Last Update 23 Jun 26

Fair value Decreased 0.53%FRPT: New Production Technology Will Drive Margins And Post 2026 Expectations

Freshpet's updated analyst price target reflects a small downward adjustment of about $0.44, as analysts balance slightly higher revenue growth assumptions with softer projected profit margins and a higher future P/E multiple. This outlook is informed by a mix of recent target cuts and upgrades across the Street.

Analyst Commentary

Recent research on Freshpet shows a split view, with several price target cuts sitting alongside a few upgrades and small upward revisions. For you as an investor, the key themes are how much confidence analysts place in Freshpet's execution and what they are willing to pay for that through target P/E multiples.

Bullish Takeaways

- Bullish analysts have raised price targets or upgraded Freshpet, which signals confidence that the company can execute on its growth plans and justify a richer valuation over time.

- Recent upgrades, including a more positive stance from JPMorgan, suggest some see Freshpet's current share price as not fully reflecting its potential to scale its business model.

- Higher targets from bullish analysts point to a willingness to underwrite a higher future P/E multiple. This indicates comfort with the trade off between near term margin pressure and longer term growth.

- Supportive commentary implies that if Freshpet delivers on revenue and operational goals, there could be room for the stock to close the gap between current trading levels and these optimistic targets.

Bearish Takeaways

- Bearish analysts have lowered price targets by amounts such as US$5 to US$14, reflecting caution around how much investors should pay for Freshpet given its profit margin profile.

- Multiple target cuts across the Street point to concerns that execution risks, such as cost control or scaling challenges, could limit the upside that a higher P/E multiple implies.

- Some reductions in targets, including from JPMorgan at an earlier stage, suggest that even firms that see long term appeal may still factor in a more conservative valuation path.

- The cluster of recent cuts indicates that, for more cautious analysts, Freshpet needs to show clearer progress on profitability before they are comfortable with materially higher price targets.

What's in the News for Freshpet

- Freshpet shares rose 5.3% after Piper Sandler reaffirmed its Overweight rating and US$87 price target, citing discussions with CFO John O'Connor that addressed competition concerns and highlighted marketing and distribution strengths (source: Piper Sandler coverage).

- Piper Sandler pointed to Freshpet's new production technology as a potential driver of profit margin improvement and cost savings through large scale purchasing, supporting its view of the stock's value at current trading levels (source: Piper Sandler coverage).

- Freshpet launched a long term brand platform titled "Better Food for Your Better Half" with an integrated "Kitchen Conversations" advertising campaign developed with agency Terri & Sandy, focusing on the bond between pet owners and pets and the role of high quality fresh food.

- The "Kitchen Conversations" campaign features multiple ad spots that link everyday kitchen moments with Freshpet's approach to fresh, real food made from simple, recognizable ingredients such as fresh meats, vegetables, fruits, and whole grains, steam cooked at lower temperatures.

- Freshpet plans to run the "Kitchen Conversations" campaign across linear and streaming TV and social platforms, aiming to reinforce its differentiated positioning in fresh pet food and the importance of mealtime rituals for pets and owners.

Valuation Changes for Freshpet

- Fair Value: the updated estimate moved slightly lower from $82.38 to $81.94, a reduction of about 0.5%.

- Discount Rate: held effectively flat at 7.11%, indicating no material change in the required return used in the model.

- Revenue Growth: the projected rate is modestly higher, shifting from 8.81% to 8.88%, which assumes slightly stronger top line expansion for Freshpet.

- Net Profit Margin: the projection moved lower from 9.19% to 8.64%, indicating a softer margin profile in the updated assumptions.

- Future P/E: the assumed valuation multiple increased from 37.64x to 39.71x, pointing to a higher price that analysts are willing to ascribe to each dollar of Freshpet's expected earnings.

Key Takeaways

- Enhanced production efficiency, digital expansion, and health-focused innovation are improving Freshpet's margins, competitive position, and prospects for top-line growth.

- Strong brand loyalty and retailer partnerships support sustainable market share gains as industry trends favor premium, fresh pet food and omni-channel purchasing.

- Slowing pet adoption, cautious consumer spending, increased competition, adjusted long-term targets, and high operating costs raise concerns about Freshpet's future growth and profitability.

Catalysts

About Freshpet- Manufactures, distributes, and markets natural fresh meals and treats for dogs and cats in the United States, Canada, and Europe.

- Operational improvements and implementation of new production technologies at Ennis and other facilities have driven higher yields, quality, and throughput, leading to a significant reduction in CapEx ($100 million less over 2025-26) and enhanced gross/EBITDA margins, setting the business up for improving net earnings and cash generation.

- Expansion of digital channels (digital up 40% YoY, now 13% of sales) and entry into the club channel (test expanded to 125 stores with further expected growth) positions Freshpet to capture the ongoing shift in consumer purchasing behavior toward online and omni-channel retail, likely boosting future revenues and household penetration.

- Consumer focus on ingredient transparency, nutrition, and less-processed foods is being leveraged through targeted health-forward marketing campaigns and new product innovation (e.g., complete nutrition bag, multipacks), enhancing competitive differentiation, supporting pricing power, and growing buy rates-key drivers for top-line growth.

- Despite macro headwinds, Freshpet's brand loyalty (MVPs up 18% YoY, represent 70% of sales), high customer retention, and strong relationships with retailers provide a foundation for sustainable market share gains within the premium fresh pet food segment, supporting both revenue and margin growth.

- As larger competitors invest in category awareness and the premium/fresh pet food segment expands, Freshpet-being the category pioneer with differentiated, health-focused offerings, growing capacity, and efficiency advantages-is well-positioned to capitalize on the long-term humanization and health trends in pet ownership, driving outsized revenue and margin growth versus the broader category.

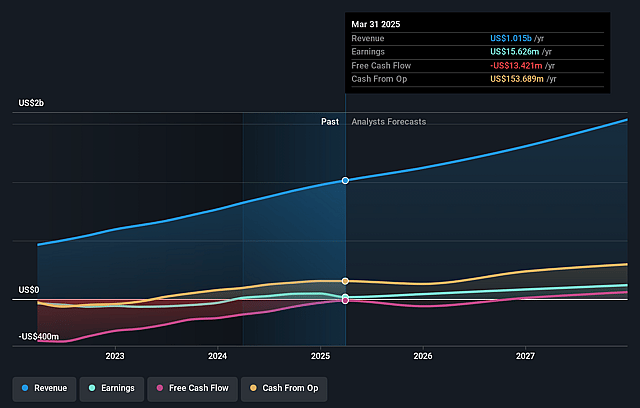

Freshpet Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Freshpet's revenue will grow by 8.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 17.6% today to 8.6% in 3 years time.

- Analysts expect earnings to reach $126.8 million (and earnings per share of $2.26) by about June 2029, down from $200.3 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $104.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 39.9x on those 2029 earnings, up from 13.5x today. This future PE is greater than the current PE for the US Food industry at 15.5x.

- Analysts expect the number of shares outstanding to grow by 0.74% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Slowing category growth for dog food, exacerbated by economic pressures (e.g., return-to-office mandates, high housing costs, lingering post-pandemic effects), has led to a weakened rate of new dog adoptions and pet replacements, which could limit Freshpet's long-term revenue growth if the dog population does not rebound as forecasted.

- Ongoing consumer hesitation to trade up to premium products, especially among more price-sensitive demographics during economic uncertainty or inflation, threatens Freshpet's ability to drive household penetration and increase buy rates, which may impact both revenue and profit margins.

- Heightened competitive pressure-particularly from entrenched brands like Blue Buffalo and others investing heavily in the fresh segment-poses a risk to Freshpet's market share and pricing power, potentially resulting in slower top-line growth and compressed net margins over time.

- The company's removal of its ambitious 2027 net sales and household penetration targets signals a recognition of structurally lower category growth, which may lead to investor skepticism regarding the company's long-term earnings trajectory and market expansion potential.

- Persistent high capital requirements for refrigeration, manufacturing, and logistics infrastructure, along with variable exposure to tariff and input cost increases, could constrain free cash flow and erode net margins if operational efficiencies and new technologies do not offset these expenses as projected.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $81.94 for Freshpet based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $104.0, and the most bearish reporting a price target of just $62.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.5 billion, earnings will come to $126.8 million, and it would be trading on a PE ratio of 39.9x, assuming you use a discount rate of 7.1%.

- Given the current share price of $55.01, the analyst price target of $81.94 is 32.9% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Freshpet?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.