Last Update 27 Mar 26

GLDD: Saltchuk Cash Offer And Downgrades Will Define Limited Upside Risk Profile

Analysts have trimmed their outlook on Great Lakes Dredge & Dock, cutting the price target to $17.00 as they align with the agreed $17 per share cash acquisition by Saltchuk Resources and see limited additional upside, with multiple firms shifting to more neutral ratings.

Analyst Commentary

Recent research around the Saltchuk Resources agreement has become more muted, with several firms moving to neutral stances as the US$17 per share cash offer now anchors valuation expectations and leaves less room for additional re rating.

Bullish Takeaways

- Bullish analysts see the US$17 per share all cash offer as providing clearer value visibility. This reduces uncertainty around where the stock might trade on standalone assumptions.

- The announced definitive agreement and subsequent Saltchuk tender offer are viewed as increasing the clarity around deal completion. Some investors may value this over potential upside from an independent path.

- For investors focused on execution risk, the shift to a takeout price is seen as simplifying the thesis. There is less dependence on future project wins or margin outcomes to justify current valuation.

- By aligning price targets to US$17, analysts highlight that the current valuation is now closely tied to a specific transaction value rather than open ended market expectations.

Bearish Takeaways

- Bearish analysts point to limited remaining upside to the US$17 offer price, which caps the potential return tied to re rating or stronger execution on existing projects.

- The series of downgrades to Neutral or Market Perform signals that, at current levels, the risk or reward profile may be less compelling compared with other names that are not subject to a pending acquisition.

- With price targets cut from higher prior levels to US$17, there is less support for a premium valuation above the deal price based on execution, growth, or standalone potential.

- The view that deal completion risks have narrowed also means there is less room for a valuation bounce from improved deal confidence. This further constrains upside for new entrants at or near US$17.

What's in the News

- Saltchuk Resources agreed to acquire Great Lakes Dredge & Dock in a transaction valuing the company at approximately US$1.2b in equity and US$1.5b in total transaction value. (Key Developments)

- The tender offer launched on March 4, 2026, at US$17.00 per share. This reflects a 25% premium to Great Lakes' 90 day volume weighted average price as of February 10, 2026, and a 5% premium to the company’s all time high closing price. (Key Developments)

- The transaction has unanimous approval from both companies' boards. It is backed by fully committed financing from Bank of America, Wells Fargo, U.S. Bank, and PNC, and is currently scheduled to close on April 1, 2026, subject to remaining conditions. (Key Developments)

- Following the tender offer, any remaining shares are expected to be acquired via a second step merger at the same US$17.00 per share price. After this, Great Lakes would become a wholly owned subsidiary of Saltchuk and its stock would cease trading on Nasdaq. (Key Developments)

- Johnson Fistel, PLLP has started an investigation into the proposed sale terms, and the FTC has already terminated the Hart Scott Rodino Act waiting period, satisfying the competition related condition to the offer. (Key Developments)

Valuation Changes

- Fair Value: $17.00 remains unchanged, in line with the agreed cash offer level.

- Discount Rate: risen slightly from 9.44% to about 9.49%, indicating a modestly higher required return in the model.

- Revenue Growth: effectively steady at about 5.25%, with only an immaterial adjustment in the estimate.

- Net Profit Margin: essentially unchanged at about 8.87%, keeping earnings expectations broadly consistent.

- Future P/E: inched up slightly from roughly 15.27x to about 15.30x, reflecting a marginal adjustment to the valuation multiple.

Key Takeaways

- Expanding project pipeline and new vessel delivery drive operational efficiency, margin improvement, and long-term revenue growth through coastal, energy, and infrastructure projects.

- Diversification into offshore energy and international markets reduces dependence on U.S. cycles and improves earnings stability, while free cash flow growth enables balance sheet strength.

- Reliance on government and LNG work, constrained project awards, and high leverage heighten vulnerability to market slowdowns, regulatory delays, and international competitive pressures.

Catalysts

About Great Lakes Dredge & Dock- Provides dredging services in the United States.

- Record levels of government funding for coastal protection and port deepening projects, combined with a substantial $1B backlog and new awards, provide strong revenue visibility through 2026–2027 and support expectations for sustained top-line growth.

- Delivery of new, modern dredging vessels (Amelia Island, Acadia) is increasing operational capacity and efficiency, enabling GLDD to target higher-margin projects and reduce operating costs, which should positively impact operating margins and net profitability.

- Increasing investments in U.S. coastal resiliency and critical subsea infrastructure (e.g., for LNG, power, telecom, and port assets) due to climate-driven risks are expanding GLDD's addressable project pipeline, driving long-term revenue and earnings growth.

- Strategic expansion into offshore energy and international markets via the Acadia vessel diversifies revenue sources, taps new high-margin business lines (offshore wind, asset protection), and reduces exposure to U.S. budget and permitting cycles, improving earnings stability.

- With the capital-intensive newbuild program completing and free cash flow expected to rise significantly in 2026, GLDD will strengthen its balance sheet, enabling deleveraging and potential for future shareholder returns-supportive of net margin and earnings per share growth.

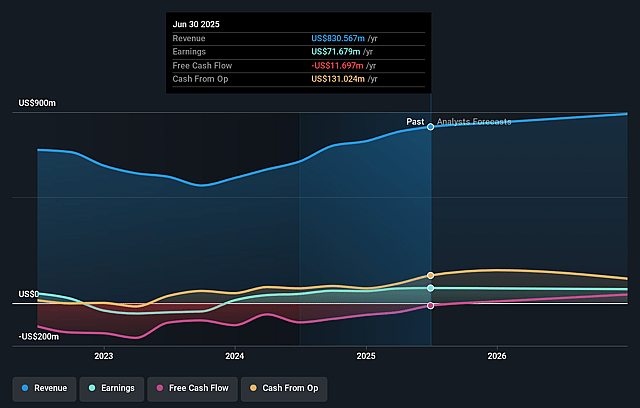

Great Lakes Dredge & Dock Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Great Lakes Dredge & Dock's revenue will grow by 5.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.3% today to 8.9% in 3 years time.

- Analysts expect earnings to reach $91.9 million (and earnings per share of $1.35) by about March 2029, up from $73.5 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $101.3 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.4x on those 2029 earnings, which is the same as it is today today. This future PE is lower than the current PE for the US Construction industry at 33.3x.

- Analysts expect the number of shares outstanding to decline by 1.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.49%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's pace of new project awards is currently constrained by both sector-wide pauses (e.g., the U.S. offshore wind slowdown and a "normalized" bid market with fewer capital deepening projects in the near term) as well as its own high asset utilization, limiting its ability to participate in over 50% of available bids; this may create future gaps in backlog and affect revenue visibility beyond 2026.

- Continued high dependence on government (U.S. Army Corps of Engineers) and LNG contracts leaves revenue exposed to political/budgetary uncertainty and shifts in infrastructure spending priorities; any delay or reduction in government funding or LNG export capacity could negatively impact revenues and earnings.

- The heavy recent and ongoing capital expenditure program, while modernizing the fleet, has led to increased leverage and higher maintenance obligations; if demand softens or bid activity weakens, elevated debt and depreciation costs could compress net margins and free cash flow.

- Initial signs of slowing in the U.S. offshore wind pipeline have forced the company to pivot the Acadia's market focus toward international work starting in 2027; increased reliance on winning projects in Europe and Asia introduces heightened competition, regulatory risk, and potential for lower pricing power, potentially lowering international revenue and profitability.

- Industry-wide cycles remain pronounced, with evidence of project timing and award delays driven by regulatory issues (e.g., "continued resolution" limits new project starts until Federal budgets are finalized), which may create earnings volatility and risks to long-term revenue stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $17.0 for Great Lakes Dredge & Dock based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.0 billion, earnings will come to $91.9 million, and it would be trading on a PE ratio of 15.4x, assuming you use a discount rate of 9.5%.

- Given the current share price of $16.97, the analyst price target of $17.0 is 0.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Great Lakes Dredge & Dock?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.