Last Update 25 Jun 26

Fair value Increased 0.32%TLS: Future Returns Will Rely On Buybacks Dividends And Pricing Power

Analysts have nudged their fair value estimate for Telstra Group slightly higher to about A$5.28 from A$5.27, reflecting updated assumptions around discount rates, margin potential and longer term valuation that align with a recent Neutral initiation carrying a A$5.50 price target.

What’s in the News for Telstra Group

- Telstra Group reported an 8.1% change in underlying NPAT for the first half of FY2026, alongside higher interim dividends, as part of its Connected Future 30 plan, according to recent earnings coverage.

- The company is focusing on expanding its 5G network and building out enterprise and government technology services as key pillars of its Connected Future 30 strategy. Market commentary highlights mobile business performance and demand for secure communications as core themes.

- Structural changes, including a partial sale of Telstra’s tower business Amplitel, have been used to free up capital and support growth in infrastructure based revenue streams, based on recent news reports.

- Telstra recently completed a A$1.25b share buyback at an average price of about A$5.08 per share, and commentators noted that the stock price saw a modest pullback after the program ended.

- From July 1, Telstra plans to lift prices on slower NBN internet plans by A$4 to A$5 a month while keeping higher speed plans unchanged, and introduce a A$4 monthly increase on mobile plans. Commentators expect this will affect average revenue per user in fiscal 2027.

Valuation Changes

- Fair Value: A$5.27 has shifted slightly to A$5.28 per share, reflecting a modest adjustment to the Telstra Group valuation model.

- Discount Rate: The discount rate moved from 7.14% to 7.00%, indicating a small change in the rate used to assess Telstra Group’s future cash flows.

- Revenue Growth: Assumed long term revenue growth changed from 2.53% to 2.49%, a very small adjustment to the forecast profile.

- Net Profit Margin: Assumed profit margin moved from 10.40% to 10.42%, reflecting a marginally higher profitability assumption for Telstra Group.

- Future P/E: The future P/E multiple shifted slightly from 28.18x to 28.13x, indicating a very small change in the valuation multiple applied.

Key Takeaways

- Investments in advanced networks, digital infrastructure, and automation position Telstra for sustained revenue growth, margin uplift, and expanding high-value digital service offerings.

- Strategic cost discipline and regulatory tailwinds support further operating leverage, diversified revenues, and improved shareholder returns through stronger cash flow.

- Shrinking high-margin revenues, rising competition, heavy network investments, and regulatory pressures undermine diversification, revenue growth, and long-term profitability.

Catalysts

About Telstra Group- Provides telecommunications and information services in Australia and internationally.

- Telstra's ongoing investment in expanding and modernizing its core mobile and fixed network-demonstrated by the rollout of 5G Advanced, intercity fibre projects, and satellite-to-mobile services-positions the company to benefit from surging mobile data consumption, proliferation of connected devices, and the anticipated explosion in demand from IoT, AR/VR, and cloud-enabled applications; these are likely to drive sustained revenue growth and justify premium pricing. (Impacts: Revenue, ARPU, long-term growth)

- Strategic focus on cost discipline, digital transformation, and AI-driven automation (including major staff reorganization, migration to a new digital stack, and rollout of AI initiatives) point to further operating leverage and margin improvement as automation scales and legacy cost structures are reduced, potentially supporting higher net margins and earnings. (Impacts: Net margins, EBITDA, earnings growth)

- Increased monetization of digital infrastructure-such as the intercity fibre network and towers (Amplitel)-plus the structural separation from InfraCo, is expected to unlock new high-margin revenue streams, improve capital efficiency, and underpin stronger free cash flow, enabling enhanced shareholder returns through dividends and buybacks. (Impacts: Free cash flow, net margins, shareholder returns)

- Rising enterprise and government demand for cloud, managed, and cybersecurity services, alongside Telstra's leadership in network quality, sovereign status, and digital transformation partnerships, should drive growth in higher-margin business and digital services, diversifying revenues beyond traditional connectivity. (Impacts: Revenue mix, margin expansion, earnings stability)

- Regulatory and government initiatives aimed at universal connectivity, particularly in regional and remote areas, alongside new spectrum allocations, offer Telstra opportunities to capture market share, benefit from public investment, and enlarge its customer base-all contributing to revenue stability and long-term growth prospects. (Impacts: Revenue growth, addressable market, long-term resilience)

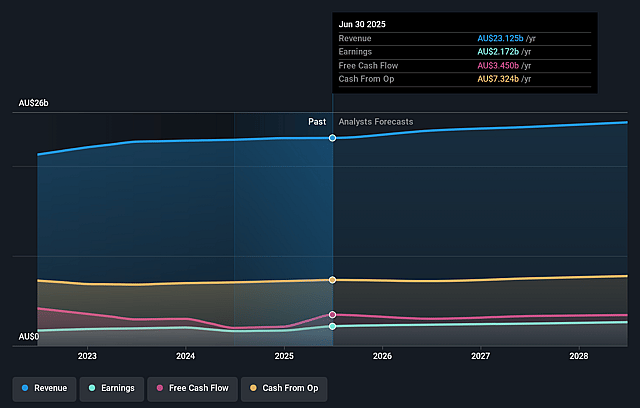

Telstra Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Telstra Group's revenue will grow by 2.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.8% today to 10.4% in 3 years time.

- Analysts expect earnings to reach A$2.6 billion (and earnings per share of A$0.23) by about June 2029, up from A$2.3 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as A$2.9 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 28.1x on those 2029 earnings, up from 25.1x today. This future PE is lower than the current PE for the AU Telecom industry at 56.8x.

- Analysts expect the number of shares outstanding to decline by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing transition away from legacy copper networks and NBN customer losses continues to pressure fixed-line and broadband revenues, while high-margin fixed revenues shrink, limiting both revenue growth and net margins long-term.

- Intensifying competition from MVNOs and digital-native providers in both prepaid and postpaid segments, along with a subdued broader mobile market, increases churn and ARPU compression risk, threatening future mobile revenue growth and margin expansion.

- Dependency on the Australian domestic market, with international EBITDA in decline due to restructuring and exit from NAS products, restricts diversification, leaving Telstra vulnerable to domestic economic downturns, regulatory changes, and earnings volatility.

- Ever-increasing network investment demands (5G/6G, intercity fiber, satellite-to-mobile) paired with only incremental revenue contributions from these projects in the near term risk outpacing revenue growth, pressuring free cash flow and returns on invested capital.

- Regulatory interventions, such as spectrum renewal uncertainty, forced wholesale access, price controls, and potential spectrum allocation changes, may reduce pricing power and profitability, further constraining long-term earnings and margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$5.28 for Telstra Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$5.6, and the most bearish reporting a price target of just A$4.6.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be A$24.9 billion, earnings will come to A$2.6 billion, and it would be trading on a PE ratio of 28.1x, assuming you use a discount rate of 7.0%.

- Given the current share price of A$5.14, the analyst price target of A$5.28 is 2.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Telstra Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.