Key Takeaways

- Shifting consumer trends, regulatory pressures, and global competition threaten long-term growth, pricing power, and margin expansion despite rising demand and brand initiatives.

- High marketing and inventory costs, coupled with supply chain vulnerabilities, may continue to pressure cash flows and delay sustainable profitability.

- Heavy marketing spend, distributor reliance, and global expansion increase pressure on margins, profitability, and expose LARK to economic, regulatory, and competitive risks.

Catalysts

About LARK Distilling- Engages in the production, marketing, distribution, and sale of craft spirits.

- Although global demand for premium and craft spirits continues to rise, particularly in Asia-Pacific and among younger consumers with growing disposable income, LARK's growth trajectory could be threatened by increasing global health consciousness and a shift in consumer preference towards lower-alcohol and alcohol-free beverages, which may cap long-term revenue expansion.

- While the recent brand restage and expanded distribution in Asian and travel retail markets are expected to enhance LARK's brand recognition and diversify revenue streams, regulatory risks loom large as tightening advertising restrictions and the potential for higher excise duties in key export destinations could compress future net margins and increase compliance costs.

- LARK's successful investment in scalable production capacity and operational efficiency at the Pontville site positions it well to leverage economies of scale and grow gross profit, yet its limited global scale compared to multinational peers magnifies vulnerability to input cost inflation and restricts the ability to fully withstand supply chain shocks or shifts in barley and water availability due to climate change, which could eat into net margins.

- Although the company's strong balance sheet and disciplined capital allocation provide a buffer and runway to invest for growth, the heavy upfront marketing spend required to drive global brand awareness-alongside ongoing capital tied up in ageing whisky inventories-may continue to pressure operating cash flows and delay the timeline to sustainable positive earnings.

- Despite increased demand for authentic, provenance-driven craft spirits and regulatory liberalization trends in some markets facilitating broader distribution, intensifying global competition from established international craft distilleries and new entrants could erode pricing power, limit LARK's ability to sustain premium selling prices, and ultimately limit long-term earnings growth.

LARK Distilling Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on LARK Distilling compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

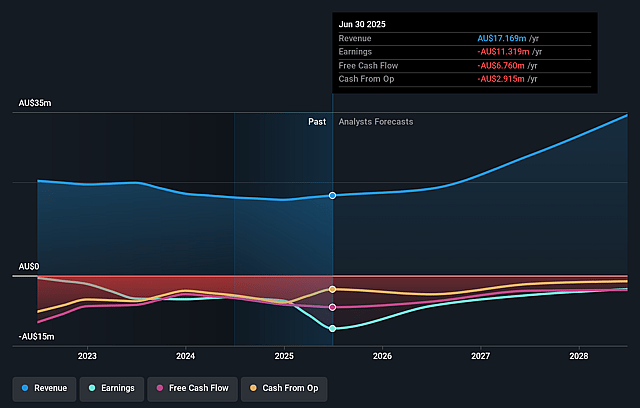

- The bearish analysts are assuming LARK Distilling's revenue will grow by 19.6% annually over the next 3 years.

- The bearish analysts are not forecasting that LARK Distilling will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate LARK Distilling's profit margin will increase from -65.9% to the average AU Beverage industry of 16.3% in 3 years.

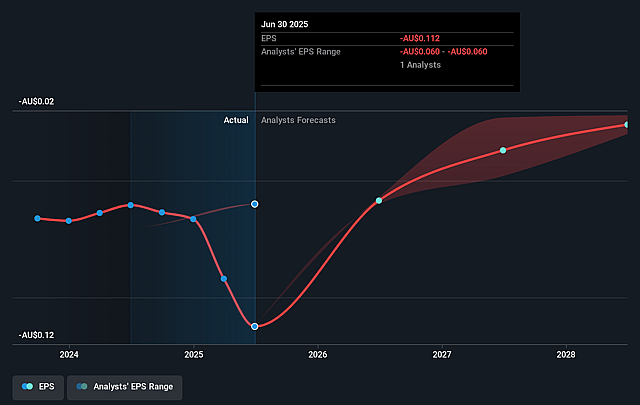

- If LARK Distilling's profit margin were to converge on the industry average, you could expect earnings to reach A$4.8 million (and earnings per share of A$0.04) by about September 2028, up from A$-11.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 23.9x on those 2028 earnings, up from -7.2x today. This future PE is lower than the current PE for the AU Beverage industry at 79.1x.

- Analysts expect the number of shares outstanding to grow by 0.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.48%, as per the Simply Wall St company report.

LARK Distilling Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- LARK's shift toward a distributor-led sales model and growing reliance on export markets may erode gross margins over time due to lower per-liter net sales and greater dependence on third-party partners, which could negatively impact overall profitability.

- The company's significant upfront and ongoing marketing expenditures, required to build global brand awareness and launch its restaged portfolio, will continue to put pressure on operating cash flow and may delay the achievement of sustainable earnings growth.

- LARK remains relatively small in scale compared to international spirits peers and remains highly exposed to Australian market performance, making it vulnerable to both regional economic downturns and an inability to achieve sufficient economies of scale to protect net margins against cost inflation.

- The Value of LARK's maturing whisky inventory is expected to face headwinds as stock acquired at higher fair value (from the Shene acquisition) is sold through in future years, reducing reported gross margins and potentially impacting earnings growth even as topline revenue expands.

- The company's long-term export strategy is susceptible to global trade disruption, intensifying competition from established international brands, and the risk of regulatory shifts or protectionist policies in key Asian markets, all of which could challenge revenue growth and sustained market penetration abroad.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for LARK Distilling is A$0.89, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of LARK Distilling's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$2.9, and the most bearish reporting a price target of just A$0.89.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be A$29.4 million, earnings will come to A$4.8 million, and it would be trading on a PE ratio of 23.9x, assuming you use a discount rate of 6.5%.

- Given the current share price of A$0.77, the bearish analyst price target of A$0.89 is 13.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.