Last Update 11 Jun 26

LFCR: CDMO Site Transfers And 2028 Ramps Will Drive Long Term Upside

Narrative Update on Lifecore Biomedical

The analyst price target for Lifecore Biomedical has been reset to $5, reflecting a balance between a $5.50 target tied to expectations for a later breakout year and a $5 target that factors in softer FY26 guidance and delayed commercial ramps, which analysts generally view as timing related rather than a shift in the long term opportunity.

Analyst Commentary

Recent Street research on Lifecore Biomedical reflects a mix of optimism about the long term setup and caution around the near term execution and guidance. Price targets in the latest notes cluster around the US$5 to US$5.50 range, with views shaped mainly by the timing of commercial ramps and the updated FY26 outlook.

Bullish Takeaways

- Bullish analysts highlight the move to an Outperform rating with a US$5.50 price target as a signal of confidence that the company can create further long term value, even with expectations pushed out by roughly a year.

- They point to additional programs, including site transfer wins, as potential drivers that could support future revenue growth and justify valuations around or above the current US$5 to US$5.50 target range.

- The FY26 outlook is viewed by bullish analysts largely as a timing issue. This keeps their long term opportunity view intact and supports the idea that current valuation already reflects much of the near term risk.

- Solid Q4 performance in the latest commentary is seen as evidence that the core business can support execution on these programs once the commercial ramps occur.

Bearish Takeaways

- Bearish analysts have trimmed targets to US$5 from prior levels such as US$8.50. This signals reduced confidence in the pace of value realization and a preference for more conservative expectations on the timing of growth.

- The negative share reaction to FY26 guidance is cited as a reminder that the market is sensitive to execution risk, particularly around the later than expected commercial ramps.

- Lowered targets reflect concerns that softer FY26 guidance could limit upside in the near to medium term, even if the broader long term opportunity is unchanged.

- With ratings such as Equal Weight maintained alongside lower targets, bearish analysts are signaling a more balanced risk or return trade off. In this view, investors may need to see clearer progress on ramps before re rating the stock higher.

What's in the News

- Lifecore Biomedical signed a manufacturing services agreement with a leading ophthalmic disease management provider to handle process development and technical transfer for a next generation reformulation moving from vials to pre filled syringes, with anticipated commercial manufacturing upon regulatory approval. Source: Company client announcement.

- The company reaffirmed 2026 revenue guidance in the range of US$120 million to US$125 million. Source: Corporate guidance update.

- Lifecore signed two CDMO manufacturing service agreements with an existing U.S. biopharmaceutical customer, including a commercial site transfer for a currently marketed ophthalmic product and an expansion to manufacture the same therapy in a second delivery system that is currently produced in Europe, with both programs expected to contribute to 2028 commercial revenue. Source: Company client announcement.

- A new CDMO manufacturing services agreement was signed with a new aesthetics customer for an established, market approved product, shifting part of production for the U.S. market from in house manufacturing outside the U.S. to Lifecore, with the company stating that this product may generate commercial revenue within 24 months and citing this as its third commercial site transfer since October 2025. Source: Company client announcement.

- Lifecore issued guidance for 2026, 2027 and 2028, including expected 2026 revenue of approximately US$120,000 to US$125,000 and an expected net loss of US$28,900 to US$33,400, and outlined factors such as an anticipated customer loss, inventory decisions at a hyaluronic acid customer, a delayed commercial launch, along with expectations for modest revenue growth in 2027 and significant revenue growth in 2028 driven by existing customer program expansion and contributions from late stage pipeline programs. Source: Corporate guidance update.

Valuation Changes

- Fair Value: $6.67 remains unchanged, indicating no adjustment to the core intrinsic value estimate.

- Discount Rate: lowered slightly from 9.32% to 9.19%, reflecting a modest reduction in the required rate of return used in the model.

- Revenue Growth: held effectively steady at about 7.01%, with no material change to the projected growth rate.

- Net Profit Margin: trimmed slightly from 15.58% to 15.57%, indicating a very small adjustment to long term profitability assumptions.

- Future P/E: eased marginally from 13.04x to 13.00x, suggesting a slightly lower valuation multiple applied to forward earnings.

Key Takeaways

- Expanding partnerships, operational enhancements, and regulatory credibility are driving Lifecore's momentum in biopharma manufacturing, supporting stronger contract wins and profitability.

- Rising demand for injectable and HA-based drugs, along with new market entries, is broadening Lifecore's addressable market and cementing a foundation for sustained growth.

- Heavy reliance on key customers, margin compression, and sector risks challenge profitability and growth, while macroeconomic pressures threaten long-term financial stability and flexibility.

Catalysts

About Lifecore Biomedical- Operates as an integrated contract development and manufacturing organization in the United States.

- The company is benefiting from increased development agreements and partnerships with both new and existing customers, including high-value programs in late-stage development (such as the GLP-1 and ophthalmic programs), positioning Lifecore to capitalize on growing biopharma R&D spending-this should support future top-line growth and provide greater revenue visibility as pipeline products reach commercialization.

- Growing demand for injectable and HA-based pharmaceuticals, driven by aging demographics and a rise in chronic illnesses like osteoarthritis and ophthalmic disorders, is expanding Lifecore's target market; recent volume increases and take-or-pay commitments from major customers, including upcoming expansions into new regions (notably Asia Pacific), suggest a foundation for sustained revenue and earnings growth.

- Lifecore has executed significant operational improvements-rightsizing the workforce, implementing manufacturing automation, and introducing an enterprise resource planning (ERP) system-all of which are likely to increase operating leverage, improve margins, and reduce SG&A as a percent of revenue, thus contributing to higher future profitability.

- The shift toward pharmaceutical manufacturing onshoring and greater regulatory focus on supply chain security is driving increased outsourcing to specialized CDMOs in the US like Lifecore-management commentary and customer pipeline activity indicate that these industry dynamics can support continued contract wins, boosting long-term volume growth and recurring revenues.

- The company's strong quality management systems, recent positive FDA audit, and investment in business development talent have upgraded capabilities and customer perception, enhancing Lifecore's ability to win new contracts and sustain its reputation; this operational credibility is expected to translate into a higher win rate for projects and improved long-term revenue growth.

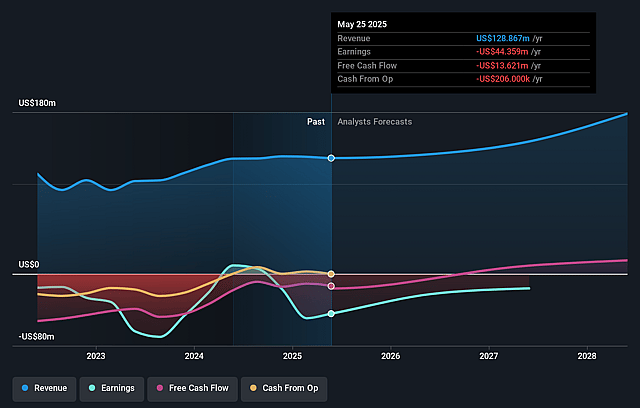

Lifecore Biomedical Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Lifecore Biomedical's revenue will grow by 7.0% annually over the next 3 years.

- Analysts are not forecasting that Lifecore Biomedical will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Lifecore Biomedical's profit margin will increase from -26.7% to the average US Life Sciences industry of 15.6% in 3 years.

- If Lifecore Biomedical's profit margin were to converge on the industry average, you could expect earnings to reach $24.7 million (and earnings per share of $0.66) by about June 2029, up from -$34.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.2x on those 2029 earnings, up from -6.2x today. This future PE is lower than the current PE for the US Life Sciences industry at 39.4x.

- Analysts expect the number of shares outstanding to grow by 0.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.19%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Lifecore remains highly dependent on a small number of large customers, with growth in HA manufacturing and revenue heavily concentrated in a single partner's supply chain shift; this customer concentration exposes the company to sudden revenue declines and earnings volatility if relationships change, contracts are lost, or terms are renegotiated, directly impacting future revenue visibility and profit stability.

- The company's recent financials reflect a net loss of $38.7 million for FY2025 versus net income the prior year, with declining gross profits in CDMO business segments and only marginal total revenue growth (0.5% YoY); these trends suggest persistent challenges in scaling profitability and improving net margins, raising questions about Lifecore's ability to deliver sustained earnings growth.

- Industry-wide margin compression and pricing pressure are foreseeable as competition intensifies in the injectable and hyaluronic acid contract manufacturing market; Lifecore's midterm margin expansion targets could be undermined if competitive or regulatory forces drive down pricing or increase cost of compliance, negatively affecting EBITDA and net margins.

- Advances in alternative drug delivery technologies or synthetic/biosynthetic substitutes for hyaluronic acid could erode demand for Lifecore's core offerings; such secular shifts in the biotechnology sector would hurt long-term top-line growth and threaten the relevance of the current product portfolio, putting revenues at risk.

- Lifecore's recently strengthened balance sheet is partly due to noncore asset sales, but the company remains exposed to broader macro risks such as rising interest rates, capital market volatility, and elevated compliance costs; these factors can increase operational overhead, borrowing costs, and refinancing risk, further squeezing net income and limiting the financial flexibility needed for long-term expansion.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $6.67 for Lifecore Biomedical based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $9.0, and the most bearish reporting a price target of just $5.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $158.6 million, earnings will come to $24.7 million, and it would be trading on a PE ratio of 13.2x, assuming you use a discount rate of 9.2%.

- Given the current share price of $5.69, the analyst price target of $6.67 is 14.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Lifecore Biomedical?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.