Last Update 16 Jun 26

Fair value Increased 75%VRT: AI Data Center Backlog Strength Will Likely Outrun Future Earnings Power

What's in the News

- Vertiv Holdings is closely tied to the AI infrastructure buildout, with recent reports highlighting a $15b order backlog and operating margins above 20%, alongside strong free cash flow and growing recognition through S&P 500 inclusion and investment grade credit ratings (source: Vertiv Holdings Reports Strong Growth and Expanding Margins Amid AI Infrastructure Boom).

- The company has acquired Strategic Thermal Labs LLC to deepen its liquid cooling capabilities for high density AI and high performance computing data centers, supporting cold plate design, server side liquid cooling and high density thermal validation, and reinforcing Vertiv's role in major AI data center projects (source: Vertiv Acquires Strategic Thermal Labs to Boost Liquid Cooling for AI Data Centers).

- Vertiv shares have seen sharp moves in May 2026, with analysts pointing to strong earnings growth expectations and multiple Buy ratings. Some investors also flag high valuation metrics such as a forward P/E near 53 and insider selling of about US$123.4m over three months as areas to watch (source: Vertiv Holdings Shares Surge Amid Strong Growth Prospects Despite Overvaluation and Insider Selling).

- At its May 2026 Investor Conference, Vertiv highlighted 23% organic revenue growth in Q1 2026, a backlog of US$12.45b and operating margins above 20%. The company also outlined plans for AI focused bolt on acquisitions in the US$750m to US$1b range and expanded use of digital twin tools through its SmartRun platform with NVIDIA Omniverse DSX (source: Vertiv Hosts Investor Conference Highlighting Strong AI Driven Growth and Strategic Outlook).

- Vertiv is investing about US$50m to expand manufacturing capacity in Ohio, targeting roughly 45% higher output for liquid cooling and thermal systems and adding hundreds of jobs through 2029. This reflects ongoing demand for power and thermal management tied to AI and high density computing (source: Vertiv Holdings Expands Ohio Operations Amid Strong AI Driven Demand and Upgraded Price Targets).

Valuation Changes

- Fair Value: revised higher from $155.12 to $271.16, representing a large uplift in the Vertiv Holdings Co valuation framework.

- Discount Rate: adjusted slightly higher from 9.28% to 9.44%, implying a modestly higher required return for Vertiv Holdings.

- Revenue Growth: updated from 17.16% to 25.58%, reflecting meaningfully stronger growth assumptions in the Vertiv Holdings model.

- Net Profit Margin: raised from 15.91% to 19.07%, indicating higher expected profitability on future Vertiv Holdings revenue.

- Future P/E: increased from 31.57x to 33.85x, pointing to a somewhat richer multiple applied to Vertiv Holdings earnings in the updated valuation.

Key Takeaways

- Vertiv's pricing strategies and supply chain realignment aim to mitigate tariff impacts, risking margins if not achieved by year-end.

- Investments in R&D and capacity support growth amid digital advancements, balancing regional performance challenges with strong order pipelines.

- Geopolitical and tariff uncertainties, coupled with execution risks in new market segments, threaten Vertiv's revenue, growth, and operating margins.

Catalysts

About Vertiv Holdings Co- Designs, manufactures, and services critical digital infrastructure technologies and life cycle services for data centers, communication networks, and commercial and industrial environments in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

- The company is focused on mitigating tariff impacts through pricing strategies and supply chain realignment, which may affect net margins unless fully successful by the year's end.

- Vertiv's substantial investment in R&D, capacity, and operational excellence is expected to support future revenue growth despite tariff challenges and geopolitical uncertainty.

- The ongoing digital revolution, AI adoption, and robust demand for data centers are anticipated to drive future revenue growth, capitalizing on Vertiv's strong market position and execution capabilities.

- Management's commitment to operational flexibility and supply chain resilience suggests potential stabilization of earnings, even amidst tariff volatility.

- Challenges in EMEA performance, relative to stronger growth in the Americas and APAC, require attention but are counterbalanced by expanding order pipelines and backlogs, which indicate future organic revenue growth.

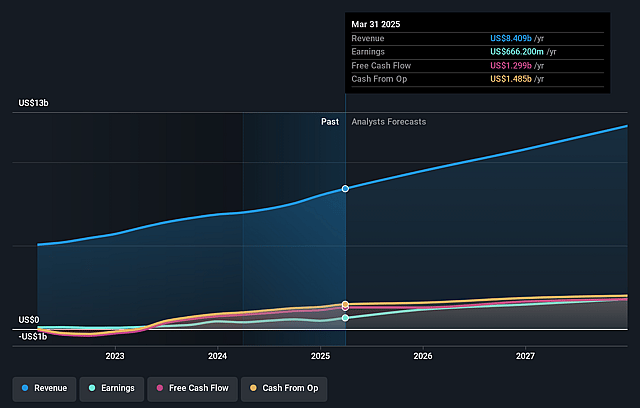

Vertiv Holdings Co Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Vertiv Holdings Co compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Vertiv Holdings Co's revenue will grow by 25.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 14.4% today to 19.1% in 3 years time.

- The bearish analysts expect earnings to reach $4.1 billion (and earnings per share of $10.31) by about June 2029, up from $1.6 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $5.1 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 33.9x on those 2029 earnings, down from 76.9x today. This future PE is lower than the current PE for the US Electrical industry at 38.6x.

- The bearish analysts expect the number of shares outstanding to grow by 0.59% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.44%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The dynamic and fluid nature of the tariff situation presents a risk to Vertiv's revenues, as the company is exposed to potential increases in costs that could impact operating margins.

- Uncertainty around geopolitical and regulatory environments, especially in regions like EMEA, could hinder market growth and affect overall revenue projections.

- The need for tariff mitigation through supply chain reconfiguration and pricing actions implies execution risks that could lead to unexpected costs, impacting net margins.

- The dependency on a few major customers in the data center market, including potential slowdowns in specific segments, could adversely affect Vertiv’s revenue and growth forecasts.

- Delays or challenges in the execution of new product introductions or expansions into new segments, such as those involving AI or hyperscale infrastructure, could impact sales growth and operating performance.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Vertiv Holdings Co is $271.16, which represents up to two standard deviations below the consensus price target of $378.31. This valuation is based on what can be assumed as the expectations of Vertiv Holdings Co's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $500.0, and the most bearish reporting a price target of just $236.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $21.5 billion, earnings will come to $4.1 billion, and it would be trading on a PE ratio of 33.9x, assuming you use a discount rate of 9.4%.

- Given the current share price of $311.93, the analyst price target of $271.16 is 15.0% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Vertiv Holdings Co?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.