Last Update 25 May 26

Fair value Increased 20%RKLB: Future Space Systems Backlog Delivery Risks May Restrain Elevated Expectations

Rocket Lab’s updated fair value estimate has shifted from about $87 to roughly $104, as analysts point to a series of higher price targets and new Buy ratings that emphasize the stock’s role as a scaled Western launch and space systems platform, as well as views that its potential share of the broader space economy is still being underappreciated.

Analyst Commentary

Recent Street research around Rocket Lab has centered on its role as a scaled Western launch and space systems platform, with several analysts updating ratings and price targets following earnings, backlog commentary, and sector-wide space coverage launches.

Bullish Takeaways

- Bullish analysts highlight Rocket Lab as the only scaled Western launch and space systems platform outside of SpaceX. They argue that its implied share of the broader space economy in current valuation is relatively small compared with its platform positioning.

- Several firms raising price targets into the US$70 to US$90 range link their view to a mix of launch activity, space systems revenue and backlog. They suggest the current price does not fully reflect execution across both segments.

- The Geost acquisition is framed as expanding Rocket Lab into payloads as a new category of offering. Bullish analysts see this as supporting the stock's profile as a potential prime contractor for U.S. national security missions.

- Some commentary points to initiatives such as the Golden Domes program as potential demand drivers for Rocket Lab's government facing work. These analysts factor such initiatives into their more constructive stance on the stock.

Bearish Takeaways

- Not all coverage is outright positive. At least one neutral initiation indicates that some analysts prefer to wait for further execution evidence before assigning more aggressive valuation assumptions.

- Bullish analysts themselves acknowledge that current valuation already embeds expectations around increased launch cadence and continued growth in space systems backlog. Slower contract awards or launch activity could pressure those assumptions.

- The broader sector research that groups Rocket Lab with other space companies also flags competitive and pricing risks for peers. This can remind investors that execution and contract wins are critical for supporting current and higher price targets.

What’s in the News

- Rocket Lab filed a US$3b at-the-market follow-on equity offering of common stock, adding to earlier filings and completed offerings in 2026 that also used at-the-market structures.

- The U.S. Space Force awarded Rocket Lab a US$90m contract to design, build, integrate, and operate two Lightning bus based geostationary satellites hosting Heimdall space domain awareness payloads, with Rocket Lab acting as prime contractor and end-to-end mission provider.

- Rocket Lab introduced silicon based solar arrays and a hybrid solar array solution aimed at powering large-scale orbital data centers and constellations, expanding its vertically integrated space power portfolio alongside existing gallium arsenide and germanium products.

- Rocket Lab launched multiple missions in early 2026, including hypersonic test flights on its HASTE vehicle for the U.S. Department of War and dedicated Electron launches for ESA, JAXA, Synspective, and Synspective’s StriX SAR constellation, reinforcing its role in small launch and hypersonic testing.

- Google and SpaceX are reported to be in talks about orbital data centers, with Google also speaking to other launch companies such as Rocket Lab, Intuitive Machines, and Planet Labs about potential launch deals (Wall Street Journal).

Valuation Changes

- Fair Value: The updated fair value estimate has risen from about $86.83 to roughly $103.91, indicating a higher implied valuation level for the stock.

- Discount Rate: The discount rate has moved up slightly from 7.52% to about 7.88%, indicating a modestly higher required return in the model.

- Revenue Growth: The long term revenue growth assumption has edged down from roughly 36.83% to about 35.33%.

- Net Profit Margin: The projected net profit margin has shifted slightly lower from around 10.36% to about 9.94%.

- Future P/E: The assumed future P/E multiple has increased from about 470x to roughly 550x, implying a higher valuation multiple in the updated framework.

Key Takeaways

- Expanded vertical integration and end-to-end space solutions position Rocket Lab for major defense contracts and future margin growth.

- High launch cadence, satellite manufacturing, and reusable rocket development enable multi-year revenue growth, backlog expansion, and broader market access.

- High R&D costs, contract dependence, competition, and regulatory risks threaten profitability, while M&A and integration complexity may distract from core execution and margin improvement.

Catalysts

About Rocket Lab- A space company, provides launch services and space systems solutions in the United States, Canada, Japan, and internationally.

- Rocket Lab's move toward end-to-end space solutions-including the acquisition of Geost and expanding vertically integrated payload, satellite, and launch service capabilities-uniquely positions the company to capture larger, national security and defense contracts like the Golden Dome and SDA constellations, supporting significant top-line growth and enhanced gross margins in future quarters.

- Escalating demand for real-time data, earth observation, and global connectivity is driving increasing recurring revenue opportunities through satellite constellation launches and manufacturing-Rocket Lab's high Electron launch cadence and in-house satellite production (including potential for future proprietary constellations) are enabling the company to capitalize on these industry tailwinds, supporting multi-year revenue growth and backlog expansion.

- Successful development and operational ramp of the medium-lift reusable Neutron rocket will allow Rocket Lab to target larger, higher-value payloads (including those currently reliant on Falcon 9), increasing addressable market, boosting revenue, and driving margin expansion through production scale and vehicle reusability.

- Demonstrated pricing power and international expansion-highlighted by increased Electron average selling prices, strong international agency demand, and multi-launch agreements-reflect Rocket Lab's differentiated reliability and execute status in a consolidating launch market, likely supporting higher net margins and revenue predictability.

- Current elevated investment in R&D, infrastructure, and acquisitions is masking near-term earnings and cash flow, but the company's strong cash position, clear line of sight to significant government/commercial contract wins, and shifting focus from R&D to production post-Neutron debut are poised to deliver operating leverage and profitability as secular industry demand continues to accelerate.

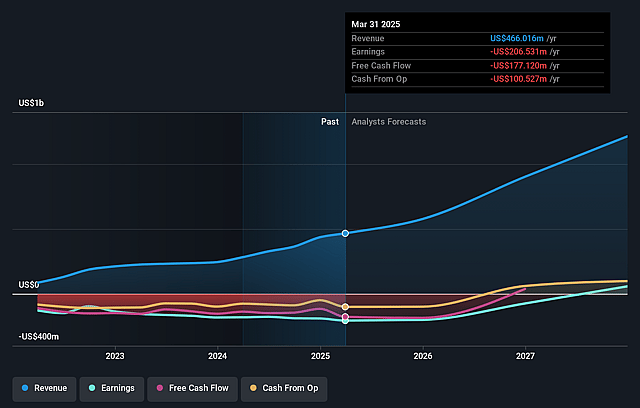

Rocket Lab Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Rocket Lab's revenue will grow by 35.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -26.9% today to 9.9% in 3 years time.

- Analysts expect earnings to reach $167.5 million (and earnings per share of $0.26) by about May 2029, up from -$182.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $351.9 million in earnings, and the most bearish expecting $14.0 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 552.3x on those 2029 earnings, up from -430.3x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 35.6x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.88%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Sustained elevated R&D and capital expenditures for Neutron development and scaling, with management projecting ongoing negative free cash flow and cash consumption into 2027 or beyond-this could materially pressure earnings and increase dilution risk if capital markets tighten or if expected revenue growth is delayed.

- Management highlighted project "lumpiness" and dependency on large contract wins (e.g., SDA Tranche 3, Golden Dome), exposing Rocket Lab to program delays, revenue recognition volatility, and heightened execution risk that could lead to irregular revenue, backlog fluctuations, and lower-than-expected operating leverage.

- While demand signals for Neutron are strong, actual customer commitment is lagging until a successful test flight, and management noted that increased competition (including established and well-capitalized peers like SpaceX and potential industry consolidation) could lead to margin compression, limited pricing power, and risk to long-term revenue targets if Neutron faces technical or schedule setbacks.

- The strategy of rapid vertical integration and aggressive M&A expands capabilities and addressable market, but also introduces operational complexities, integration risks, and possible distractions from core execution. Acquisition-driven growth requires sustained access to capital and successful integration to avoid impacting net margins and profitability.

- Exposure to variable trends in commercial and government launch budgets, and the risk of regulatory or geopolitical headwinds (such as export controls or launch bottlenecks at federal sites), could reduce launch frequency, delay government contract awards, and limit access to key international markets. These long-term trends could negatively impact revenue growth and market share if not mitigated.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $103.91 for Rocket Lab based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $150.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.7 billion, earnings will come to $167.5 million, and it would be trading on a PE ratio of 552.3x, assuming you use a discount rate of 7.9%.

- Given the current share price of $135.76, the analyst price target of $103.91 is 30.7% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Rocket Lab?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.