Last Update 01 Jul 26

Fair value Increased 217%MXL: AI Optical Hype Will Pressure Future Repricing Assumptions

MaxLinear's updated analyst price target of $68.36, compared with the previous fair value estimate of $21.55, reflects analysts' focus on its expanding data center and AI optical infrastructure ambitions, as well as the potential for a higher margin infrastructure mix.

Analyst Commentary

Recent research on MaxLinear centers on how the stock reflects its growing exposure to AI driven data center and optical infrastructure, as well as the company’s longer term infrastructure ambitions. Price targets in the research cited are clustered well above the current fair value estimate, which highlights how much weight some analysts are placing on execution in this part of the business.

Bullish Takeaways

- Bullish analysts point to MaxLinear’s focus on data center and AI optical interconnects as a key driver for their higher price targets, linking these areas to a potentially higher margin infrastructure mix.

- The reiterated long term ambition for a US$3b infrastructure business is used by optimistic analysts as a reference point for the company’s scale aspirations. They incorporate this into more constructive valuation frameworks.

- Several price target increases are tied to what bullish analysts describe as improving traction across MaxLinear’s product lines that are connected to AI data center demand. They view this as supportive for growth expectations.

- Some research argues that MaxLinear is no longer viewed mainly as a broadband recovery story, but as a small cap mixed signal supplier with AI interconnect exposure. Bullish analysts see this as supporting a higher valuation multiple.

Bearish Takeaways

- More cautious analysts highlight that current sentiment and valuation are sensitive to AI related expectations, so any shortfall in AI optical demand or project timing could affect how the stock is priced.

- The US$3b infrastructure goal is long term and contingent on MaxLinear’s execution in new and existing product categories. This introduces uncertainty around how quickly, or even whether, that ambition is met.

- While some research cites building AI optical visibility, skeptics may question the durability of this visibility if cloud capex plans or broader AI spending priorities change, which could affect revenue mix assumptions.

- The re rating described by bullish analysts implies that a meaningful portion of the AI and infrastructure story is already reflected in the stock. This leaves less room for error if growth or margins do not track expectations.

What’s in the News for MaxLinear

- MaxLinear reported Q1 fiscal 2026 revenue growth of 43% year over year, with a 136% rise in its infrastructure segment and AI optical data center business becoming the largest revenue category, non GAAP diluted EPS of $0.22, and a 59.5% gross margin, while management issued 2026 optical data center revenue guidance of US$150 million to US$170 million and Q2 2026 revenue guidance of US$160 million to US$170 million (source: recent earnings coverage).

- The stock surged nearly 200% in April 2026 to a four year high, supported by bullish analyst upgrades and higher price targets. These included Loop Capital’s move to a US$75 target and Stifel’s target increase to US$105, although some third party services describe the shares as trading well above certain intrinsic value estimates and highlight an elevated forward P/E versus historical levels (sources: MaxLinear Soars on 43% Q1 Revenue Growth, MaxLinear Shares Show Volatility Amid Sector Rally and Overvaluation Concerns).

- MaxLinear’s infrastructure segment, led by data center optical platforms such as the Keystone PAM4 DSP family, became the company’s largest revenue category in Q1 2026. Management commentary focused on AI optical ramps at major data centers in the US and Asia and expectations for continued infrastructure led revenue contributions (source: Infrastructure Takes Center Stage for MaxLinear: What Lies Ahead?).

- Recent partnerships include a collaboration with Los Alamos National Laboratory to integrate Panther storage accelerator SoCs into hardware accelerated OpenZFS for high performance computing and AI workloads, and alliances with GCT Semiconductor and Edgecore Networks to support 5G fixed wireless access gateways and AI focused edge networking solutions (sources: LANL collaboration announcement, GCT partnership announcement, Edgecore partnership announcement).

- Index providers removed MaxLinear from several Russell value oriented benchmarks, including the Russell 3000 Value, Russell 2500 Value, Russell 2000 Value, and related composites. The company also changed its auditor, replacing Grant Thornton LLP with KPMG LLP for the fiscal year ending December 31, 2026 (source: index constituent changes and auditor change filings).

Valuation Changes for MaxLinear

- Fair Value: updated from $21.55 to $68.36, a very large upward reset in the valuation anchor used for MaxLinear.

- Discount Rate: moved slightly higher from 10.91% to 11.15%, implying a modestly higher required return for valuing future cash flows.

- Revenue Growth: revised from 13.33% to 24.03%, indicating a meaningfully higher assumed top line growth profile for the company.

- Net Profit Margin: adjusted down from 16.30% to 10.48%, reflecting a more conservative view on MaxLinear’s long term profitability.

- Future P/E: updated from 22.79x to 89.45x, a very large step up in the multiple implied by the new assumptions.

Key Takeaways

- Expanding partnerships with major telecom and cloud customers, plus strong design wins in data center and wireless, position MaxLinear for sustained, broad-based growth.

- Ongoing innovation and cost efficiency in advanced connectivity and AI-focused solutions bolster the company's pricing power, profit margins, and market reach.

- Heavy reliance on maturing broadband markets, industry commoditization, geopolitical risks, acquisition distractions, and rapid technological change threaten growth, margins, and long-term competitiveness.

Catalysts

About MaxLinear- Provides communications systems-on-chip solutions in the United States, Asia, Europe, and internationally.

- Accelerating demand for high-speed data center optical interconnects and next-generation PAM4 DSP solutions (Keystone and Rushmore), supported by robust design win momentum with major module makers and hyperscale customers, positions MaxLinear to capture a significant share of growing global data/AI infrastructure spend, likely driving meaningful revenue growth from late 2025 through 2027.

- Recovery and expansion in wireless infrastructure, including design wins with Tier 1 North American telecom operators for Sierra-based 5G base station products and increasing carrier CapEx, are expected to fuel sustained growth across 5G/future wireless networks, supporting top-line expansion and improved earnings visibility.

- Strong order rates, backlog, and rising service provider CapEx in broadband access-including significant gateway SoC wins for fiber PON and WiFi 7 platforms-reflect rising investment in broadband upgrades, indicating a multi-year opportunity for revenue growth and improved margin contribution as new platforms ramp.

- Continued investment in low-power high-performance analog and mixed-signal innovation, cost reduction initiatives, and the expansion of differentiated product offerings (e.g., Panther storage accelerators for data center/cloud AI use-cases) are set to enhance MaxLinear's technology edge, enabling premium pricing, margin improvement, and the potential for higher recurring earnings.

- Growing integration into Tier 1 customer roadmaps, both in North America and emerging markets like China (where data center transceiver volumes are forecast to rapidly expand), alongside demonstrated capability in cross-market platforms (optical, Ethernet, storage, wireless), increases MaxLinear's total addressable market and positions the company to benefit from long-term volume growth, supporting sustained revenue and earnings upside.

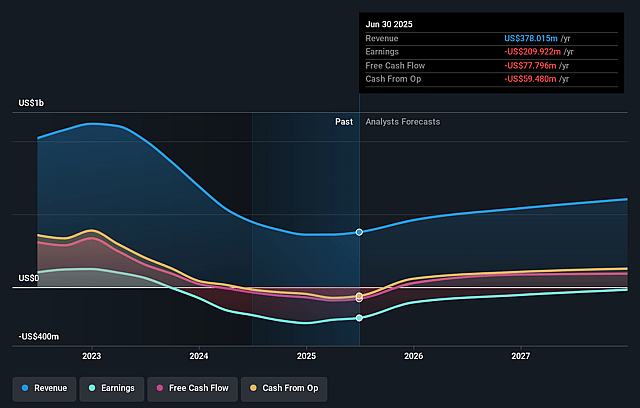

MaxLinear Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming MaxLinear's revenue will grow by 24.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -26.0% today to 10.5% in 3 years time.

- Analysts expect earnings to reach $101.8 million (and earnings per share of $0.59) by about July 2029, up from -$132.1 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $115.0 million in earnings, and the most bearish expecting $64.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 89.8x on those 2029 earnings, up from -86.8x today. This future PE is greater than the current PE for the US Semiconductor industry at 73.0x.

- Analysts expect the number of shares outstanding to grow by 2.83% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.15%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- MaxLinear remains heavily exposed to broadband and connectivity markets, which are maturing and subject to cyclical downturns; this concentration heightens the risk of long-term revenue stagnation if infrastructure CapEx cycles reverse or carrier investment slows. (Revenue)

- The semiconductor industry's ongoing commoditization and intense pricing pressure, particularly from larger competitors and low-cost Asian manufacturers (including China), threaten MaxLinear's ability to maintain premium pricing and healthy gross margins over the long run. (Gross margins, Earnings)

- Geopolitical tensions, rising protectionism (e.g., China's "Made in China" initiatives), and increasing regionalization of supply chains may reduce MaxLinear's access to major non-US markets or force margin-sapping concessions to retain share, exacerbating volatility in its international revenue streams. (Revenue, Net margins)

- MaxLinear's ongoing acquisitive growth strategy (including amortization of acquisition-related intangibles and recurring integration costs) raises the risk of impaired goodwill, unexpected restructuring expenses, and operational distractions, which could undermine net margins and consistent earnings expansion. (Net margins, Earnings)

- The rapid pace of technological evolution (such as the potential shift to custom ASICs, silicon photonics, or co-packaged optics) may outpace MaxLinear's R&D resources, threatening its market relevance and requiring expensive investments that, if unsuccessful, could lead to product obsolescence or missed growth opportunities. (R&D expenses, Revenue growth)

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $68.36 for MaxLinear based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $40.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $971.0 million, earnings will come to $101.8 million, and it would be trading on a PE ratio of 89.8x, assuming you use a discount rate of 11.1%.

- Given the current share price of $128.03, the analyst price target of $68.36 is 87.3% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on MaxLinear?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.