Narratives are currently in beta

Key Takeaways

- Expansion in HIV and oncology sectors can significantly boost revenue with innovative treatments and market penetration.

- Cost management and strategic product mix improvements are poised to enhance profit margins and support earnings growth.

- Competition in oncology and cell therapy threatens market share, while product setbacks and pricing pressures impact Gilead's revenue growth and financial stability.

Catalysts

About Gilead Sciences- A biopharmaceutical company, discovers, develops, and commercializes medicines in the areas of unmet medical need in the United States, Europe, and internationally.

- Approval and anticipated launch of lenacapavir for HIV prevention could significantly grow the PrEP market, which is expected to expand to new demographics and international markets. This growth should increase revenue.

- The early success and planned global rollout of Livdelzi for primary biliary cholangitis, with demand already surpassing expectations, suggest potential revenue growth as adoption continues.

- Anito-cel’s promising data in relapsed or refractory multiple myeloma may offer a best-in-class treatment option, supporting revenue growth in an expanding oncology portfolio.

- Ongoing expansion and innovative strategies in cell therapy, including community outreach, are likely to increase market share and drive revenue growth, overcoming competitive pressures.

- Continued cost management and expected favorable product mix are likely to sustain or improve operating margins and influence earnings positively, supporting EPS growth expectations.

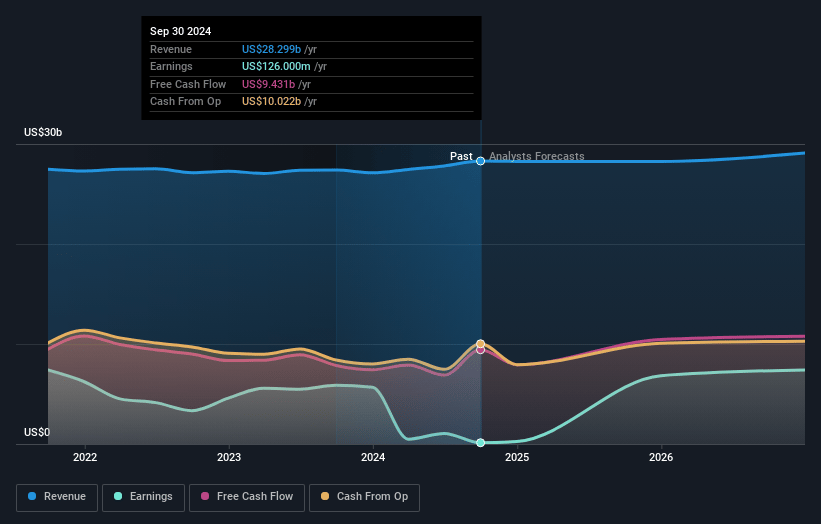

Gilead Sciences Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Gilead Sciences's revenue will grow by 2.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.4% today to 26.5% in 3 years time.

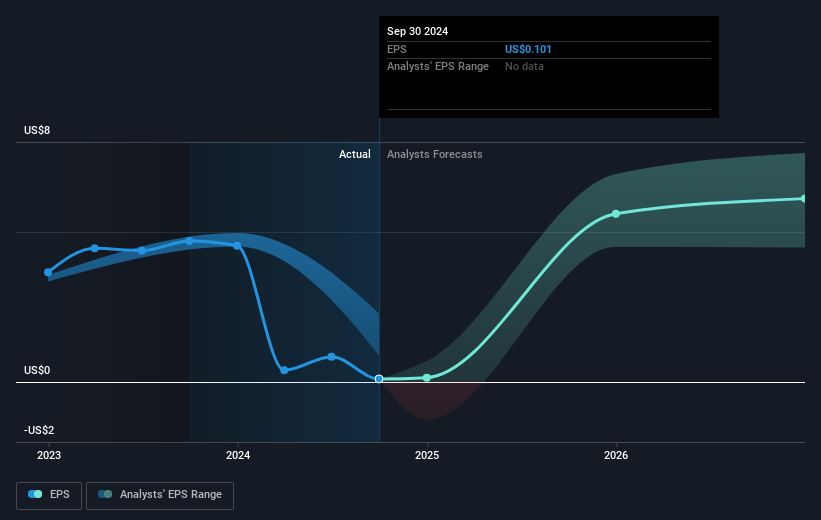

- Analysts expect earnings to reach $8.0 billion (and earnings per share of $6.5) by about January 2028, up from $126.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $9.5 billion in earnings, and the most bearish expecting $5.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.4x on those 2028 earnings, down from 896.4x today. This future PE is greater than the current PE for the US Biotechs industry at 16.5x.

- Analysts expect the number of shares outstanding to decline by 0.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.62%, as per the Simply Wall St company report.

Gilead Sciences Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Gilead's cell therapy sales have faced competition from both in-class rivals and out-of-class competitors such as bispecific antibodies, which could impact market share and revenue growth in the oncology segment.

- The removal of the second-line non-small cell lung cancer indication for Trodelvy led to a $1.8 billion impairment charge, affecting the net earnings and potentially signaling challenges in capturing market opportunities in this area.

- The commercial launch of new products like Livdelzi and lenacapavir requires significant investment in prelaunch activities, which could pressure net margins if revenue growth does not meet expectations.

- Potential rising competition in the cell therapy market, particularly with products like CAR T facing uptake challenges and regulatory hurdles, could limit future growth and profitability.

- Dependence on Medicaid and 340B pricing could expose the HIV portfolio to financial risks from potential policy changes and reimbursement pressures, impacting revenue stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $98.88 for Gilead Sciences based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $73.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $30.1 billion, earnings will come to $8.0 billion, and it would be trading on a PE ratio of 18.4x, assuming you use a discount rate of 6.6%.

- Given the current share price of $90.63, the analyst's price target of $98.88 is 8.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives