Last Update 02 Jun 26

Fair value Increased 0.63%NPCE: Strong Prescriber Momentum And 2026 Guidance Will Support More Optimistic Outlook

Narrative Update on NeuroPace

The analyst price target for NeuroPace has moved from $19 to $20. Analysts point to stronger prescriber and patient pipeline trends and higher 2026 revenue guidance for the core RNS business as key drivers of this change.

Analyst Commentary

Analysts are reacting to the updated outlook for NeuroPace with a focus on the core RNS business, the prescriber base and the company’s medium term revenue targets. The shift in the price target to $20 reflects how the Street is weighing execution risk against the growth profile implied by management’s guidance.

Bullish Takeaways

- Bullish analysts highlight new all time highs in active prescribers, accounts and patient pipeline as evidence that demand for the core RNS offering is broadening, which they see as supportive of higher revenue over time.

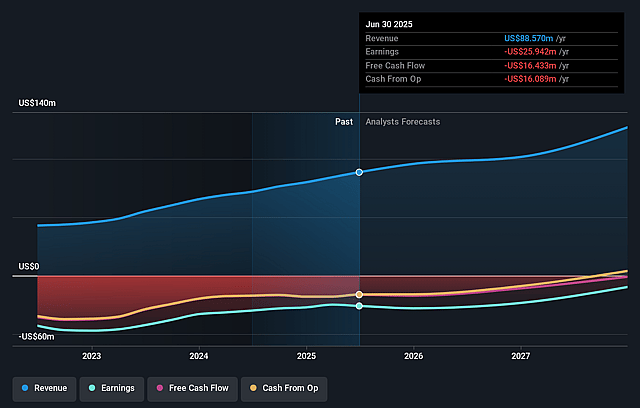

- The updated 2026 revenue guidance of US$99m to US$101m, tied to 21% to 23% growth in the core RNS business, is viewed as a sign of confidence in execution and capacity to scale the existing platform.

- Some view the raised price target as recognition that stronger prescriber and patient pipeline trends could justify a richer valuation if the company hits its stated revenue range.

- Bullish analysts also point out that guidance does not include any contribution from potential idiopathic generalized epilepsy indication expansion, which they see as additional optionality for future growth if it materializes.

Bearish Takeaways

- Bearish analysts focus on execution risk, noting that the 21% to 23% growth expectation for the core RNS business requires sustained performance from prescribers and accounts, with little room for operational missteps.

- There is caution that the price target move may already factor in strong pipeline metrics, which could limit upside if future data only matches, rather than exceeds, current guidance.

- Some are wary that the exclusion of idiopathic generalized epilepsy from current guidance means investors should be careful not to overvalue unproven revenue streams that are not yet part of the official outlook.

- Bearish analysts also flag that reliance on a concentrated core RNS franchise exposes the company to risk if competitive or regulatory pressures emerge and weigh on execution against the 2026 targets.

What's in the News

- FDA approved NeuroPace’s first AI driven clinician enabled feature, ECoG Assistant, built on long term patient level brain data from the RNS System to support faster and more confident treatment decisions. (Source: Company product announcement)

- ECoG Assistant is positioned as the first in a planned suite of NeuroPace AI tools. Features such as the ECoG Assistant Trends Report and Circadian Pattern Chart are aimed at helping clinicians review ECoGs of Interest over months and explore timing patterns and potential triggers. (Source: Company product announcement)

- NeuroPace has submitted its next generation Patient Data Management System to the FDA. It is designed to modernize software infrastructure for the RNS System and provide a more flexible base for AI enabled tools, with company expectations for potential approval in the second quarter of 2026. (Source: Company product announcement)

- New clinical data were released, including 3 year results from the RNS System Post Approval Study in Neurology and 12 and 18 month NAUTILUS trial data. These data reinforce clinical outcomes in drug resistant focal epilepsy and outline seizure reductions and lower injury and rescue medication events in idiopathic generalized epilepsy. (Source: Company clinical evidence program update)

- NeuroPace revised its 2026 earnings guidance, now expecting total revenue of US$99m to US$101m for the full year and a GAAP loss from operations of US$19,500,000 to US$20,500,000. (Source: Company guidance update)

Valuation Changes

- Fair Value: The assessed fair value per share has risen slightly from $19.88 to $20.00.

- Discount Rate: The discount rate has fallen slightly from 8.02% to 7.80%, implying a modest change in the required return used in the valuation model.

- Revenue Growth: The modeled long term revenue growth rate has moved from 15.39% to 16.95%.

- Net Profit Margin: The projected net profit margin has fallen significantly from 13.08% to 0.38%, indicating a much lower earnings contribution on each revenue dollar in the current assumptions.

- Future P/E: The future P/E multiple has shifted sharply from 44.9x to 1,540.6x, suggesting that earnings now account for a much smaller share of the valuation in the updated model.

Key Takeaways

- Expanding presence in epilepsy centers and Project CARE may significantly boost revenue by increasing market penetration and service delivery.

- AI-enhancements and clinical program advancements promise operational efficiency, new revenue streams, and improved financial performance.

- NeuroPace's growth strategy relies on ambitious expansions, new product success, and increased prescriber engagement, yet faces risks from resource strain and market adoption challenges.

Catalysts

About NeuroPace- Operates as a medical device company in the United States.

- Expanding adoption and utilization within Level 4 comprehensive epilepsy centers could significantly increase revenue by tapping into a $2 billion annual core market opportunity.

- Project CARE aims to expand site of service delivery and has begun contributing to revenue growth; doubling implants and referrals can further drive revenue increases.

- Advancing key clinical development programs to expand indications of use for the RNS System suggests potential new revenue streams and market expansion, positively impacting future earnings.

- Introduction of AI-enabled software tools and next-generation platform improvements might enhance operational efficiency and patient outcomes, potentially boosting both revenue and net margins.

- Strengthened balance sheet post-public offering supports strategic growth initiatives and operating expansions, aiming for cash flow breakeven and improved earnings.

NeuroPace Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming NeuroPace's revenue will grow by 17.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -21.7% today to 0.4% in 3 years time.

- Analysts expect earnings to reach $601.6 thousand (and earnings per share of $0.02) by about June 2029, up from -$21.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $9.6 million in earnings, and the most bearish expecting $-22.4 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 1554.0x on those 2029 earnings, up from -26.1x today. This future PE is greater than the current PE for the US Medical Equipment industry at 24.2x.

- Analysts expect the number of shares outstanding to grow by 3.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.8%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- NeuroPace's rapid expansion strategy at Level 4 comprehensive epilepsy centers and outside of them with Project CARE depends on significant increases in implants and referrals, which might strain their resources and potentially affect revenue if expected growth doesn't materialize as projected.

- The company's 2025 revenue guidance is heavily reliant on the success of new product offerings and indications, such as the NAUTILUS pivotal study and pediatric RNS indications. Regulatory or clinical trial setbacks could delay these expansions and impact forecasted revenue growth.

- While gross margins are currently healthy, potential fluctuations in the mix of distributed product lines, like DIXI Medical, which carry lower margins, could pressure overall gross margins, impacting profitability.

- The company's reliance on increasing prescriber numbers and direct-to-consumer marketing for revenue growth might incur higher-than-anticipated expenses, affecting their net income and ability to achieve cash flow breakeven.

- NeuroPace's significant investments in AI-enabled software tools and new technologies aim for long-term gains, but if deployment or adoption is slower than expected, it could impact short-to-medium-term earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $20.0 for NeuroPace based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $159.2 million, earnings will come to $601.6 thousand, and it would be trading on a PE ratio of 1554.0x, assuming you use a discount rate of 7.8%.

- Given the current share price of $16.51, the analyst price target of $20.0 is 17.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on NeuroPace?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.