Key Takeaways

- Fast digital and distribution transformation, plus early stablecoin adoption, position Western Union for revenue and margin gains ahead of market expectations.

- AI-driven automation and growth in emerging markets enable cost reductions and accelerated long-term earnings growth.

- Digital disruption, heightened competition, regulatory challenges, and high fixed costs threaten Western Union's profitability as consumer preference shifts away from cash-based transfers.

Catalysts

About Western Union- Provides money movement and payment services worldwide.

- Analysts broadly agree that the Evolve 2025 strategy will gradually drive profitable revenue growth and margin expansion, but early results in Europe and rapid scaling of owned distribution (such as exclusive UK Post and Eurochange) indicate the strategy may deliver step-function gains in both revenue and margin years ahead of consensus estimates.

- While consensus expects the digital transformation to support steady gains, Western Union's real-time migration of US retail volumes to card-based transactions, accelerated by tax changes, is likely to convert a much larger portion of the base to higher-margin digital and wallet products with speed, significantly boosting both revenue growth and net margins.

- Western Union's early embracing of stablecoin rails and on-/off-ramp services could allow it to leapfrog legacy players in emerging markets, reduce capital requirements for cross-border settlements, and capture a leadership share in new digital remittance corridors, translating into higher revenue and unprecedented improvements in operating cash flow.

- Robust adoption of AI-driven automation-from customer service through treasury and compliance-will drive structural cost advantage, enabling sustained reductions in operating expenses and materially higher earnings growth potential than is being modeled by the market.

- Secular tailwinds-especially expanding migration and rapid financial services digitization in Asia and Africa-position Western Union to capture market share in fast-growing remittance corridors, supporting double-digit transaction growth and outsized long-term revenue acceleration.

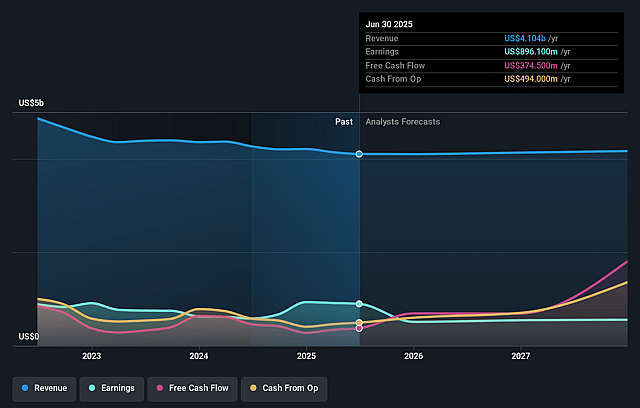

Western Union Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Western Union compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Western Union's revenue will grow by 2.2% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 21.8% today to 12.4% in 3 years time.

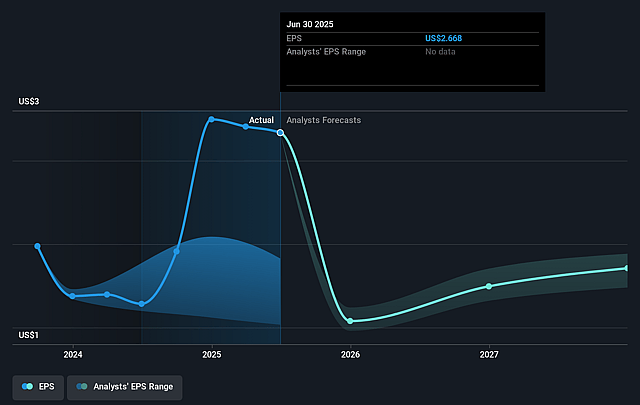

- The bullish analysts expect earnings to reach $543.9 million (and earnings per share of $1.82) by about September 2028, down from $896.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 9.8x on those 2028 earnings, up from 3.1x today. This future PE is lower than the current PE for the US Diversified Financial industry at 16.5x.

- Analysts expect the number of shares outstanding to decline by 4.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.6%, as per the Simply Wall St company report.

Western Union Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Accelerating adoption of digital wallets, mobile payment platforms, and fintech-led financial inclusion initiatives is reducing demand for cash-based money transfer services, which could structurally erode Western Union's retail transaction volumes and place downward pressure on long-term revenues.

- Western Union continues to experience market share losses to digital-native competitors and faces slowing transaction growth in both its retail and digital channels, indicating that its relatively slow digital transition could further impact future revenue growth and profitability.

- Persistent regulatory scrutiny, changing immigration policies, the introduction of a 1% remittance tax on cash-based transfers, and increasing AML compliance obligations add uncertainty and could increase Western Union's compliance and operational costs, negatively affecting net margins and earnings.

- Intensifying industry competition, both from traditional players and emerging blockchain or stablecoin-enabled transfer rails, continues to compress remittance fees, threatening Western Union's fee-based business model and placing sustained downward pressure on both top line revenue and net margins.

- Western Union's heavy reliance on its extensive physical agent network leads to high fixed costs, which may become increasingly burdensome as consumer preference shifts online, further squeezing net margins and lowering overall profitability in the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Western Union is $14.42, which represents two standard deviations above the consensus price target of $9.32. This valuation is based on what can be assumed as the expectations of Western Union's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $17.0, and the most bearish reporting a price target of just $7.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $4.4 billion, earnings will come to $543.9 million, and it would be trading on a PE ratio of 9.8x, assuming you use a discount rate of 9.6%.

- Given the current share price of $8.64, the bullish analyst price target of $14.42 is 40.1% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.