Last Update 01 Jul 26

Fair value Decreased 4.07%WU: New Stablecoin And Intermex Deal Will Support Future Earnings

Analysts have slightly reduced their $ fair value estimate for Western Union to about $9.08 from roughly $9.46, citing updated assumptions for discount rates, revenue growth, profit margins, and future P/E multiples.

What’s in the News for Western Union

- Western Union and Total Wireless partnered to embed one fee-free Western Union money transfer per month into certain Total Wireless plans, with transfers available to over 200 countries and territories, according to recent company announcements.

- Western Union and International Money Express, Inc. reported that regulators in 51 U.S. states and territories and all international jurisdictions have either approved or not objected to Western Union’s pending acquisition of Intermex, with approval from one remaining U.S. state and customary closing conditions still outstanding.

- Western Union announced the launch of USDPT, a U.S. dollar denominated payment stablecoin issued by Anchorage Digital Bank N.A. on the Solana blockchain, which is positioned as an always on settlement asset within Western Union’s global payment systems.

- Western Union and crypto exchange Bybit disclosed that Bybit users in selected Latin American markets can now access USDPT through Bybit’s fiat channels, creating a new on and off ramp for the stablecoin using local currencies.

- Western Union disclosed that from January 1, 2026 to March 31, 2026, it repurchased 4,788,206 shares for $45.2 million, completing a total of 28,460,589 shares repurchased for $269.86 million under the buyback program announced on December 13, 2024.

Valuation Changes for Western Union

- Fair Value: The fair value estimate for Western Union was trimmed from $9.46 to $9.08, a small downward adjustment.

- Discount Rate: The discount rate assumption moved slightly higher from 9.03% to 9.06%, indicating a modest increase in the required return used in the model.

- Revenue Growth: The revenue growth assumption eased from 4.91% to 4.70%, reflecting a slightly more conservative outlook for future sales expansion in dollar terms.

- Net Profit Margin: The profit margin assumption edged down from 12.10% to 12.07%, a minimal change in expected profitability.

- Future P/E: The future P/E multiple was revised from 6.11x to 5.92x, indicating a slightly lower valuation multiple being applied to Western Union’s earnings in the model.

Key Takeaways

- Expansion in digital services, AI integration, and new consumer offerings enhance cost efficiency, diversify revenue, and position the company for higher margins and long-term growth.

- Increased migration and urbanization drive resilient remittance demand, while early adoption of blockchain and stablecoin technologies offers new revenue and operational advantages.

- Declining transaction volumes, rising regulatory and compliance burdens, and intensified competition from digital and fintech disruptors threaten revenue, market share, and long-term profitability.

Catalysts

About Western Union- Provides money movement and payment services worldwide.

- The ongoing digital transformation-including expanded digital wallet offerings, card-based retail transactions, and value-added services-positions the company to capture a growing share of the large, underpenetrated market of financially included and mobile-first consumers, supporting improved revenue growth and higher long-term net margins due to better cost efficiency.

- Rising global migration flows and continued urbanization underpin resilient long-term demand for cross-border remittances, strengthening Western Union's top-line prospects despite near-term headwinds in specific corridors or geographies.

- The integration of AI-driven operational improvements across customer service, technology, and treasury operations is already driving significant cost savings and productivity gains, providing a clear path to further operating margin expansion and improved long-term earnings power.

- Early strategic engagement with stablecoins and on-chain settlement technologies offers the potential to materially lower capital requirements, accelerate settlement speed, and potentially increase revenue opportunities by serving as a global on/off-ramp between fiat and digital currencies as global payments infrastructure modernizes.

- Growth in the Consumer Services segment-including acquisitions like Eurochange and expanded travel money and bill-pay offerings-unlocks new, higher-margin revenue streams and diversifies earnings, contributing to greater earnings stability and supporting higher valuations as these businesses scale.

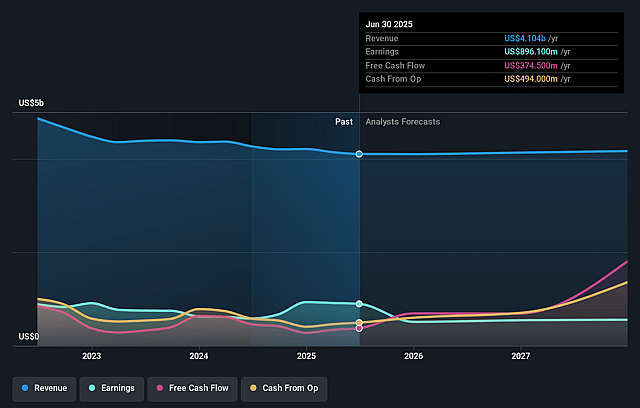

Western Union Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Western Union's revenue will grow by 4.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.9% today to 12.1% in 3 years time.

- Analysts expect earnings to reach $561.1 million (and earnings per share of $1.92) by about July 2029, up from $440.8 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $693.0 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 5.9x on those 2029 earnings, up from 5.6x today. This future PE is lower than the current PE for the US Diversified Financial industry at 15.3x.

- Analysts expect the number of shares outstanding to decline by 3.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.06%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying regulatory scrutiny and enforcement around immigration in the U.S. is creating persistent volatility and softness in key corridors, especially U.S. to Mexico, leading to lower transaction volumes and risking further revenue declines if policies tighten further or customer behavior shifts to informal or alternative remittance channels. (Impacts: revenue and earnings)

- Growth in Western Union's digital business is not offsetting weakness in the core retail channel in North America; both digital and retail money transfer transactions showed declines in critical regions, suggesting the company may be losing market share to digital-first disruptors and that topline growth is at risk. (Impacts: revenue and top-line growth)

- Aggressive expansion of lower-cost digital and fintech competitors, as well as emerging blockchain and stablecoin-based solutions, is eroding pricing power and could pressure profit margins long-term if Western Union cannot accelerate its shift to digital and innovate fast enough. (Impacts: net margins and long-term competitiveness)

- Increasing global financial inclusion and rising adoption of digital wallets may reduce dependence on cash-based remittances-Western Union's historical core-limiting customer growth potential and challenging legacy agent-network-driven cost structure. (Impacts: revenue, customer base, and cost flexibility)

- New taxes on cash remittance transactions (such as the 1% U.S. remittance tax) and ongoing regulatory changes raise compliance costs and could further drive customers towards non-traditional or lower-cost channels, making it more difficult for Western Union to protect net margins if they do not successfully transform their business mix. (Impacts: net margins and cost structure)

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $9.08 for Western Union based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $11.0, and the most bearish reporting a price target of just $7.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.6 billion, earnings will come to $561.1 million, and it would be trading on a PE ratio of 5.9x, assuming you use a discount rate of 9.1%.

- Given the current share price of $7.85, the analyst price target of $9.08 is 13.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Western Union?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.