Last Update 30 Jun 26

Fair value Increased 11%TRST: Shopify Partnership And German Expansion Will Support Stronger Future Returns

The latest analyst updates have lifted the implied fair value for Trustpilot Group to about £3.40 per share from roughly £3.07, with the shift mainly linked to firmer margin assumptions, a lower future P/E of around 42x, and recent supportive research including a new Overweight rating and raised price targets.

Analyst Commentary

Recent street research around Trustpilot Group gives a mixed picture, with some analysts pointing to underappreciated product strength and geographic opportunities, while others are more cautious. For you as an investor, the key questions are how much growth can be captured in core markets and whether the current share price already reflects those expectations.

Bullish Takeaways

- Bullish analysts highlight Trustpilot Group's products as a core asset that they see as undervalued at current share levels. They link this view to upside potential in the implied fair value range.

- Growth in focus markets such as Germany is a central part of the constructive view. Supporters argue that successful execution there could help support the higher P/E and margin assumptions used in recent fair value work.

- The initiation of coverage with an Overweight rating and a £3.50 price target is cited by bullish analysts as evidence that some on the street view the risk or reward balance as attractive relative to current pricing.

- Supportive research and raised price targets are seen as reinforcing confidence in Trustpilot Group's ability to convert its product and geographic position into financial progress that can justify the current valuation framework.

Bearish Takeaways

- Bearish analysts, including those behind the recent downgrade, are more cautious on execution risk. They question whether Trustpilot Group can fully deliver on the growth embedded in higher margin and P/E assumptions.

- The downgrade signals concern that the share price may already embed optimistic expectations, leaving less room for disappointment if product traction or geographic expansion does not unfold as anticipated.

- Some cautious views focus on the possibility that investor enthusiasm around specific markets like Germany could exceed the near term contribution to earnings or cash flow. This would weigh on how sustainable the current valuation looks.

- The presence of both raised targets and a downgrade in close succession underlines that there is no clear consensus on Trustpilot Group. This means the stock can be sensitive to any new information on growth, margins, or capital allocation.

What’s in the News for Trustpilot Group

- Trustpilot is partnering with Shopify to let merchants display and manage Trustpilot reviews directly on their Shopify stores. CEO Adrian Blair highlights reviews as a way to build trust for customers amid rising AI generated content (source: Bloomberg, Chloe Meley).

- Trustpilot Group has appointed Ernst & Young LLP as auditors at its Annual General Meeting held on 19 May 2026, marking a change in audit firm for the company.

- Trustpilot Group has scheduled an Analyst and Investor Day to provide a deep dive into its trust infrastructure and to facilitate interactions between investors and the wider Trustpilot team.

Valuation Changes for Trustpilot Group

- Fair Value increased from £3.07 to £3.40 per share, reflecting a modest uplift in the implied valuation range for Trustpilot Group.

- Discount Rate moved from 8.65% to 9.09%, indicating a slightly higher required return being used in the updated analysis.

- Revenue Growth adjusted from 17.84% to 16.78%, pointing to a more conservative view on future $ revenue expansion in the model.

- Profit Margin updated from 9.64% to 11.63%, implying higher expected $ profitability relative to prior assumptions.

- Future P/E reduced from 59.35x to 42.16x, suggesting a lower valuation multiple is now being applied to Trustpilot Group’s projected earnings.

Key Takeaways

- Trustpilot's product innovation and pricing strategies enhance retention and future revenue growth, alongside strong market expansion, particularly in the U.S.

- Increased profitability is driven by operating leverage and a strategic shift towards enterprise clients with higher value contracts.

- Foreign exchange volatility, growth deceleration, competition, macro-economic uncertainties, and innovation challenges could collectively strain Trustpilot's revenue stability and operational efficiency.

Catalysts

About Trustpilot Group- Engages in the development and hosting of an online review platform for businesses and consumers in the United Kingdom, North America, Europe, and internationally.

- Trustpilot's SaaS business model is supported by product innovation, resulting in new product launches within pricing plans that have improved net dollar retention from 99% to 103%, which is expected to drive future revenue growth.

- Bookings have grown by 21% in constant currency, particularly with strong growth in key markets like the U.S., which saw a 26% increase. This growth is expected to sustain revenue increases in the future.

- Consumer adoption of Trustpilot is strong, with active reviews up by 23% and TrustBox impressions up by 19%, enhancing brand awareness and potential earnings through increased engagement.

- Operating leverage has led to a 260 basis point increase in adjusted EBITDA margin to 11.4%, which signals an expectation of improved profitability going forward.

- Strategic focus on enterprise clients and higher service packages is shifting the customer mix towards higher contract values, likely improving the company’s net margins and overall revenue.

Trustpilot Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

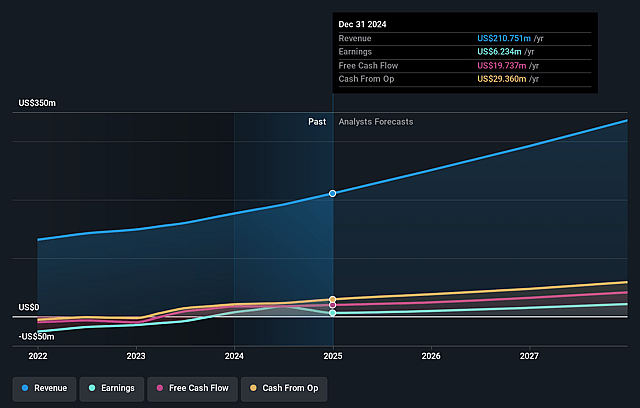

- Analysts are assuming Trustpilot Group's revenue will grow by 16.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.0% today to 11.6% in 3 years time.

- Analysts expect earnings to reach $48.4 million (and earnings per share of $0.12) by about June 2029, up from $7.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $69.4 million in earnings, and the most bearish expecting $32.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 42.2x on those 2029 earnings, down from 170.9x today. This future PE is greater than the current PE for the GB Interactive Media and Services industry at 19.3x.

- Analysts expect the number of shares outstanding to decline by 4.02% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.09%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The impact of foreign exchange volatility, particularly with the euro and sterling against the dollar, could adversely influence reported revenue despite strong bookings growth, affecting earnings.

- The anticipated deceleration of growth, following the one-time benefit from migrating customers to new pricing plans, could challenge sustained revenue growth if not compensated by upsells within the new pricing bands, impacting future revenue stability.

- Increasing competition and evolving market dynamics could strain Trustpilot's ability to maintain high retention rates and expand market share, potentially impacting net margins if customer acquisition costs rise relative to revenue.

- Macro-economic uncertainties, like inflation or downturns, particularly in the U.S., could affect SME clients more significantly, leading to higher churn rates and impacting overall revenue and financial projections.

- The need to continuously innovate while minimizing distractions from new ventures such as TrustLayer could strain resources, which may affect operational efficiency and net earnings if not managed effectively.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £3.4 for Trustpilot Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £4.12, and the most bearish reporting a price target of just £2.39.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $415.8 million, earnings will come to $48.4 million, and it would be trading on a PE ratio of 42.2x, assuming you use a discount rate of 9.1%.

- Given the current share price of £2.54, the analyst price target of £3.4 is 25.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Trustpilot Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.