Last Update 22 Jun 26

Fair value Increased 0.44%IAU: Nevada Development Progress And Secured Funding Will Drive Future Upside

Analysts have slightly increased their fair value estimate for i-80 Gold to CA$4.53 from CA$4.51, citing updated work on discount rates and future P/E assumptions following recent bullish Street research coverage.

What's in the News

- Freedom Broker raised its price target on i-80 Gold Corp. to US$2.60 from US$2.00 and reiterated a Buy rating, citing stronger operational Q1 results tied to higher gold sales volumes and realized prices. (Source: Freedom Broker)

- The company reports that funding for the first and second stages of its Nevada development plan is fully secured, covering core projects at Granite Creek, Cove, Upper Archimedes and the Lone Tree complex. (Source: Freedom Broker)

- i-80 Gold produced 10,825 ounces of gold in the first quarter of 2026, compared with 5,240 ounces in the same period a year earlier. (Source: Company Q1 2026 operating results)

- Construction has commenced at Archimedes, the second underground project, with mineral resources reported at 436,000 indicated ounces at 7.6 grams per tonne and 988,000 inferred ounces at 7.3 grams per tonne as of 31 December 2025. (Source: Company Archimedes project update)

- Permitting for mining at Upper Archimedes is complete, around 1,200 meters of development has been finished, and the company continues to guide to first gold from Upper Archimedes in the third quarter of 2026 while advancing permitting for Lower Archimedes toward an estimated mid 2027 completion. (Source: Company Archimedes project update)

Valuation Changes for i-80 Gold

- Fair Value was updated marginally to CA$4.53 from CA$4.51, reflecting a small adjustment in the modelled estimate.

- The Discount Rate was adjusted slightly lower to 8.83% from 8.90%, which modestly affects the present value of projected cash flows.

- Revenue Growth was kept effectively unchanged at about 74.29%, indicating no material shift in the growth assumptions used.

- The Net Profit Margin was maintained at roughly 36.82%, with no meaningful revision to the long term profitability assumption.

- Future P/E was reduced moderately to 16.08x from 16.35x, implying a slightly lower valuation multiple applied to expected earnings.

Key Takeaways

- Increased production from Nevada projects, infrastructure upgrades, and high gold prices are set to strengthen revenue growth, cash flow, and margins.

- Continued exploration and in-house processing support long-term reserve growth and position the company to benefit from sector supply constraints.

- Heavy dependence on timely project execution, successful resource expansion, and cost control exposes the company to operational, financial, and regulatory risks that could impair future profitability.

Catalysts

About i-80 Gold- A mining company, explores for, develops, and produces gold, silver, and polymetallic deposits in the United States.

- The ramp-up of high-grade underground mining at Granite Creek, combined with unexpectedly higher oxide ore volumes and strong grades, positions the company for increasing gold production and improved revenue growth as resource modeling upgrades support future output targets.

- Progress towards commissioning the refurbished Lone Tree autoclave by 2027 (potentially earlier), which will drive much higher gold recovery rates (from ~55–60% to ~92%) and lower operating costs per ounce compared to third-party toll milling, should significantly expand net margins and operational cash flow.

- Persistent global inflation and ongoing geopolitical uncertainty are supporting elevated gold prices, benefiting realized revenues and creating a strong background for future earnings growth as i-80 Gold scales production.

- The company's extensive infill and resource expansion drilling across underexplored Nevada projects (including Cove and Mineral Point) could materially increase reserves and mine life, underpinning long-term earnings growth and reinforcing i-80 Gold's market valuation as a Nevada-focused mid-tier producer.

- Industry-wide underinvestment in new gold projects, coupled with i-80's strategic Nevada asset base and in-house processing infrastructure, positions the company to benefit from constrained sector-wide supply and potential long-term gold price appreciation, positively impacting both revenue and net margins.

i-80 Gold Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

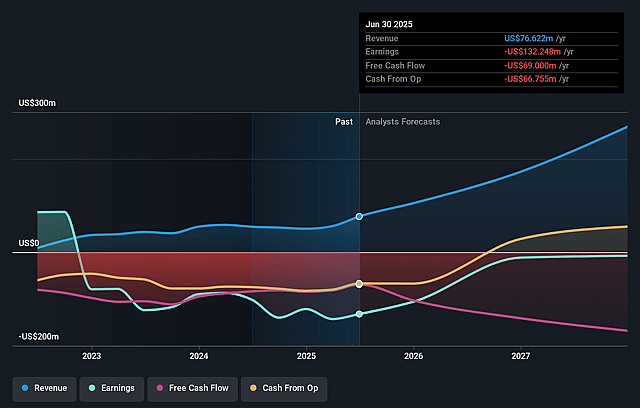

- Analysts are assuming i-80 Gold's revenue will grow by 74.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -176.9% today to 36.8% in 3 years time.

- Analysts expect earnings to reach $260.3 million (and earnings per share of $0.22) by about June 2029, up from -$236.2 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $445.0 million in earnings, and the most bearish expecting $219.9 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.1x on those 2029 earnings, up from -5.5x today. This future PE is greater than the current PE for the CA Metals and Mining industry at 14.2x.

- Analysts expect the number of shares outstanding to grow by 5.64% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.83%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on successful execution of multiple high-capex development projects (Granite Creek, Archimedes, Cove, Lone Tree, Mineral Point) introduces significant project execution and timeline risk, as any delays, cost overruns, or permitting setbacks could lead to higher-than-anticipated capital expenditures and impair free cash flow, net margins, or delay revenue growth.

- The company's future revenue growth and profitability are highly dependent on resource expansion, high-grade mineralization, and successful conversion of inferred resources to reserves in a geologically complex and competitive region; disappointing exploration results, lower-than-modeled grades, or technical mining challenges may reduce future gold output and impact revenues and long-term earnings.

- Ongoing and planned large-scale capital raises, including the need for a new $350–$400 million debt facility and potential asset sales/royalty deals, create ongoing shareholder dilution risk and higher debt servicing costs, which could suppress earnings per share and erode net margins if gold price or operating performance disappoints.

- The company is exposed to escalating regulatory, permitting, and environmental scrutiny, including the complexities of water management and expanding treatment infrastructure at Granite Creek; further delays or rising compliance costs from heightened ESG expectations could increase operating expenses, stretch project timelines, and constrain future profitability.

- Long-term secular shifts such as rising investor interest in alternative assets (like cryptocurrencies) and new technologies that could reduce gold's allure as a store of value, may weaken gold price appreciation over time, directly impacting i-80 Gold's revenue outlook and operating leverage.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$4.53 for i-80 Gold based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$6.59, and the most bearish reporting a price target of just CA$2.63.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $707.0 million, earnings will come to $260.3 million, and it would be trading on a PE ratio of 16.1x, assuming you use a discount rate of 8.8%.

- Given the current share price of CA$2.13, the analyst price target of CA$4.53 is 53.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on i-80 Gold?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.