Last Update 02 Jun 26

WOOF: Self Help Initiatives And 2026 Plans Will Support Future Recovery

The analyst price target for Petco Health and Wellness Company is now framed in a tighter $3 to $5 range, with modest shifts in inputs such as the discount rate and future P/E reflecting mixed recent research, including both price target cuts around $3 to $3.95 and increases up to $4 and $5, as analysts weigh progress on growth initiatives against updated views on risk and earnings quality.

Analyst Commentary

Bullish Takeaways

- Bullish analysts point to recent research where Petco reported a quarter with adjusted EBITDA described as better than guided and above consensus, which they see as support for the current P/E framework used in price targets.

- Some target increases toward US$4 and US$5 are tied to the view that Petco is moving from stabilization to growth, with plans highlighted for 2026 that, if executed, could help underpin earnings quality over time.

- Jefferies highlights that Petco's initiatives are viewed as aligned with the retailer's core strengths and not dependent on an improving macro environment. Bullish analysts see this as key for execution risk.

- Supportive research notes argue that the stock, at recent levels, may underappreciate the progress already made and potential self help improvements. This view feeds into higher end targets within the US$3 to US$5 range.

Bearish Takeaways

- Bearish analysts have moved price targets closer to US$3, reflecting caution around risk and earnings quality even after a solid reported quarter. This tempers how much credit they are willing to give future growth initiatives in their models.

- The downgrade at Goldman Sachs and a target cut to US$3.95 from US$4.53 underscore concerns that recent performance may not fully offset perceived execution and balance sheet risks. This has led to a more conservative valuation stance.

- Lower targets from some firms suggest uncertainty around how consistently Petco can deliver on its growth plans through 2026. Bears see this as a reason to apply tighter multiples and more conservative assumptions in their P/E based work.

- Even where ratings remain Neutral or In Line, target trims signal that some analysts are not yet ready to factor in a stronger growth profile. They prefer to wait for clearer evidence on execution and the durability of recent EBITDA outcomes.

What's in the News

- Petco Health and Wellness Company introduced more than 130 summer products across cooling gear, toys, travel accessories and seasonal apparel, targeting pet safety, comfort and enrichment for warmer months. Source: Company product announcement.

- The company is offering a Summer Grooming Package priced at US$29, available as an add on to full service baths or grooms from May 3 through July 5, featuring seasonal shampoos, conditioners and extras such as nail buffing and teeth brushing. Source: Company product announcement.

- Petco outlined multiple in store and online promotions, including a 10% discount at petco.com over selected May dates, buy one get one 50% offers on certain private label summer collections, free toys with qualifying in store purchases and a series of free tasting events with branded pet food partners. Source: Company product announcement.

- The company highlighted ongoing in store engagement, including free puppy playtime sessions, pet adoption events in partnership with Petco Love and themed photo opportunities such as a Father’s Day event in June. Source: Company product announcement.

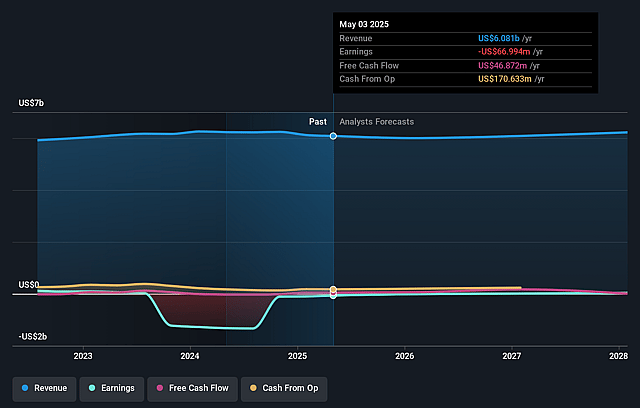

- Petco issued earnings guidance indicating that first quarter net sales are expected to be down 1% to flat year over year, and full year 2026 net sales are expected to be flat to up 1.5% year over year. Source: Corporate guidance update.

Valuation Changes

- Fair Value: Model fair value stays at $3.52, with no change between the prior and updated estimate.

- Discount Rate: The discount rate has risen slightly from 12.33% to 12.46%, indicating a modestly higher required return in the model.

- Revenue Growth: The revenue growth assumption is essentially unchanged, remaining at 1.278066% in the model.

- Profit Margin: The profit margin input remains effectively flat at 1.261431% in the latest update.

- Future P/E: The future P/E multiple has risen slightly from 19.24x to 19.31x in the updated assumptions.

Key Takeaways

- Expanding in-store experiences and wellness services aims to drive customer engagement, higher margins, and recurring revenue through premium offerings and service integration.

- Enhanced omnichannel strategy, loyalty programs, and differentiated merchandising seek to boost retention, operational efficiency, and brand exclusivity for long-term profitability.

- Ongoing sales declines, weak e-commerce performance, industry stagnation, rising costs, and high debt together threaten Petco's revenue growth, competitiveness, and financial flexibility.

Catalysts

About Petco Health and Wellness Company- Operates as a health and wellness company, focuses on enhancing the lives of pets, pet parents, and its Petco partners in the United States, Mexico, and Puerto Rico.

- Petco's focus on in-store experiences-including unique events, revamped merchandising, and enhanced customer-facing services-leverages the ongoing shift toward pet humanization and the desire for premium, experiential pet care, which is expected to drive higher customer engagement, increase foot traffic, and support revenue growth as these initiatives scale.

- Investments in personalized loyalty programs and data-driven marketing (including the upcoming relaunch of Vital Care in 2026) are designed to better capture the full customer lifecycle and expand share of wallet, with the potential to boost retention, average basket size, and long-term earnings consistency.

- Ongoing expansion and integration of high-margin pet wellness services (grooming, veterinary, pharmacy) within stores improves customer stickiness and creates recurring, higher-margin revenue streams, supporting net margin expansion and stronger bottom-line performance.

- Accelerated efforts to modernize and optimize the omnichannel experience-with new leadership, technology upgrades, and focus on seamless cross-channel execution-position Petco to participate in the continued migration to e-commerce and harness operational efficiencies, which should drive incremental revenue and profitability as digital rebounds.

- Company-wide focus on merchandising differentiation, faster product refreshes, and the introduction of owned brands and new pet-related categories aims to capitalize on long-term demand for innovation in pet products and nutrition, which can support both revenue growth and higher gross margins through enhanced exclusivity and reduced reliance on third-party brands.

Petco Health and Wellness Company Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Petco Health and Wellness Company's revenue will grow by 1.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.2% today to 1.3% in 3 years time.

- Analysts expect earnings to reach $78.1 million (and earnings per share of $0.28) by about June 2029, up from $9.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $129.2 million in earnings, and the most bearish expecting $58.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.3x on those 2029 earnings, down from 96.0x today. This future PE is lower than the current PE for the US Specialty Retail industry at 21.5x.

- Analysts expect the number of shares outstanding to grow by 1.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Net sales continue to decline (down 2.3% year-over-year with comparable sales down 1.4%), largely attributed to intentional moves away from unprofitable sales and store closures; while margins have improved, sustained top-line contraction puts long-term revenue growth at risk.

- The company's current turnaround is heavily dependent on in-store operations and events, but they acknowledged ongoing underperformance in e-commerce and are only in early stages of omnichannel improvements; this lag leaves Petco vulnerable to continued share loss to digital-native competitors like Chewy and Amazon, negatively impacting revenue and customer retention.

- Tariff impacts were minimal in the first half but are expected to become significant in the back half of the year, with the most meaningful headwinds in Q4; this could compress gross margins and limit the ability to reinvest, affecting profitability and earnings.

- The pet industry overall is described as relatively flat right now, with no meaningful growth in the number of pet-owning families; this stagnation in the core market, coupled with increasing competition and consumer price sensitivity, threatens Petco's addressable market and future sales growth.

- High leverage from past expansion (including significant net interest expense guidance and restrained capital expenditures) reduces financial flexibility, making it harder for Petco to weather economic volatility or invest sufficiently in innovation and growth, with direct implications for earnings and long-term viability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $3.52 for Petco Health and Wellness Company based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $5.0, and the most bearish reporting a price target of just $2.18.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $6.2 billion, earnings will come to $78.1 million, and it would be trading on a PE ratio of 19.3x, assuming you use a discount rate of 12.5%.

- Given the current share price of $3.06, the analyst price target of $3.52 is 13.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Petco Health and Wellness Company?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.