hold static views. This can be positive for Barrick if upcoming results or project updates align with their updated models.

Bearish Takeaways

- Bearish analysts highlight that, for some peers, strong share price performance has led to rating cuts as valuations move toward what they see as fully reflecting recent achievements. This is a cautionary signal for how far multiples could stretch for Barrick.

- Peer research that trims price targets, even when fundamentals are not being criticized, underscores the risk that Barrick's fair value could also be adjusted if market prices move ahead of model assumptions.

- The use of lower future P/E multiples in updated work, including for Barrick, shows a degree of restraint around how much investors might be willing to pay for earnings. This can cap upside if expectations run ahead of execution.

- Commentary that stresses valuation over rating labels suggests that, for Barrick, any misalignment between share price and updated fair value estimates could lead to more cautious stances even without a major change in the business story.

What's in the News

- Barrick is reviewing all aspects of the Reko Diq project after an escalation in security risks in Pakistan and the region, slowing development activity and extending the review to mid 2027. The company flagged the potential for significant increases to the previously disclosed capital budget and timeline for the project while maintaining community and social programs (company announcement).

- Barrick was removed from the S&P/TSX 60 Shariah Index, which may matter if you track Shariah compliant or index linked mandates (index announcement).

- The company scheduled a Special and Extraordinary Shareholders Meeting for May 8, 2026, which could be a focal point for major corporate decisions (company announcement).

- Barrick issued 2026 production guidance, outlining expected gold production of 2.90 million to 3.25 million ounces and copper production of 190,000 to 220,000 tonnes for the year (company guidance).

- The company completed a share repurchase of 51,900,000 shares, representing 3.04% of shares, for US$1,500 million under the buyback announced on February 12, 2025, including 12,110,000 shares or 0.72% for US$500 million bought between October 1 and December 31, 2025 (buyback update).

Valuation Changes

- Fair Value: The CA$ fair value estimate has risen from about CA$65.36 to about CA$71.61, reflecting the updated model inputs.

- Discount Rate: The discount rate has increased slightly from about 7.29% to about 7.80%, which generally makes future cash flows less valuable in the model.

- Revenue Growth: The revenue growth assumption has eased from about 15.66% to about 15.15%, a small reduction in the expected pace of future revenue expansion used in the valuation work.

- Net Profit Margin: The profit margin assumption has edged down from about 29.19% to about 28.77%, pointing to a slightly more conservative view on future profitability.

- Future P/E: The future P/E multiple applied in the analysis has shifted from about 14.06x to about 13.63x, indicating a modestly lower valuation multiple in the updated framework.

Key Takeaways

- Expansion and optimization of gold and copper assets, along with efficiency initiatives, are driving improved margins, production stability, and long-term earnings growth.

- Disciplined asset management and strong capital returns support operational resilience, attractive shareholder payouts, and potential for additional value creation through future projects.

- Political instability, ESG compliance, declining ore grades, resource constraints, and shifting demand trends present significant risks to profitability, operational stability, and long-term market valuation.

Catalysts

About Barrick Mining- Engages in the exploration, development, production, and sale of mineral properties.

- Significant ongoing expansion of both gold and copper production capacity-particularly at Lumwana and via organic growth at Fourmile and Reko Diq-positions Barrick to capture elevated long-term demand for gold (as a financial hedge during geopolitical uncertainty/inflation) and copper (driven by electrification and infrastructure investment), supporting top-line revenue growth over the coming decade.

- Continued focus on Tier 1, long-life assets in stable jurisdictions, and the divestment of non-core projects (e.g., Donlin Gold), enhance operational resilience and production predictability, which are likely to result in stronger, more consistent free cash flow and net earnings.

- Ongoing investment in operational efficiency-including automation, innovation, and digitization-is translating into reduced all-in sustaining costs across core assets, directly improving net margins and profitability as production volumes scale.

- Demonstrated ability to extend or expand existing mine lives (e.g., Pueblo Viejo stockpile optimization, resource conversion at Fourmile, new mining permits at Zaldivar) increases production visibility and the value of Barrick's high-quality resource base, supporting higher asset valuations and sustained earnings growth.

- Barrick's robust balance sheet and disciplined capital return strategy enable continued shareholder-friendly actions (dividends, buybacks) without diluting equity, while future catalysts-such as successful financing for Reko Diq and new exploration results-could further unlock value, improving investor return profiles and narrowing the gap between asset and market value.

Barrick Mining Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

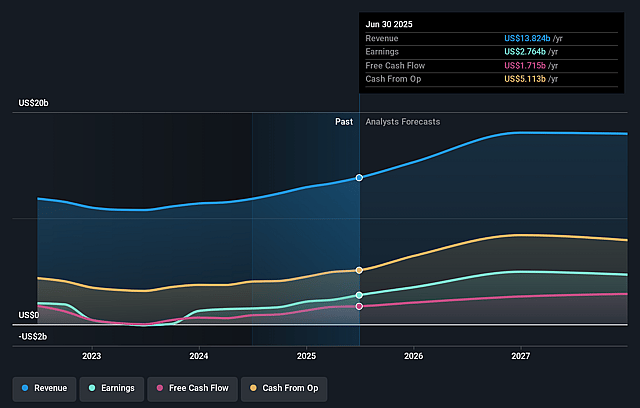

- Analysts are assuming Barrick Mining's revenue will grow by 15.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 29.4% today to 28.8% in 3 years time.

- Analysts expect earnings to reach $7.4 billion (and earnings per share of $4.74) by about April 2029, up from $5.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $9.1 billion in earnings, and the most bearish expecting $5.7 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.6x on those 2029 earnings, down from 14.5x today. This future PE is lower than the current PE for the CA Metals and Mining industry at 19.8x.

- Analysts expect the number of shares outstanding to decline by 2.56% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.8%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing risks in politically and economically unstable regions, such as the unresolved situation in Mali with Loulo-Gounkoto and continued reliance on African and Middle Eastern assets, could introduce volatility in revenue streams and threaten earnings due to potential asset expropriation, operational disruptions, and costly legal disputes.

- Heightened global scrutiny of large-scale mining projects and evolving ESG (Environmental, Social, Governance) requirements may drive up long-term capex and opex for complying with sustainability standards and securing permits, directly impacting net margins and free cash flow.

- Declining average ore grades at some of Barrick's key assets, along with the reliance on processing significant (aging) stockpiled ore at operations like Pueblo Viejo, risk increasing future cash costs and compressing gross and net margins, especially if gold/copper prices normalize.

- Long-term water and energy supply constraints, particularly in power-challenged regions like Zambia, pose operational risks and may result in higher energy costs and/or intermittent production disruptions, which would pressure margins and could force production cuts, affecting overall output and profitability.

- Growing global trends toward decarbonization and the rise of alternative materials and green technologies could gradually erode traditional gold and copper demand, ultimately suppressing Barrick's long-term revenue growth and market valuation if commodity prices weaken or sentiment shifts away from resource-intensive industries.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$71.61 for Barrick Mining based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$94.62, and the most bearish reporting a price target of just CA$30.7.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $25.9 billion, earnings will come to $7.4 billion, and it would be trading on a PE ratio of 13.6x, assuming you use a discount rate of 7.8%.

- Given the current share price of CA$59.35, the analyst price target of CA$71.61 is 17.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Barrick Mining?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.