Last Update 06 Jul 26

Fair value Increased 39%ROIV: Late Stage Pipeline Progress Will Shape Future Upside Potential

Roivant Sciences' analyst fair value estimate has increased from $32.31 to $45.00 as analysts update their models following recent earnings, pipeline data, and revised assumptions on revenue growth, margins, and future P/E levels.

Analyst Commentary

Recent Street research on Roivant Sciences points to a cluster of higher fair value views, with several bullish analysts revisiting their models after earnings updates and new clinical data. The revisions center on Roivant's late stage pipeline progress, updated revenue and margin assumptions, and refreshed views on appropriate future P/E levels for the stock.

Across recent notes, bullish analysts highlight two main drivers behind their more optimistic stance. First, they are reacting to recent quarterly reports and pipeline updates, which have prompted adjustments to projected cash flows and profitability. Second, they point to specific drug assets such as IMVT-1402 and brepocitinib, where new data or regulatory progress has prompted revisions to risk weighting and timelines in their valuation work.

Major firms are also part of this shift. For example, JPMorgan increased its Roivant Sciences price target to US$40 and maintained an Overweight rating after updating its model following the Q1 report. Another global bank raised its price target to US$31.50 and kept a Neutral rating, stating that current share levels reflect what it views as a balanced risk and reward profile.

Other research houses moved their targets in smaller steps as key checkpoints were reached. One such move was a modest increase to US$29.50 linked to a decision to remove some risk discount from brepocitinib after the drug received a priority review and approached a Q3 FDA action date. Separately, several bullish analysts flagged IMVT-1402 as a key contributor to their higher price targets, citing Phase 2b data in difficult to treat rheumatoid arthritis, with ACR20 of 73%, ACR50 of 55%, and ACR70 of 36%.

Across these updates, the common thread is that analysts are fine tuning their Roivant Sciences models in response to new information rather than making wholesale changes based on macro views. Investors tracking these revisions can use them as one reference point on how professional forecasters currently think about valuation, execution risk, and the potential long term contribution from the company's pipeline.

Bullish Takeaways

- Several bullish analysts have raised Roivant Sciences price targets, indicating that updated earnings and pipeline inputs are feeding through to higher fair value assumptions for the stock.

- JPMorgan's move to a US$40 price target, alongside an Overweight rating, reflects confidence in Roivant's ability to execute on its Q1 driven outlook and supports the higher fair value estimate cited earlier.

- Positive Phase 2b IMVT-1402 data in difficult to treat rheumatoid arthritis, with strong ACR20, ACR50, and ACR70 readouts, is viewed as a key catalyst for Roivant's longer term growth potential and is explicitly tied to higher targets at some firms.

- The decision by one bank to remove some risk discount from brepocitinib after priority review status and proximity to the FDA decision shows how regulatory milestones can improve analysts' confidence in future cash flow contributions and thus support valuation for Roivant Sciences.

What’s in the News for Roivant Sciences

- Roivant Sciences was removed from the Russell 1000 Value-Defensive Index, according to index constituent updates.

- Roivant Sciences was also removed from the Russell 1000 Defensive Index, as part of the same index review process.

- From January 1, 2026 to March 31, 2026, Roivant Sciences repurchased 3,956,362 shares for US$109.73 million, completing a total of 4,226,362 shares for US$112.88 million under the buyback announced on August 11, 2025 (Key Developments).

Valuation Changes for Roivant Sciences

- Fair Value: The analyst fair value estimate for Roivant Sciences has risen from $32.31 to $45.00.

- Discount Rate: The discount rate used in analyst models has moved slightly higher from 7.44% to 7.58%.

- Revenue Growth: The revenue growth input is now very large compared with the prior figure, shifting from 395.76% to a higher multiple of that level.

- Net Profit Margin: The net profit margin assumption has increased from 11.80% to 29.88%.

- Future P/E: The future P/E multiple applied to Roivant Sciences has declined from 88.30x to 39.15x.

Catalysts

About Roivant Sciences

Roivant Sciences is a biopharmaceutical company advancing a diversified portfolio of late stage medicines targeting large, underserved immunology and specialty disease markets.

What are the underlying business or industry changes driving this perspective?

- Multiple pending late stage readouts and launches for brepocitinib and IMVT-1402 across dermatomyositis, noninfectious uveitis, Graves' disease and other autoimmune indications position Roivant to convert its broad clinical pipeline into a series of commercial assets over the next 36 months. This supports a potential step change in revenue and operating scale.

- The growing medical and regulatory focus on steroid sparing regimens in chronic autoimmune disease, exemplified by brepocitinib data showing deep responses with meaningful steroid reduction, creates an environment where differentiated oral agents can rapidly become standard of care. This may lift pricing power and long term net margins.

- Deep IgG lowering with IMVT-1402 that appears to translate into durable benefit in Graves' disease and potentially other antibody driven conditions offers a clear competitive position within the FcRn class. This may support premium positioning, higher peak sales per indication and improved earnings visibility.

- Expansion of diagnostic capabilities and physician awareness in under treated autoimmune populations such as dermatomyositis, Sjögren's and Graves' disease is enlarging the addressable market for targeted therapies. This could amplify the revenue impact of each successful launch in Roivant's portfolio.

- A balance sheet with 4.4 billion dollars of cash, no debt, and an authorized 500 million dollar capital return program provides Roivant with resources to fund its path to potential profitability, selectively in license additional programs and absorb launch costs without dilutive financing. This may support long term earnings growth and shareholder returns.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Roivant Sciences compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Roivant Sciences's revenue will grow by 686.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -3629.2% today to 29.9% in 3 years time.

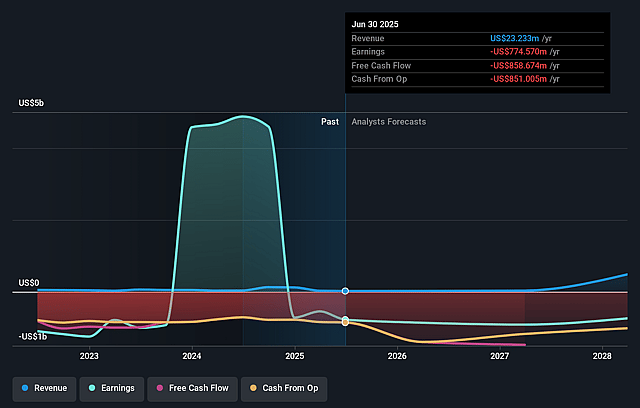

- The bullish analysts expect earnings to reach $1.2 billion (and earnings per share of $1.77) by about July 2029, up from -$299.8 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $-1.1 billion.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 39.2x on those 2029 earnings, up from -84.3x today. This future PE is greater than the current PE for the US Biotechs industry at 17.3x.

- The bullish analysts expect the number of shares outstanding to grow by 5.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.58%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The long term success of Roivant’s pipeline is heavily dependent on positive outcomes from multiple registrational and proof of concept trials across brepocitinib, IMVT-1402 and Pulmovant. Any late stage failures or merely modest efficacy versus existing standards of care could limit adoption and shrink the expected peak patient base, putting downward pressure on long term revenue and earnings growth.

- Rapidly intensifying competition in key autoimmune indications from established FcRn players and other novel mechanisms such as IGF 1R, IL 6 and CAR T approaches may erode Roivant’s hoped for first in class and best in class positioning. This could force more restrictive pricing or higher commercial spend to defend share, which would cap revenue upside and compress net margins over time.

- The evolving safety and tolerability expectations for chronic immunomodulatory therapies, particularly in large, earlier line populations like Graves’ disease and Sjögren’s, raise the risk that regulators or prescribers demand more conservative use or extensive post marketing data. This could slow uptake and extend payback periods on R and D, which would delay the path to sustainable positive earnings.

- While management expects the current 4.4 billion dollars cash balance to fund the pipeline to profitability, prolonged launch curves in rare and specialty indications, coupled with higher than anticipated commercial and litigation expenses, could exhaust balance sheet flexibility and necessitate future equity or debt raises at unfavorable terms. This could dilute shareholders and weaken earnings per share progression.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Roivant Sciences is $45.0, which represents up to two standard deviations above the consensus price target of $39.04. This valuation is based on what can be assumed as the expectations of Roivant Sciences's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $45.0, and the most bearish reporting a price target of just $31.5.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $4.0 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 39.2x, assuming you use a discount rate of 7.6%.

- Given the current share price of $35.13, the analyst price target of $45.0 is 21.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Roivant Sciences?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.