Last Update 06 Feb 26

Fair value Increased 68%VRT: AI Data Center Momentum Will Likely Outrun Future Earnings Power

Analysts have raised their price target for Vertiv Holdings Co from US$92.18 to US$155.12, pointing to updated assumptions around higher projected revenue growth, slightly stronger profit margins, and a higher future P/E multiple as key drivers of the new fair value range.

What's in the News

- Vertiv launched Vertiv Next Predict, an AI-powered managed service aimed at shifting data center maintenance toward predictive analytics, using AI-based anomaly detection, risk assessment, and prescriptive actions across power, cooling, and IT systems (Product-Related Announcements).

- Vertiv Next Predict is positioned as part of an integrated AI infrastructure portfolio, with support for a wide range of Vertiv power and cooling platforms, including battery energy storage solutions and liquid cooling components. It is described as scalable for future data center technologies (Product-Related Announcements).

- Vertiv introduced new configurations of the Vertiv MegaMod HDX, a prefabricated power and liquid cooling solution targeted at AI and high-performance computing setups, with module options supporting up to 10 MW of power capacity and rack densities of more than 100 kW per rack (Product-Related Announcements).

- Hut 8 Corp. announced that Jacobs Solutions is engaged as EPCM partner in collaboration with Vertiv for a project that Hut 8 believes can become a benchmark for AI infrastructure, highlighting Vertiv as a key collaborator in the buildout (Client Announcements).

- Vertiv and Caterpillar Inc., along with Solar Turbines, signed a memorandum of understanding to combine Vertiv power and cooling offerings with Caterpillar power generation solutions. The collaboration targets pre-designed, modular architectures for data centers that aim to shorten deployment timelines and address on-site energy needs (Strategic Alliances).

Valuation Changes

- Fair Value: updated from US$92.18 to US$155.12, representing a large upward reset in the modelled price range.

- Discount Rate: moved from 7.79% to 9.28%, indicating a higher required return applied to future cash flows.

- Revenue Growth: revised from 10.65% to 17.16%, reflecting stronger projected top line expansion in the model.

- Net Profit Margin: adjusted from 14.80% to 15.91%, indicating slightly higher expected profitability.

- Future P/E: updated from 27.53x to 31.57x, pointing to a higher assumed valuation multiple for the business.

Key Takeaways

- Vertiv's pricing strategies and supply chain realignment aim to mitigate tariff impacts, risking margins if not achieved by year-end.

- Investments in R&D and capacity support growth amid digital advancements, balancing regional performance challenges with strong order pipelines.

- Geopolitical and tariff uncertainties, coupled with execution risks in new market segments, threaten Vertiv's revenue, growth, and operating margins.

Catalysts

About Vertiv Holdings Co- Designs, manufactures, and services critical digital infrastructure technologies and life cycle services for data centers, communication networks, and commercial and industrial environments in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

- The company is focused on mitigating tariff impacts through pricing strategies and supply chain realignment, which may affect net margins unless fully successful by the year's end.

- Vertiv's substantial investment in R&D, capacity, and operational excellence is expected to support future revenue growth despite tariff challenges and geopolitical uncertainty.

- The ongoing digital revolution, AI adoption, and robust demand for data centers are anticipated to drive future revenue growth, capitalizing on Vertiv's strong market position and execution capabilities.

- Management's commitment to operational flexibility and supply chain resilience suggests potential stabilization of earnings, even amidst tariff volatility.

- Challenges in EMEA performance, relative to stronger growth in the Americas and APAC, require attention but are counterbalanced by expanding order pipelines and backlogs, which indicate future organic revenue growth.

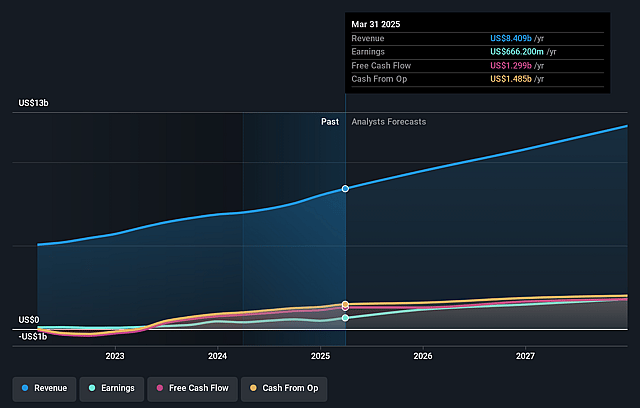

Vertiv Holdings Co Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Vertiv Holdings Co compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Vertiv Holdings Co's revenue will grow by 10.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 7.9% today to 14.8% in 3 years time.

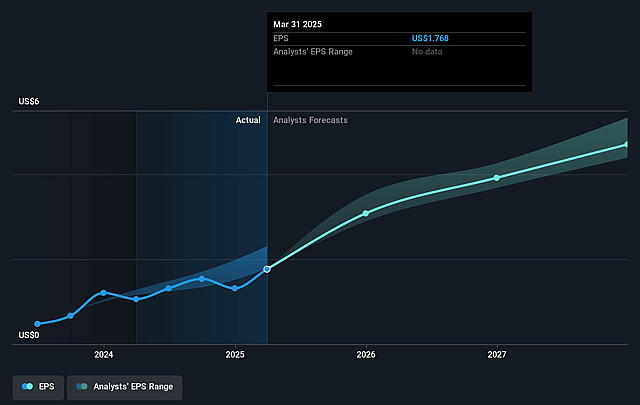

- The bearish analysts expect earnings to reach $1.7 billion (and earnings per share of $4.39) by about April 2028, up from $666.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 27.5x on those 2028 earnings, down from 48.8x today. This future PE is greater than the current PE for the US Electrical industry at 22.8x.

- Analysts expect the number of shares outstanding to grow by 1.81% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.79%, as per the Simply Wall St company report.

Vertiv Holdings Co Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The dynamic and fluid nature of the tariff situation presents a risk to Vertiv's revenues, as the company is exposed to potential increases in costs that could impact operating margins.

- Uncertainty around geopolitical and regulatory environments, especially in regions like EMEA, could hinder market growth and affect overall revenue projections.

- The need for tariff mitigation through supply chain reconfiguration and pricing actions implies execution risks that could lead to unexpected costs, impacting net margins.

- The dependency on a few major customers in the data center market, including potential slowdowns in specific segments, could adversely affect Vertiv’s revenue and growth forecasts.

- Delays or challenges in the execution of new product introductions or expansions into new segments, such as those involving AI or hyperscale infrastructure, could impact sales growth and operating performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Vertiv Holdings Co is $92.18, which represents one standard deviation below the consensus price target of $108.14. This valuation is based on what can be assumed as the expectations of Vertiv Holdings Co's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $135.0, and the most bearish reporting a price target of just $73.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $11.4 billion, earnings will come to $1.7 billion, and it would be trading on a PE ratio of 27.5x, assuming you use a discount rate of 7.8%.

- Given the current share price of $85.38, the bearish analyst price target of $92.18 is 7.4% higher. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Vertiv Holdings Co?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.