Last Update 23 Mar 26

Fair value Increased 3.78%388: Higher Dividend And Earnings Outlook Will Support Future Resilience

Analysts have raised their price target on Hong Kong Exchanges and Clearing to HK$519 from about HK$500, citing updated assumptions. These include a slightly lower discount rate, a higher revenue growth outlook, a reduced profit margin and a higher future P/E multiple.

What's in the News

- The 2026 third extraordinary general meeting on April 2, 2026 will consider a change in registered capital and amendments to the Articles of Association, alongside completion of related industrial and commercial registration changes (company filing).

- A board meeting is scheduled for April 29, 2026 to approve the announcement of unaudited consolidated results for the three months ending March 31, 2026 (company filing).

- The board has declared an ordinary second interim dividend of HK$6.52 per share for the year ended December 31, 2025, compared with the 2024 second interim dividend of HK$4.90 per share. The dividend will be payable in cash to shareholders on the register on March 16, 2026, with expected payment on March 25, 2026 and an ex dividend date on March 11, 2026 (company filing).

- Earnings guidance for January 1, 2025 to December 31, 2025 indicates expected net profit attributable to owners of the parent between RMB 147.9940 million and RMB 180.1666 million, with net profit after deducting non recurring items expected to be between RMB 29.1898 million and RMB 39.5014 million (company guidance).

Valuation Changes

- Fair Value: updated from HK$500.33 to HK$519.24, representing a modest uplift in the analyst assessment of the shares.

- Discount Rate: revised from 8.11% to 7.80%, indicating slightly different assumptions about risk and required return.

- Revenue Growth: adjusted from 3.71% to 4.44%, reflecting a higher assumed growth rate for future revenues in HK$ terms.

- Net Profit Margin: moved from 68.29% to 61.05%, pointing to a lower assumed level of profitability on future HK$ earnings.

- Future P/E: updated from 37.35x to 41.14x, implying a higher valuation multiple applied to projected earnings.

Key Takeaways

- HKEX is leveraging Asia's economic rise and expanding global connectivity to strengthen its position, diversify revenues, and drive sustainable, higher-margin growth.

- Investments in fintech, product expansion, and platform upgrades increase operational efficiency, scalability, and earnings resilience amid shifting industry trends.

- Intensifying competition, regulatory and political risks, technological disruption, macroeconomic sensitivity, and rising costs threaten HKEX's core revenue streams and long-term profitability.

Catalysts

About Hong Kong Exchanges and Clearing- Owns and operates stock and futures exchanges, and related clearing houses in Hong Kong, the United Kingdom, and Mainland China.

- HKEX is poised to benefit materially from the continued growth of Asia as a global economic powerhouse, as evidenced by record trading volumes across multiple asset classes, a robust IPO pipeline with increasing international listings, and ongoing enhancements to fundraising infrastructure-supporting sustainable growth in revenue and profit.

- HKEX has firmly positioned itself as a global gateway between China and the world, with strong growth in Southbound and Northbound Connect volumes, expanding access for Mainland and international investors, and upcoming initiatives such as Southbound RMB counters and expanded product eligibility-likely to drive further increases in trading and listing-related revenues.

- Strategic investments in fintech, platform upgrades, and efficiency improvements-such as introducing severe weather trading, ongoing market microstructure enhancements, and studies into digital asset integration-should drive operational scalability and support long-term margin expansion.

- Product diversification via successful expansion into derivatives, ETPs, commodities, fixed income, and ESG-related offerings has created new recurring and higher-margin revenue streams, reducing reliance on traditional cash equities and enhancing overall earnings stability.

- Structural industry shifts toward increased ETF usage, passive investing, and heightened retail and institutional activity in Asia have translated into surging ETP and derivatives volumes (e.g., record 163% YoY growth in ETP turnover), supporting growth in transaction revenues and future-proofing the top line against cyclical volatility.

Hong Kong Exchanges and Clearing Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

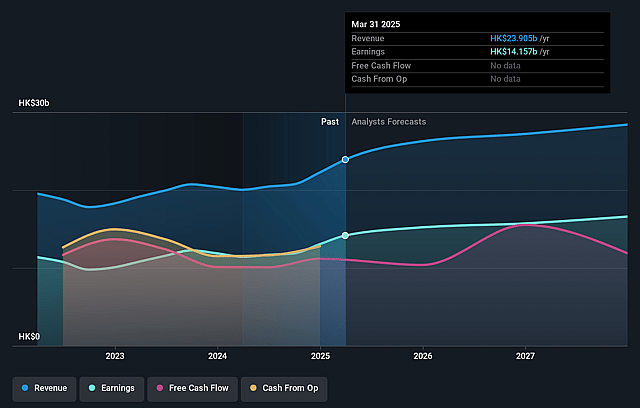

- Analysts are assuming Hong Kong Exchanges and Clearing's revenue will grow by 4.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 61.5% today to 61.0% in 3 years time.

- Analysts expect earnings to reach HK$20.1 billion (and earnings per share of HK$15.74) by about March 2029, up from HK$17.8 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting HK$22.8 billion in earnings, and the most bearish expecting HK$17.7 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 41.2x on those 2029 earnings, up from 28.2x today. This future PE is greater than the current PE for the HK Capital Markets industry at 16.7x.

- Analysts expect the number of shares outstanding to grow by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.8%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The rapid growth in onshore China's domestic exchanges and the reopening of the Asia IPO queue could intensify competition for listings, potentially diverting Mainland Chinese and regional IPOs away from HKEX, risking a slowdown in new listing revenue and affecting future top-line growth.

- HKEX's continued reliance on Southbound and Northbound capital flows exposes it to potential regulatory changes, capital controls, or political tensions between Mainland China and Hong Kong, which could materially dampen trading volumes and core revenue streams over the long term.

- The global shift toward digital assets and decentralized finance (DeFi), as evidenced by rapid advances in digital asset ecosystems and regulatory changes (e.g., stablecoin legislation in Hong Kong), may erode HKEX's traditional exchange infrastructure-if adaptation lags, this threatens long-term relevance and could displace significant trading and clearing revenues.

- Despite ongoing diversification, HKEX remains highly sensitive to macroeconomic conditions and short-term interest rates (e.g., HIBOR volatility impacting net investment income). Prolonged low interest rate environments and market downturns would pressure both net margins and earnings, given the cyclical nature of capital market activity.

- Increased operational and compliance costs-including rising staff and IT expenses, one-off regulatory fines, and mounting requirements under new global tax and regulatory regimes-could place persistent downward pressure on net margins, particularly if revenue growth slows or competitive fee compression accelerates.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of HK$519.24 for Hong Kong Exchanges and Clearing based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of HK$610.0, and the most bearish reporting a price target of just HK$390.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be HK$32.9 billion, earnings will come to HK$20.1 billion, and it would be trading on a PE ratio of 41.2x, assuming you use a discount rate of 7.8%.

- Given the current share price of HK$396.0, the analyst price target of HK$519.24 is 23.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Hong Kong Exchanges and Clearing?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.