Last Update 21 Apr 26

Fair value Decreased 3.52%MRP: Allan Gray’s Larger Stake Will Support Future Upside Potential

Analysts have trimmed their price target on Mr Price Group to ZAR243.93 from ZAR252.82, reflecting updated assumptions for slightly softer revenue growth, a marginally higher discount rate, and a small adjustment to future P/E and profit margin expectations.

What's in the News

- Allan Gray Proprietary Limited acquired an additional minority stake in Mr Price Group Limited (JSE:MRP) on January 22, 2026, increasing its clients' holding to 10.1318% of the total issued ordinary shares (Key Developments).

- The transaction closed as part of an M&A transaction event category, which signals continued institutional interest in Mr Price Group's equity (Key Developments).

- Allan Gray's clients now collectively hold more than a 10% stake. This may be relevant for investors tracking changes in significant shareholder ownership levels (Key Developments).

Valuation Changes

- Fair Value: Trimmed to ZAR243.93 from ZAR252.82, indicating a modest reduction in the valuation estimate.

- Discount Rate: Revised slightly higher to 19.57% from 19.16%, reflecting a small change in the required return input.

- Revenue Growth: Assumption adjusted to 6.04% from 6.54%, indicating a slightly softer top line growth outlook in the model.

- Net Profit Margin: Tweaked to 9.80% from 9.78%, a minimal upward revision to expected profitability.

- Future P/E: Updated to 22.13x from 22.45x, indicating a small reduction in the valuation multiple applied to future earnings.

Key Takeaways

- Focus on strategic market share gains has improved gross profit margins, potentially enhancing net margins.

- Expansion and supply chain initiatives could drive revenue growth and improve operational efficiency.

- Growing expenses and reliance on acquisitions amid high rates and volatile currency could undermine revenue and profitability if not managed effectively.

Catalysts

About Mr Price Group- Operates as a fashion retailer serving women, men, and children in South Africa and internationally.

- The management expects a much improved second half (H2) due to an inflection point in the retail sector driven by higher consumer and business confidence, suggesting potential revenue growth.

- The strategy of focusing on profitable market share gains rather than growth at all costs resulted in an increase in gross profit margin by 110 basis points, which could lead to improved net margins.

- Expansion plans with 92 new store openings in H1 and a target of 108 more in H2 could drive higher revenue through increased retail space and reach.

- The implementation of a Supply Chain Finance program, which has already unlocked significant working capital, could improve operational efficiencies, supporting better net margins and earnings.

- The company anticipates benefits from strategic category extensions and private label growth, especially in Telecoms, which could boost earnings through higher-margin sales.

Mr Price Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

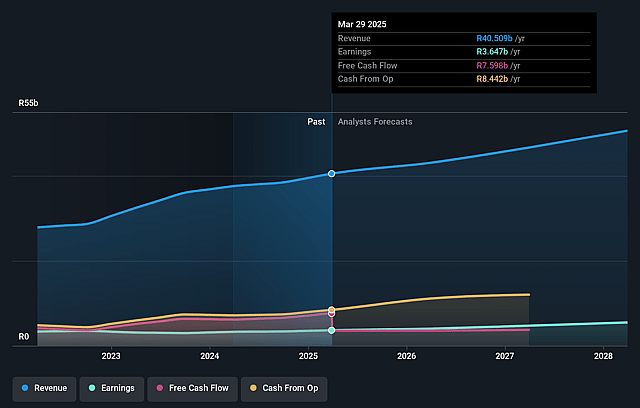

- Analysts are assuming Mr Price Group's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.0% today to 9.8% in 3 years time.

- Analysts expect earnings to reach ZAR 4.8 billion (and earnings per share of ZAR 16.92) by about April 2029, up from ZAR 3.7 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 22.2x on those 2029 earnings, up from 11.3x today. This future PE is greater than the current PE for the ZA Specialty Retail industry at 8.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 19.57%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent geopolitical tensions and currency volatility could impact consumer confidence and disposable income, affecting revenue and profit growth.

- High interest rates and inflation have historically reduced consumer spending power, potentially affecting Mr Price's revenue from lower to mid-income customer segments.

- Operating expenses are growing at a higher rate than revenue, which could pressure net margins and operating profit if not managed effectively.

- The market share gains are primarily driven by low growth and promotional environments, indicating a risk to sustained growth if competitive pressures increase or promotions become less effective.

- The increased level of debt attributable to Studio 88 and reliance on the performance of new acquisitions introduce uncertainties, which may impact earnings if these ventures do not perform as expected.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ZAR243.93 for Mr Price Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ZAR566.08, and the most bearish reporting a price target of just ZAR173.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ZAR49.4 billion, earnings will come to ZAR4.8 billion, and it would be trading on a PE ratio of 22.2x, assuming you use a discount rate of 19.6%.

- Given the current share price of ZAR164.01, the analyst price target of ZAR243.93 is 32.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Mr Price Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.