Last Update 17 Jun 26

ZD: Asset Sales Buybacks And AI Use Will Balance Revenue Headwinds

What's in the News for Ziff Davis

- Ziff Davis reported a 1.9% year over year decline in Q1 2026 revenue, missing analyst expectations by 6.9%. A 13% drop in the Tech & Shopping segment contributed to weaker adjusted EBITDA, margins, and earnings per share. Source: company earnings reports summarized in recent news coverage dated May 8, 2026.

- Other Ziff Davis segments, including Gaming & Entertainment, Cybersecurity, Health & Wellness, and Martech, showed growth that partially offset Tech & Shopping weakness. This highlighted a mixed performance across the portfolio. Source: recent earnings coverage.

- Management is pursuing asset monetization, including a pending sale of the Connectivity business, and is accelerating share repurchases as part of a broader effort to focus on shareholder value and efficiency. Source: recent earnings coverage.

- The company is ramping up use of AI tools to support product development, operating leverage, and off platform monetization, and is positioning these initiatives as a key focus area. Source: recent earnings coverage.

- From January 1, 2026 to March 31, 2026, Ziff Davis repurchased 1,186,086 shares for US$46.35 million. This brought total buybacks under the August 10, 2020 authorization to 14,703,059 shares, or 33.58%, for US$798.72 million. Ziff Davis has also been removed from the NASDAQ Internet Index. Source: company buyback update and index constituent changes.

Valuation Changes for Ziff Davis

- Fair Value: The $48.67 fair value estimate for Ziff Davis is unchanged, reflecting a steady overall valuation view.

- Discount Rate: Discount rate assumptions have fallen slightly from 10.20% to 10.11%, indicating a modestly lower required return in the updated model.

- Revenue Growth: The expected revenue trend has improved, with the prior assumption of a 6.50% decline adjusted to a smaller projected decline of 4.35%.

- Net Profit Margin: Net profit margin assumptions have been trimmed from 5.59% to 5.22%, pointing to slightly lower expected profitability levels.

- Future P/E: The future P/E multiple has edged down from 28.58x to 28.51x. This is a very small adjustment to the valuation multiple applied to Ziff Davis earnings.

Key Takeaways

- Focus on digital content, SaaS, and high-margin verticals is driving recurring revenue growth and strengthening margins through proprietary brands and data assets.

- Strategic M&A, disciplined capital return, and advanced ad tech are accelerating diversification, platform scaling, and enhancing long-term shareholder value.

- Heavy dependence on acquisitions and industry shifts threaten organic growth, advertising revenue, and overall profitability amidst evolving digital and AI-driven media landscapes.

Catalysts

About Ziff Davis- Operates as a digital media and internet company in the United States and internationally.

- Ziff Davis is benefiting from the growing demand for digital content, cloud-based solutions, and recurring subscription services, as demonstrated by double-digit organic growth across Health & Wellness, Connectivity, and strong SaaS uptake, which supports sustained revenue and margin expansion from recurring business models.

- The company is capitalizing on a significant shift toward data-driven, performance-oriented digital advertising and e-commerce, as evidenced by its AI-enhanced moment of influence targeting platform and large, privacy-protected first-party data assets, likely to drive higher digital ad yields and improved advertiser spend, boosting ad revenue growth.

- Strategic focus on premium, high-margin verticals (health, gaming, cybersecurity) and the monetization of proprietary brands-such as CNET, Everyday Health, IGN, and Lose It!-is delivering both pricing power and margin resilience, positioning the company for further net margin and EBITDA expansion.

- Ziff Davis's disciplined M&A approach, with ongoing tuck-in acquisitions funded by a strong balance sheet, is actively diversifying revenues and accelerating growth across verticals, directly contributing to future earnings and margin growth through operational synergies and platform scaling.

- Sustained and substantial share repurchases-nearly 10% of outstanding shares in the past year-combined with organic and inorganic growth, enhance EPS accretion and shareholder value, highlighting management's confidence in undervaluation and future earnings growth.

Ziff Davis Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Ziff Davis's revenue will decrease by 4.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.5% today to 5.2% in 3 years time.

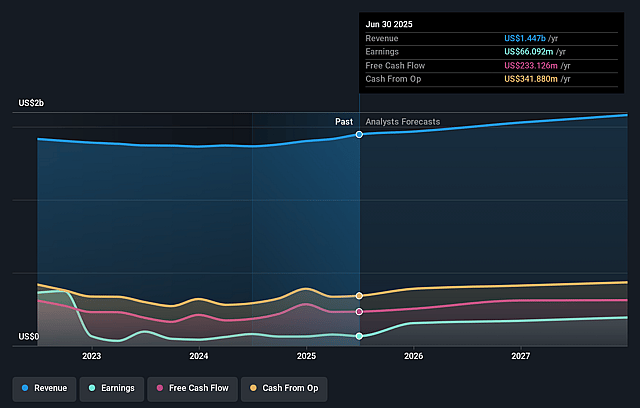

- Analysts expect earnings to reach $66.1 million (and earnings per share of $2.01) by about June 2029, up from $36.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 29.1x on those 2029 earnings, down from 46.1x today. This future PE is greater than the current PE for the US Interactive Media and Services industry at 13.1x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on inorganic (acquisition-driven) growth, as roughly half of Ziff Davis's intended double-digit revenue growth is expected to come from M&A, creating ongoing risk of integration challenges, overpayment, and potential pressure on net margins and earnings if acquisition synergies fall short.

- Exposure to long-term digital advertising headwinds, including increasing adoption of privacy regulations, the global proliferation of ad-blocking technologies, and a continued shift of advertising budgets to walled gardens and social platforms-challenges that could structurally reduce advertising effectiveness and ultimately compress Ziff Davis's advertising-related revenue and margins.

- The risk posed by accelerated AI and large-language-model-driven content aggregation (such as zero-click search and AI-powered overviews), which disrupts traditional web traffic and threatens the value of premium owned-and-operated content properties-potentially undermining Ziff Davis's traffic, user engagement, and revenue base over time.

- Weakness and stagnation in certain core segments and brands, specifically Tech & Shopping's Offers brand (placed into "managed decline") and B2B technology, as well as lumpy or slowing performance in Cybersecurity & Martech, pointing to dependence on continual acquisition to prevent revenue plateaus and raising questions about the sustainability of organic growth, revenue, and net margins.

- Ongoing industry-wide challenges from declining desktop web traffic in favor of closed mobile/app environments and intensifying digital media consolidation by major tech firms, which can diminish Ziff Davis's audience reach, erode its negotiating power with advertisers, and put long-term pressure on both revenue generation and earnings capacity.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $48.67 for Ziff Davis based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $61.0, and the most bearish reporting a price target of just $30.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.3 billion, earnings will come to $66.1 million, and it would be trading on a PE ratio of 29.1x, assuming you use a discount rate of 10.1%.

- Given the current share price of $45.97, the analyst price target of $48.67 is 5.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Ziff Davis?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.