Last Update 22 Aug 25

Fair value Decreased 15%Despite a higher consensus revenue growth forecast, a sharp reduction in LARK Distilling’s future P/E has driven the analyst price target down from A$2.00 to A$1.81.

Valuation Changes

Summary of Valuation Changes for LARK Distilling

- The Consensus Analyst Price Target has fallen from A$2.00 to A$1.81.

- The Future P/E for LARK Distilling has significantly fallen from 61.34x to 41.73x.

- The Consensus Revenue Growth forecasts for LARK Distilling has risen from 24.6% per annum to 26.0% per annum.

Key Takeaways

- Strategic expansion into Asian markets and innovative product offerings position the brand to capture premiumization trends and drive sustainable global growth.

- Enhanced consumer engagement, experiential luxury focus, and operational efficiencies support premium pricing, margin improvement, and increased customer lifetime value.

- Heavy reliance on premium whisky demand, shifting sales channels, and ongoing investment needs pose significant risks to profitability, margins, and future shareholder returns.

Catalysts

About LARK Distilling- Engages in the production, marketing, distribution, and sale of craft spirits.

- The strategic international expansion, especially recent distribution agreements in key Asian markets (e.g., Singapore, Indonesia, Korea, Vietnam, and pending entry into China), positions LARK to capitalize on rising demand for premium craft spirits globally-likely driving meaningful revenue growth as exports scale from a low base.

- The completed brand restage and marketing investments, validated by positive trade and consumer feedback, underpin LARK's ability to differentiate as an authentic luxury brand with strong provenance, enabling premium pricing, deeper consumer engagement, and potential to improve net margins as brand equity and loyalty are built.

- Broadening direct-to-consumer channels (e-commerce, hospitality, and exclusive/limited releases) and experiential tourism at the redeveloped Pontville site leverage the trend toward experiential luxury consumption, which can boost high-margin sales, increase customer lifetime value, and provide a buffer to margin pressure from wholesale channel mix changes.

- Increased production capacity and operational efficiencies-delivered through the modular, automated Pontville upgrade-enable scalable growth to meet demand while controlling costs, supporting improved operating leverage and long-term earnings accretion, especially as higher-volume export opportunities materialize.

- An expanded and innovative product portfolio (e.g., KURIO, halo releases, collectible editions for Asian markets) positions LARK to benefit from continued premiumization in spirits, supporting higher average selling prices and safeguarding gross profit as the mix shifts toward high-value, limited, or bespoke offerings.

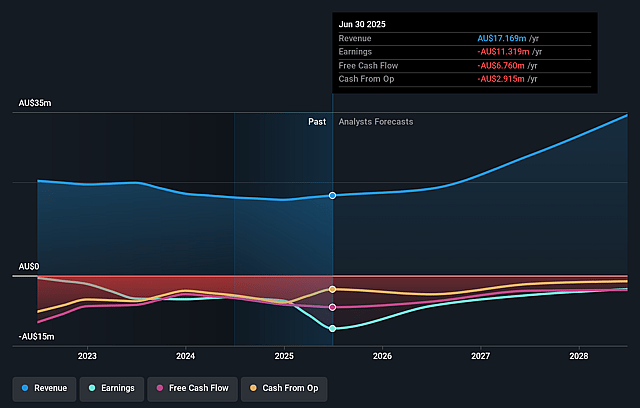

LARK Distilling Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LARK Distilling's revenue will grow by 23.6% annually over the next 3 years.

- Analysts are not forecasting that LARK Distilling will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate LARK Distilling's profit margin will increase from -65.9% to the average AU Beverage industry of 16.3% in 3 years.

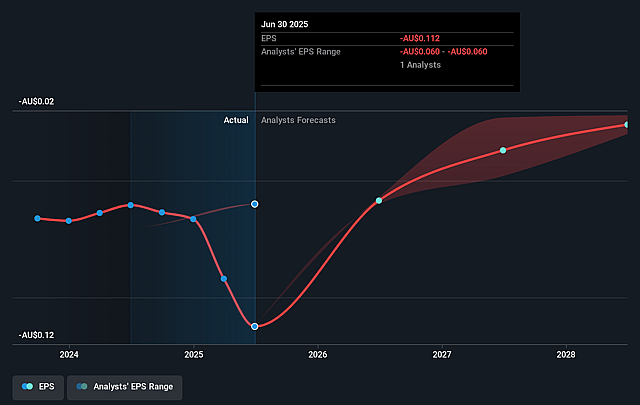

- If LARK Distilling's profit margin were to converge on the industry average, you could expect earnings to reach A$5.3 million (and earnings per share of A$0.05) by about September 2028, up from A$-11.3 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 41.7x on those 2028 earnings, up from -7.2x today. This future PE is lower than the current PE for the AU Beverage industry at 79.1x.

- Analysts expect the number of shares outstanding to grow by 0.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.48%, as per the Simply Wall St company report.

LARK Distilling Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The shift towards a distributor-led sales model and growing export channels is leading to a declining gross profit margin (down from 68% to 64% in FY '25), and management expects modest further declines as channel mix shifts away from higher-margin D2C, which could suppress future earnings growth even if top-line revenue increases.

- The company is increasing marketing expenditure significantly (up $2.4 million or ~34% of net sales in FY '25), pushing operating cash flows to remain negative through FY '26 before anticipated improvement, meaning that profitability and positive net cash generation are still at least two years away and subject to successful execution of international expansion.

- LARK's growth prospects and premium positioning are heavily exposed to the resilience of the ultra-premium/high-end whisky segment, which has already seen post-COVID correction and ongoing headwinds in domestic and international markets, creating the risk that a further cyclical or secular consumer shift away from luxury alcohol could materially impact sales volumes and revenue.

- As LARK deploys its Whisky Bank inventory, a portion of this maturing stock (specifically, inventory from the Shene acquisition) is held at higher fair value, and management has cautioned that as this stock is depleted from FY '26 onward, non-cash gross margin dilution will occur, potentially weighing on reported profitability and net margins at a critical time of expansion.

- Although LARK is well capitalized following a recent equity placement, its need for ongoing elevated brand investment and uncertain pace of international growth could result in future capital raises or dilution, which-when combined with scale disadvantages relative to global competitors-may limit per-share earnings, compress returns, and expose the share price to downside if growth lags expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$1.71 for LARK Distilling based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$2.9, and the most bearish reporting a price target of just A$0.89.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$32.4 million, earnings will come to A$5.3 million, and it would be trading on a PE ratio of 41.7x, assuming you use a discount rate of 6.5%.

- Given the current share price of A$0.77, the analyst price target of A$1.71 is 55.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on LARK Distilling?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.