Last Update 05 Jun 26

PRN: New Leadership Appointment Will Support Re Rating Potential

Analysts have kept their A$2.70 price target for Perenti broadly unchanged, reflecting only minor tweaks to the discount rate and valuation inputs rather than a shift in their overall view of the stock.

What's in the News

- Perenti has announced that Dr. Vanessa Torres will succeed Mark Norwell as CEO, following the transition process outlined to shareholders at the October AGM. Source: Company key developments

- Dr. Torres brings more than 25 years of senior leadership experience across the global resources industry, including roles as Chief Operating Officer, Chief Technology Officer and Chief Technical Officer at South32, as well as executive positions at BHP and Vale in South and North America. Source: Company key developments

- Her appointment follows an extensive search process led by Perenti's non executive directors with a global executive search firm, with a focus on supporting a fully diversified portfolio of businesses and long term growth ambitions. Source: Company key developments

- Dr. Torres is scheduled to commence with Perenti on April 13, 2026 and to be appointed CEO on June 1, 2026, while outgoing CEO Mark Norwell will remain with the company to support the transition through June and into FY27. Source: Company key developments

Valuation Changes

- Fair Value: A$2.70 remains unchanged, with the updated estimate still at A$2.70.

- Discount Rate: risen slightly from 9.07% to about 9.10%, reflecting a modest adjustment to the risk settings used in the model.

- Revenue Growth: effectively steady at about 3.98%, with only a very small numerical adjustment in the modelled rate.

- Net Profit Margin: effectively steady at about 5.95%, with only a minor rounding change in the updated assumption.

- Future P/E: risen slightly from about 14.61x to about 14.63x, indicating a marginally higher multiple applied in the forward valuation.

Key Takeaways

- Expansion into new regions, digital innovation, and strong ESG positioning are broadening market opportunities, improving efficiency, and enhancing Perenti's revenue growth and margins.

- Improved cash flow and reduced debt are enabling increased investment, higher shareholder returns, and strengthening overall financial resilience.

- Margin pressure, geographic risk, talent shortages, and rising ESG compliance threaten Perenti's revenue stability, earnings growth, and ability to diversify or sustainably expand profits.

Catalysts

About Perenti- Operates as a mining services company worldwide.

- The accelerating demand for critical minerals (such as copper, lithium, and nickel) driven by global energy transition and electrification is fueling a large and sustained pipeline of projects, which underpins Perenti's long-term contract opportunities and provides high revenue visibility and growth potential.

- Expanded presence and contract wins in North America and ongoing diversification beyond Africa and Australia are reducing geographic concentration risk, broadening Perenti's addressable market, and positioning it to capture a larger share of global mining investment, supporting future revenue growth and margin stability.

- Adoption and commercialization of digital mining solutions and automation (via investments in idoba and fleet optimization) are expected to improve operational efficiency and safety, supporting gradual EBITDA margin expansion and higher long-term earnings.

- The steady trend among mining companies to outsource complex operations to contractors with strong ESG credentials and technical expertise plays to Perenti's strengths, as tightening environmental and social standards favor established, diversified operators-supporting both contract pipeline growth and premium pricing, enhancing margins.

- Record cash generation and ongoing deleveraging have strengthened the balance sheet, enabling Perenti to allocate additional capital toward growth projects, pay higher dividends and conduct buybacks, all of which are likely to support EPS and shareholder returns in the medium to long term.

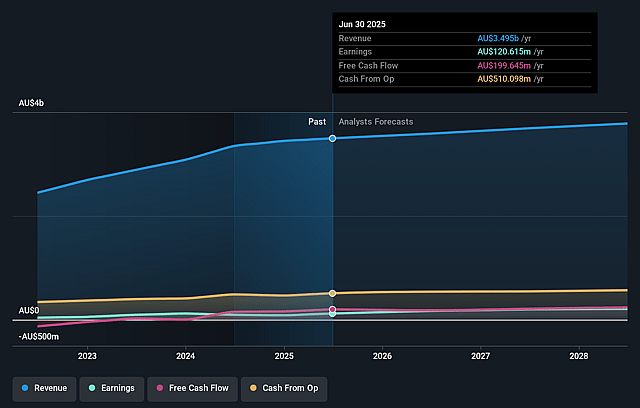

Perenti Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Perenti's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.5% today to 6.0% in 3 years time.

- Analysts expect earnings to reach A$233.9 million (and earnings per share of A$0.23) by about June 2029, up from A$122.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting A$262.7 million in earnings, and the most bearish expecting A$208.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 14.6x on those 2029 earnings, down from 16.2x today. This future PE is greater than the current PE for the AU Metals and Mining industry at 12.4x.

- Analysts expect the number of shares outstanding to grow by 1.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.1%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent margin pressure and client bargaining power, especially in contract mining, could limit Perenti's ability to sustainably expand net margins, as evidenced by past financial underperformance in Botswana and recent project conclusions, potentially capping long-term earnings growth.

- Geographic concentration in Africa and Australia, with relatively new and small exposure in North America, increases exposure to political instability, regulatory changes, and operational disruptions, which could adversely impact revenue stability and future cash flow.

- Slower recovery in exploration drilling and ongoing underutilization in areas such as Mining and Technology Services indicate that macro industry headwinds or technological disruption could limit top-line growth and reduce Perenti's ability to diversify earnings streams.

- Structural workforce challenges in the mining sector, including skill shortages and labor inflation, could elevate operational costs and slow project delivery, placing further pressure on operating margins and overall profitability.

- Increasingly stringent ESG requirements and evolving regulatory frameworks may elevate compliance costs and restrict permit access, particularly in higher-risk jurisdictions, potentially delaying projects and eroding future revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$2.7 for Perenti based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$2.87, and the most bearish reporting a price target of just A$2.35.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be A$3.9 billion, earnings will come to A$233.9 million, and it would be trading on a PE ratio of 14.6x, assuming you use a discount rate of 9.1%.

- Given the current share price of A$2.12, the analyst price target of A$2.7 is 21.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Perenti?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.