Last Update 14 May 26

Fair value Increased 168%MXL: Infrastructure Demand Inflection Will Eventually Fail To Justify Current P/E

Analysts have sharply lifted their MaxLinear price targets, with the updated fair value estimate moving from about $27.50 to roughly $73.73. Recent initiations, upgrades and target hikes reflect higher assumed revenue growth, a lower profit margin outlook and a much higher future P/E multiple.

Analyst Commentary

Recent Street research around MaxLinear has been firmly bullish, with multiple firms either initiating positive coverage, upgrading ratings or lifting price targets. Bullish analysts are generally leaning into a story that blends higher assumed revenue, changing margin assumptions and a willingness to assign a higher future P/E multiple.

Several research notes describe shares as having "room left to run" or highlight an "inflection" in infrastructure related demand. Others frame their target hikes as a response to what they see as improved execution and a clearer path to monetizing MaxLinear's portfolio.

Bullish analysts are not aligned on every detail, but the cluster of initiations, upgrades and target resets around similar dates points to a shared view that the previous fair value range no longer reflected their revised scenarios.

Bullish Takeaways

- Bullish analysts raising price targets by double digit dollar amounts signal a view that prior models understated the stock's potential valuation under updated assumptions for growth, profitability mix and P/E.

- Multiple upgrades around the same time suggest improving confidence in MaxLinear's ability to execute on its roadmap, particularly in areas tied to infrastructure where some research flags an "inflection."

- The combination of fresh initiations with a bullish tilt and follow up target increases indicates that more of the Street is willing to underwrite higher long term earnings power than before.

- References to "room left to run" in recent reports reflect a view that, even after earlier target levels, the risk or reward profile remains attractive enough to justify higher fair value estimates.

What's in the News

- MaxLinear announced Washington, a four lane 200G TIA for 1.6T optical transceivers aimed at AI data centers, with samples available now and mass production scheduled for the second half of 2026 (Key Developments).

- The company issued earnings guidance for the second quarter of 2026, targeting net revenue of about US$160 million to US$170 million (Key Developments).

- MaxLinear expanded its industrial connectivity portfolio with the MxL8323x RS-485 / RS-422 transceiver family, targeting harsh industrial environments and data rates up to 50 Mbps (Key Developments).

- The company introduced Annapurna, a scale up retimer designed to support up to 3.2 Tbps of copper connectivity at 224 Gbps per lane for AI focused data center architectures, with availability expected in the second quarter of 2026 (Key Developments).

- MaxLinear is rolling out and showcasing its Sierra based Open RAN radio solutions and power management platforms at MWC Barcelona 2026 and APEC 2026, highlighting use cases across macro O-RUs, indoor O-RUs and broadband gateways (Key Developments).

Valuation Changes

- Fair Value: The updated fair value estimate has risen significantly from $27.50 to about $73.73.

- Discount Rate: The discount rate assumption has edged higher from 10.40% to about 11.01%.

- Revenue Growth: The revenue growth assumption has moved up from roughly 21.88% to about 23.32%.

- Net Profit Margin: The net profit margin assumption has been reduced from about 14.10% to roughly 10.98%.

- Future P/E: The future P/E multiple assumption has increased sharply from about 36.4x to about 95.2x.

Key Takeaways

- Early leadership and rapid scaling in next-generation data center and broadband segments position MaxLinear to outpace competitors and consolidate market share in high-growth areas.

- Strong technology portfolio and fabless model enhance pricing power, supporting structurally higher margins and more resilient free cash flow through industry cycles.

- Heavy reliance on major customers, industry shifts, geopolitical risks, and slow diversification threaten MaxLinear's growth, margin stability, and long-term competitiveness.

Catalysts

About MaxLinear- Provides communications systems-on-chip solutions in the United States, Asia, Europe, and internationally.

- Analyst consensus expects Keystone and Rushmore deployments to drive strong growth, but they may be underestimating MaxLinear's penetration-the company is positioned to exceed $100 million in annual optical DSP revenues as 800-gigabit and 1.6-terabit transitions accelerate globally, especially as design wins quickly convert to multi-year production ramps, potentially doubling revenues in data center segments and meaningfully growing earnings per share through 2027.

- While the consensus sees broadband and PON wins driving growth, the pace of North American and global fiber investment, alongside MaxLinear's early leadership in 10-gigabit WiFi gateway SoCs and multi-gigabit PON, positions the company to consolidate market share in next-generation broadband, which could lift gross margins and deliver high-teens earnings growth, outpacing current Street models.

- MaxLinear's rapid scale in the Ethernet switch and PHY upgrade cycle-enabled by edge cloud expansion, growing IoT adoption, and the industry move from 1-gigabit to 2.5-gigabit-creates a long runway for annual recurring revenues of $100 million or more by 2028, transforming the connectivity segment into a structurally higher-margin contributor.

- Accelerated AI/ML and cloud infrastructure buildouts are increasing demand for MaxLinear's Panther storage accelerator SoC, with the company now having proof-of-concept traction at multiple hyperscale data centers; if adoption in AI-centric workloads continues, Panther could become a $150–200 million product line with industry-leading profitability, potentially adding hundreds of basis points to blended net margin.

- Global supply chain localization, the push for North American silicon and the ongoing shift to system-on-chip integration favor MaxLinear's advanced fabless model and robust technology portfolio, enabling pricing power and more resilient operating leverage-which are set to translate into expanding operating margins and structurally stronger free cash flow through industry cycles.

MaxLinear Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on MaxLinear compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming MaxLinear's revenue will grow by 23.3% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -26.0% today to 11.0% in 3 years time.

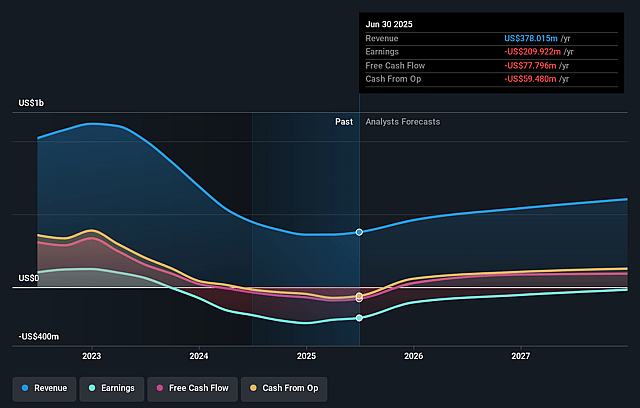

- The bullish analysts expect earnings to reach $104.8 million (and earnings per share of $1.01) by about May 2029, up from -$132.1 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $65.1 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 96.0x on those 2029 earnings, up from -59.5x today. This future PE is greater than the current PE for the US Semiconductor industry at 63.4x.

- The bullish analysts expect the number of shares outstanding to grow by 3.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.01%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- MaxLinear faces persistent customer concentration risk, as noted by their dependence on major design wins with Tier 1 carriers and module makers; the loss or delay of a key customer or the inability to win significant new contracts could lead to significant revenue declines and sharp swings in earnings.

- The semiconductor industry's move toward system-on-chip integration and larger players offering custom silicon for hyperscale data centers could marginalize MaxLinear's merchant, analog, and mixed-signal products, directly threatening their addressable market and long-term revenue growth.

- Rising geopolitical tensions and the potential escalation of trade restrictions between the US and China could disrupt MaxLinear's access to critical supply chains and fast-growing Chinese data center markets, while increased compliance costs or retaliation may add persistent pressures to net margins.

- Sustained cost pressures from foundry suppliers and the need for continued high R&D and operational investment to remain competitive with larger, vertically integrated players could squeeze MaxLinear's gross margins and result in margin compression if new products do not ramp as quickly or broadly as expected.

- A slow pace of diversification beyond current broadband, optical, and infrastructure markets or setbacks integrating new technology platforms such as silicon photonics and co-packaged optics may leave MaxLinear exposed to rapid industry shifts, contributing to revenue volatility and hindering long-term earnings potential.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for MaxLinear is $73.73, which represents up to two standard deviations above the consensus price target of $49.45. This valuation is based on what can be assumed as the expectations of MaxLinear's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $75.0, and the most bearish reporting a price target of just $28.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $954.5 million, earnings will come to $104.8 million, and it would be trading on a PE ratio of 96.0x, assuming you use a discount rate of 11.0%.

- Given the current share price of $87.73, the analyst price target of $73.73 is 19.0% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on MaxLinear?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.