Last Update 24 Jul 26

Fair value Decreased 13%CKF: Class Action Settlement Progress Will Support Future P/E Re-Rating

Analysts have trimmed their price target on Collins Foods from A$11.79 to A$10.27, citing updated assumptions around slightly lower profit margins, a modestly lower discount rate and a small adjustment to the future P/E multiple, along with revised revenue growth expectations.

What’s in the News for Collins Foods

- No recent Collins Foods news items were available from the provided primary sources.

- No relevant Collins Foods coverage was identified in the periodicals data supplied.

- No additional Collins Foods key developments were listed in the referenced materials.

Valuation Changes for Collins Foods

- Fair Value: trimmed from A$11.79 to A$10.27, a reduction of roughly 13%.

- Discount Rate: adjusted slightly lower from 10.19% to 9.99%.

- Revenue Growth: revised modestly higher from 6.48% to 7.23%.

- Net Profit Margin: reduced from 4.88% to about 4.10%, reflecting a lighter margin outlook.

- Future P/E: eased marginally from 20.17x to 20.05x.

Key Takeaways

- Growth in digital revenue channels and KFC store remodels could boost customer engagement, sales, and margins.

- Strategic technology, sustainability investments, and a strong balance sheet may enhance efficiencies, support M&A, and drive long-term earnings growth.

- Cost-of-living pressures and inflation are impacting Collins Foods' revenue growth and margins, with potential short-term cash flow strain from new investments.

Catalysts

About Collins Foods- Engages in the operation, management, and administration of restaurants in Australia and Europe.

- The continued growth in digital revenue channels, accounting for over 33% of sales in Australia and more than 60% in Europe, provides an opportunity to drive higher basket sizes and improved customer engagement, which could positively impact revenue and net margins.

- The expansion and remodeling of KFC stores, including the super-charge remodels, are expected to deliver rapid same-store sales growth and enhance customer experience, potentially boosting revenue and EBITDA margins.

- The company's focus on operational excellence and innovation with Every Day Value marketing strategies may help drive same-store sales growth and protect margins against inflationary pressures, especially in Australia.

- Strategic investments in technology and sustainability, alongside a disciplined approach to new restaurant development, are expected to enhance operational efficiencies and drive earnings growth in the medium to long term.

- A strong balance sheet and maintained cash generation capacity position Collins Foods to seize potential M&A opportunities, potentially expanding the store network and enhancing revenue and EBIT growth prospects.

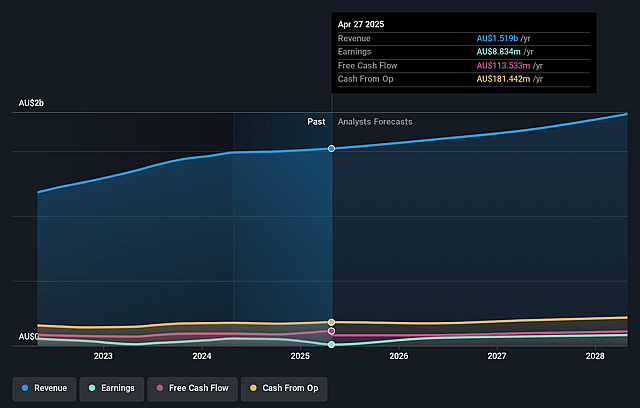

Collins Foods Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Collins Foods's revenue will grow by 7.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.0% today to 4.1% in 3 years time.

- Analysts expect earnings to reach A$80.4 million (and earnings per share of A$0.7) by about July 2029, up from A$47.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting A$93.7 million in earnings, and the most bearish expecting A$54.8 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 20.1x on those 2029 earnings, up from 19.3x today. This future PE is lower than the current PE for the AU Hospitality industry at 22.1x.

- Analysts expect the number of shares outstanding to grow by 0.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.99%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company faced a decline in same-store sales in KFC Europe, attributed to affordability issues due to cost of living pressures, indicating challenges that could continue to impact revenue growth in these markets.

- Persistent inflation has led to lower margins, particularly impacting labor and energy costs, which suggests possible continued pressure on net margins.

- The outlook suggests that margins will remain under pressure until at least FY '26, indicating potential challenges in maintaining or improving earnings in the short term.

- Challenges in the Netherlands, including disruptions due to local demonstrations, could affect customer traffic and sales levels, thereby impacting revenue consistency.

- Investment in new restaurants and remodelling, although positive for long-term growth, involves significant CapEx, which might strain short-term cash flows and earnings if not managed properly.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$10.27 for Collins Foods based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$12.5, and the most bearish reporting a price target of just A$8.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be A$2.0 billion, earnings will come to A$80.4 million, and it would be trading on a PE ratio of 20.1x, assuming you use a discount rate of 10.0%.

- Given the current share price of A$7.7, the analyst price target of A$10.27 is 25.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Collins Foods?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.