Last Update 21 Apr 26

Fair value Increased 0.16%DE: Construction Momentum And Pending Large Ag Recovery Will Support Future Earnings

The analyst fair value estimate for Deere has increased by about $1 to $665, reflecting modest adjustments to growth, profit and P/E assumptions as analysts weigh recent price target increases against mixed views on valuation and the timing of an agriculture recovery.

Analyst Commentary

Recent research on Deere is divided, with many firms lifting price targets and talking up execution, while others focus on valuation risk and the timing of an agriculture recovery. The result is an active debate around how much of the potential earnings rebound is already reflected in the share price.

Bullish Takeaways

- Bullish analysts highlight Deere's recent Q1 results and raised guidance as evidence that execution across Small Ag & Turf and Construction & Forestry is tracking ahead of prior expectations. They see this as supportive of higher earnings power.

- Several price target moves into the US$700s and beyond are tied to views that Construction momentum and a stabilizing agriculture backdrop can support Deere's transition from negative to positive earnings revisions. These analysts associate that shift with a stronger equity case.

- Some research points to healthier Large Ag order trends and a potential bottoming in the agriculture market. They see this as a setup for Deere's equipment operations to contribute more meaningfully alongside Construction over time.

- JPMorgan and other bullish analysts refer to Deere's potential to deliver solid earnings growth in later years, and some explicitly raise mid cycle earnings assumptions. This flows into higher valuation frameworks and richer P/E multiples.

Bearish Takeaways

- Bearish analysts argue that the recent share price move and higher multiples already discount a full agriculture recovery and peak earnings several years out. In their view, this leaves limited room for error on execution or the cycle.

- Some research flags that Deere's valuation is well above prior peak averages, and that the stock is trading on extended P/E levels relative to its own history. They see this as a risk if farm incomes or crop prices do not improve as expected.

- There is caution that while the agriculture cycle may trough soon, a sustained recovery depends on better U.S. farmer income and crop prices. Timing therefore remains a key uncertainty for how quickly Large Ag can support growth.

- Neutral and cautious analysts also warn that recent strength in the shares could lead to profit taking, with valuation pushback increasing as Deere grows into its higher multiple without a clear, near term inflection in fundamentals.

What's in the News

- Deere reached a settlement agreement to resolve multidistrict "right to repair" litigation in U.S. federal court, with no finding of wrongdoing. The company plans to fund a class settlement pool and continue providing repair tools, manuals, and diagnostic software access to customers and third party service providers (Lawsuits & Legal Issues).

- John Deere and Tarter USA entered a manufacturing partnership to produce American made Frontier Flex Wing Rotary Cutters. Early dealer orders were above first year forecasts and production is based in Liberty, Kentucky, supported by automated fabrication and welding systems (Strategic Alliances).

- Deere increased its full fiscal year 2026 net income guidance to a range of US$4.5b to US$5.0b attributable to the company (Corporate Guidance, Raised).

- Bayer and John Deere introduced a new data connection that lets U.S. farmers send FieldView prescriptions wirelessly into John Deere Operations Center Work Plans. The feature is aimed at reducing manual file transfers and enabling two way data sharing for in field execution and post season analysis (Client Announcements).

- Deere reported that from November 3, 2025 to February 1, 2026 it repurchased 602,000 shares for US$293.01m, bringing total buybacks under the program launched in 2008 to 184,187,000 shares, or 54.2%, for US$31,380.4m (Buyback Tranche Update).

Valuation Changes

- Fair Value: The analyst fair value estimate has edged up from $664.01 to $665.10, reflecting only a very small adjustment.

- Discount Rate: The discount rate has risen slightly from 9.31% to 9.34%, a modest change in the risk assumption used in the model.

- Revenue Growth: The long term revenue growth input is essentially unchanged, moving from 58.91% to 58.92%.

- Net Profit Margin: The projected net profit margin has ticked up from 17.74% to 17.76%, indicating a marginal refinement to profitability expectations.

- Future P/E: The assumed future P/E multiple has moved slightly higher, from 27.45x to 27.49x, indicating a very small shift in the valuation multiple applied.

Key Takeaways

- Rapid adoption of advanced precision agriculture and automation tech is increasing higher-margin product sales and recurring software revenue for Deere.

- Global farm market improvements and disciplined inventory management position Deere for margin gains and accelerated earnings as agricultural demand rebounds.

- Rising tariffs, volatile demand, competitive pricing, and overreliance on incentives threaten Deere's profitability and margin sustainability amid cost pressures and market uncertainty.

Catalysts

About Deere- Engages in the manufacture and distribution of various equipment worldwide.

- Rapid adoption of Deere's precision agriculture and automation solutions (e.g., JDLink Boost, Precision Essentials bundles, See & Spray tech, and new automation features) is driving higher-value product sales and increased software engagement globally, positioning Deere to benefit from shifts toward high-efficiency, technology-enabled farming; this should lift both future revenue and net margins through higher-margin recurring software and data services.

- Global improvements in farm fundamentals outside North America-such as strong dairy profitability and crop yields in Europe, expanding acreage and profits in Brazil, and stable acreage with favorable credit in India-signal a demand recovery for advanced farm equipment, which could reaccelerate Deere's revenue and earnings as end markets inflect positively.

- Structural reductions in global inventory levels across all major product lines (e.g., 45% reduction in NA large tractor inventory, 50%+ down in Brazil) and a disciplined "build-to-retail" strategy allow Deere to respond rapidly to any upturn in demand, minimizing risk of production inefficiency and supporting margin improvement.

- Expansion and increased effectiveness of John Deere Financial, including innovative rate-buydown products for equipment purchasers even in a high-rate environment, are enabling customers to continue investing in equipment and supporting more resilient revenue streams and stable earnings in down cycles.

- Deere's continued investment in cost reductions, factory efficiency, and parts/service supports ongoing margin improvement, while announced price increases for 2026 models (2-4%) are expected to help offset tariff and input cost headwinds, supporting net margin and future earnings growth.

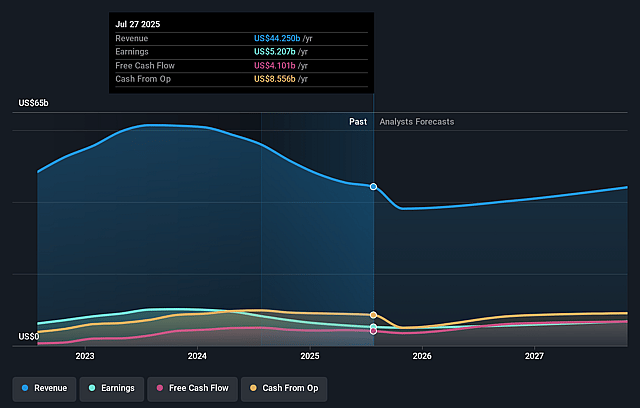

Deere Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Deere's revenue will remain fairly flat over the next 3 years.

- Analysts assume that profit margins will increase from 10.3% today to 17.8% in 3 years time.

- Analysts expect earnings to reach $8.4 billion (and earnings per share of $33.3) by about April 2029, up from $4.8 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $10.6 billion in earnings, and the most bearish expecting $6.2 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 27.6x on those 2029 earnings, down from 33.4x today. This future PE is greater than the current PE for the US Machinery industry at 27.5x.

- Analysts expect the number of shares outstanding to decline by 0.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.34%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Growing tariff and trade uncertainties, especially higher tariffs on Europe, India, and steel/aluminum, are materially increasing costs ($600 million forecast for FY25), which could compress operating margins and constrain future earnings if not fully offset by price realization.

- North America, Deere's largest market, is experiencing significant end-market volatility, marked by a projected 30% decline in large ag equipment sales for FY25, elevated used equipment inventories, high interest rates, and cautious sentiment-indicating risk of sustained pressure on revenue and market share if these headwinds persist.

- Aggressive competitive pricing, especially in construction and earthmoving equipment, is forcing Deere to deploy more incentives and accept negative price realization in segments; failure to reverse this trend could erode net margins and limit profitability over the long term.

- Over-reliance on incentives and financial services (e.g., John Deere Financial split rate tools and dealer pool funds) to stimulate demand in the face of high interest rates may prop up sales in the short-term but risks future revenue quality, credit losses, and margin sustainability if underlying demand does not recover.

- Growing costs from environmental, regulatory (tariff), and input inflation are requiring relentless execution on cost controls and supply chain adaptation; any misstep, inflation surprise, or inability to further reduce costs could materially impact net margins and ultimately earnings power.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $665.1 for Deere based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $793.0, and the most bearish reporting a price target of just $500.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $47.6 billion, earnings will come to $8.4 billion, and it would be trading on a PE ratio of 27.6x, assuming you use a discount rate of 9.3%.

- Given the current share price of $594.52, the analyst price target of $665.1 is 10.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Deere?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.