Last Update 07 Jun 26

VPG: Humanoid Robotics Hype Will Stretch P/E And Raise Downside Risk

Narrative Update on Vishay Precision Group

The analyst price target for Vishay Precision Group has been raised to a triple digit level, supported by recent research that cites strong Q1 results, a book-to-bill of 1.21, and growing interest in the company as a profitable picks-and-shovels play on humanoid robotics and physical AI infrastructure themes.

Analyst Commentary

Recent Street research points to a sharp reset higher in expectations for Vishay Precision Group, with bullish analysts lifting price targets into a triple digit range following what they describe as strong Q1 results and guidance.

Bullish Takeaways

- Bullish analysts highlight the Q1 report as strong, which they see as supportive of higher valuation ranges and a wider potential upside case.

- A book to bill ratio of 1.21 is viewed as a key data point, suggesting to these analysts that orders are outpacing shipments and that the company may have visibility into future revenue execution.

- Analysts describe Vishay Precision Group as a profitable picks and shovels play on humanoid robotics and physical AI infrastructure themes, which they see as a supportive backdrop for longer term growth expectations.

- One bullish analyst characterizes the results and guidance as robust and states they are hard pressed to find meaningful issues, which they see as reinforcing confidence in management execution and earnings quality.

Bearish Takeaways

- Street commentary shared so far is largely positive, so potential risks are implied rather than explicitly detailed. These include the need to sustain current order momentum to support elevated price targets.

- Positioning Vishay Precision Group as a beneficiary of humanoid robotics and physical AI themes may raise expectations for growth, which could leave the stock exposed if those themes develop more slowly than the market anticipates.

- The move in price targets from the mid US$50s and US$60s to a triple digit range reflects a higher bar for future results. Any miss on execution or guidance could therefore pressure valuation.

- Strong guidance is mentioned without specific numbers, so investors still need to weigh how much of that optimism is already reflected in current pricing versus future delivery on that outlook.

What's in the News

- Vishay Precision Group announced that Executive Vice President and Chief Financial Officer William M. Clancy plans to retire on December 31, 2026, after a 38 year career with VPG and its predecessor company. The Board has started a search for his successor (company announcement, May 19, 2026).

- Recent commentary highlights that Mr. Clancy played a key role in establishing VPG as an independent publicly traded company and in building what the company describes as a strong financial foundation (company announcement, May 19, 2026).

- The company provided Q2 2026 earnings guidance, expecting net revenues in a range of US$85 million to US$90 million (company guidance, May 18, 2026).

- Vishay Precision Group stock recently reached an all time high of US$131.90, with reports linking the move to Q1 2026 results that came in ahead of earnings and revenue expectations (news reports, June 2, 2026).

- Other coverage notes that VPG shares previously surged more than 28% in a recent period, moving from prices in the low US$50s to above US$85, with commentary citing strong momentum and technical strength alongside upward revisions to earnings estimates (news reports, May 12, 2026).

Valuation Changes

- Fair Value: Model fair value remains at $94.67, with no change from the prior estimate.

- Discount Rate: The discount rate has risen slightly from 8.87% to 8.88%, reflecting a marginal adjustment to the required return assumption.

- Revenue Growth: The revenue growth assumption is effectively unchanged at about 8.28%.

- Net Profit Margin: The net profit margin assumption is effectively unchanged at about 10.50%.

- Future P/E: The future P/E multiple has risen slightly from 37.24x to 37.25x, indicating a very small shift in the valuation multiple applied to future earnings.

Key Takeaways

- Rising demand in automation, robotics, and new technology sectors positions the company for revenue growth and improved margins as these markets expand.

- Operational efficiencies, cost reductions, and pricing power are set to enhance profitability and support stable long-term earnings even during uncertainty.

- Dependence on customer production decisions, geopolitical risks, subdued key markets, margin compression, and restructuring challenges could drive earnings volatility and threaten long-term profitability.

Catalysts

About Vishay Precision Group- Engages in the precision measurement and sensing technologies business in the United States, Europe, Israel, Asia, and Canada.

- The strong sequential growth in bookings and a positive book-to-bill ratio across key segments indicate building demand for VPG's precision sensors and measurement products, positioning the company to benefit as global Industry 4.0 adoption and automation trends accelerate-likely supporting top-line revenue growth.

- New order momentum in cutting-edge markets such as humanoid robotics and beta installations for high-performance testing systems (e.g., UHTC for aerospace and energy) show VPG's entry into high-growth, high-margin niches, which can meaningfully expand gross margin and improve earnings quality as these end-markets scale.

- The company's focus on operational efficiencies-including a $5 million fixed cost reduction program and consolidation of production into lower-cost countries-is set to enhance margin leverage as volumes recover, which should lead to higher EBITDA and net margin upside as revenues rebound.

- Bookings related to electrification and precision agriculture, along with recent data center orders, validate VPG's exposure to secular shifts toward electrified vehicles, renewables, and infrastructure modernization-creating multi-year revenue tailwinds as these sectors continue expanding.

- Demonstrated pricing power, observed through strategic tariff-driven price adjustments and proprietary solutions, supports VPG's ability to maintain or raise margins even amid macroeconomic and geopolitical uncertainty, underpinning long-term earnings predictability.

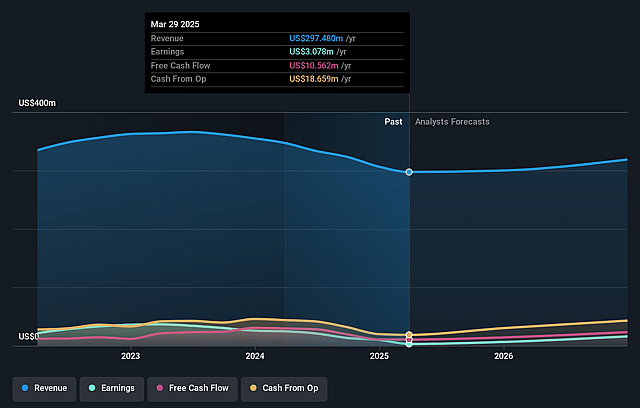

Vishay Precision Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Vishay Precision Group's revenue will grow by 8.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.8% today to 10.5% in 3 years time.

- Analysts expect earnings to reach $42.6 million (and earnings per share of $2.55) by about June 2029, up from $5.9 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $55.7 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 38.3x on those 2029 earnings, down from 264.2x today. This future PE is greater than the current PE for the US Electronic industry at 32.7x.

- Analysts expect the number of shares outstanding to grow by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.88%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's growth in the humanoid robotics market is highly dependent on the schedules and production ramp-up decisions of its customers, introducing significant revenue uncertainty and execution risk-potentially leading to volatile or delayed revenues if customer adoption or industry timelines slip.

- Exposure to tariffs, geopolitical tensions, and changing global trade policies has already negatively impacted gross margins, and further unpredictability in these areas could continue to pressure profitability and increase cost volatility, impacting both gross and net margins.

- The steel market and certain transportation end-markets remain subdued, with order variability and weak macro demand, leading to cyclical risk and vulnerability to downturns in these key sectors-which could constrain future revenue growth and create earnings volatility.

- Anticipated margin improvement from higher volumes in robotics or new applications may be undercut by the requirement for lower pricing in high-volume production scenarios, risking margin compression as new industries scale and threatening long-term profitability.

- While cost-saving programs and overseas production consolidation aim to improve efficiency, such restructuring also comes with risks of operational disruption, increased execution complexity, and potential quality or supply challenges-potentially impacting SG&A expense, capital allocation, and free cash flow if not managed effectively.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $94.67 for Vishay Precision Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $109.0, and the most bearish reporting a price target of just $77.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $406.1 million, earnings will come to $42.6 million, and it would be trading on a PE ratio of 38.3x, assuming you use a discount rate of 8.9%.

- Given the current share price of $117.51, the analyst price target of $94.67 is 24.1% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Vishay Precision Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.