Last Update 22 Jun 26

ROIV: 2026 Autoimmune Readouts And Regulatory Milestones Will Drive Repricing

Analysts have raised their average price target on Roivant Sciences to $39.04, citing updated models following recent earnings, pipeline data, and revised assumptions regarding the discount rate, profit margin, and forward P/E.

Analyst Commentary

Recent research updates on Roivant Sciences point to a more constructive stance from several firms, with higher price targets tied to refreshed models following quarterly results, pipeline data and changes to key assumptions such as discount rates, profit margins and forward P/E multiples.

Bullish Takeaways

- Bullish analysts are revising models after recent Q1 and fiscal Q4 reports, which feeds into higher price targets and reflects increased confidence in Roivant Sciences' ability to execute on its current plan.

- Updates to assumptions around profit margins and forward P/E are feeding into higher valuation ranges, suggesting that some analysts see room for the stock to better reflect Roivant's pipeline and commercial prospects.

- Several bullish analysts highlight the impact of recent pipeline updates, including brepocitinib's priority review status and proximity to its FDA action date, which they factor into higher price targets.

- TD Cowen and Citi emphasize IMVT-1402 data, with reported ACR20, ACR50 and ACR70 results viewed as supportive of Roivant Sciences' longer term growth potential and a source of multiple potential data catalysts.

Bearish Takeaways

- Neutral and more cautious analysts describe the current risk and reward as balanced, indicating that, at recent share levels, they see less room for upside without additional clinical or commercial validation.

- Some models retain more conservative assumptions for pipeline execution and market uptake, which tempers price targets relative to the more bullish group and reflects caution around timing and probability of success.

- The focus on adjusted forecasts, including un risk adjusting brepocitinib in response to regulatory milestones, underlines that a portion of Roivant Sciences' valuation is still tightly linked to binary clinical and regulatory events.

- While several firms lift targets, the presence of Neutral ratings signals that not all analysts are prepared to ascribe higher multiples until they see further evidence of consistent execution across the portfolio.

What’s in the News for Roivant Sciences

- Roivant Sciences reported a US$2.25b global settlement with Moderna, resolving pending patent infringement litigation, according to recent coverage.

- Positive clinical results were announced for IMVT-1402 in difficult to treat rheumatoid arthritis, highlighting progress in Roivant Sciences' autoimmune pipeline. (Source: recent news summary)

- The FDA granted Breakthrough Therapy Designation for brepocitinib in cutaneous sarcoidosis, recognizing the potential to address a serious inflammatory condition. (Source: recent news summary)

- Guggenheim raised its price target on Roivant Sciences to US$36 from US$30 and Citi raised its target to US$42, both citing recent fiscal Q4 earnings and pipeline updates. (Source: Guggenheim and Citi coverage)

- Roivant announced a new Phase 2b/3 clinical program for brepocitinib in lichen planopilaris and reported topline Phase 3 data for batoclimab in thyroid eye disease, alongside updates on late stage studies in dermatomyositis, non infectious uveitis and cutaneous sarcoidosis. (Source: company key developments)

Valuation Changes for Roivant Sciences

- Fair Value: Model fair value for Roivant Sciences is stable at $39.04 per share, with no change between the prior and updated estimates.

- Discount Rate: The discount rate has risen slightly from 7.55% to about 7.61%, indicating a modestly higher required return in the updated model.

- Revenue Growth: The long term revenue growth assumption remains very large and is effectively unchanged between the prior and updated forecasts.

- Profit Margin: The projected profit margin has edged down slightly from about 19.04% to about 18.98% in the refreshed assumptions.

- Future P/E: The forward P/E multiple has risen slightly from about 120.43x to about 120.99x in the updated valuation work.

Key Takeaways

- Successful clinical trials and strategic deals may improve revenue and net margins by focusing on high-value areas.

- Potential in-licensing and late-stage pipeline approvals could significantly enhance earnings and portfolio sales impact.

- Execution risks and competitive pressures could delay Roivant's earnings growth and profitability amidst high R&D costs and legal uncertainties.

Catalysts

About Roivant Sciences- A commercial-stage biopharmaceutical company, engages in the development and commercialization of medicines for inflammation and immunology areas.

- Roivant Sciences is focused on clinical trial execution with multiple ongoing trials, including late-stage programs like brepocitinib and batoclimab, which are expected to generate significant data readouts in the near future. Successful trial outcomes may positively impact future revenue streams.

- The company has completed the Dermavant deal, potentially allowing a greater focus on clinical execution and the upside of VTAMA. This could improve net margins by refocusing capital and operational efforts on higher-value areas.

- Roivant's late-stage pipeline, with potential approvals expected in the next couple of years, could lead to a projected $10 billion+ peak sales portfolio, significantly impacting earnings as these therapies are commercialized.

- Business development activities with negotiations for potential in-licensing of new programs are ongoing, representing opportunities for revenue growth through the expansion of their development-stage clinical pipeline.

- Roivant's commitment to returning capital to shareholders, including significant stock repurchases, is a catalyst for EPS growth, reflecting a potential undervaluation of current share prices if business fundamentals improve.

Roivant Sciences Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

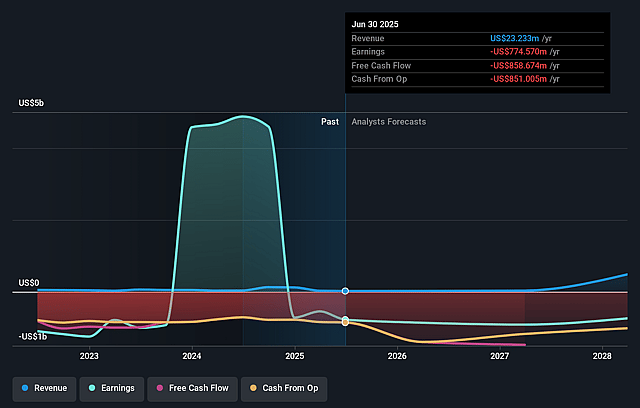

- Analysts are assuming Roivant Sciences's revenue will grow by 499.5% annually over the next 3 years.

- Analysts are not forecasting that Roivant Sciences will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Roivant Sciences's profit margin will increase from -3629.2% to the average US Biotechs industry of 19.0% in 3 years.

- If Roivant Sciences's profit margin were to converge on the industry average, you could expect earnings to reach $337.8 million (and earnings per share of $0.4) by about June 2029, up from -$299.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.2 billion in earnings, and the most bearish expecting $-1.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 121.1x on those 2029 earnings, up from -75.4x today. This future PE is greater than the current PE for the US Biotechs industry at 16.5x.

- Analysts expect the number of shares outstanding to grow by 5.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.61%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Roivant Sciences faces execution risks in clinical trial management across multiple ongoing trials, which could negatively affect their revenue and delay potential earnings growth.

- The competitive landscape, especially from well-established treatments like Humira, may limit Roivant's ability to capture market share quickly, impacting their expected revenue and potential profitability.

- There are legal uncertainties with ongoing LNP litigation, which could result in financial liabilities or distract management, thereby affecting net margins.

- Given the early development stage of many of Roivant’s drugs, there is a risk of clinical trial failures or delays, potentially impacting potential future revenues and profitability.

- The projected high R&D expenses and ongoing share repurchase program could strain Roivant’s financial resources, potentially impacting their cash flow and net income.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $39.04 for Roivant Sciences based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $45.0, and the most bearish reporting a price target of just $31.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.8 billion, earnings will come to $337.8 million, and it would be trading on a PE ratio of 121.1x, assuming you use a discount rate of 7.6%.

- Given the current share price of $31.43, the analyst price target of $39.04 is 19.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Roivant Sciences?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.