Last Update 04 Jun 26

Fair value Increased 2.47%BRAV3: Mixed Ratings And Ecopetrol Deal Will Shape Future Cash Flow Profile

Brava Energia's analyst price target has been adjusted from R$22.25 to R$22.80 as analysts balance mixed recent ratings with updated assumptions on growth, margins and future P/E for the stock.

Analyst Commentary

Bullish Takeaways

- Bullish analysts highlight that the updated target price reflects confidence that Brava Energia can sustain its current margin framework, which they see as supportive of the stock's P/E assumptions.

- They point to the recent upgrade from a major global bank as a sign that some on the Street view the current valuation as reasonable relative to the company's long term earnings potential.

- Supportive views often focus on execution, with an emphasis on Brava Energia's ability to manage costs and capital spending in a way that could underpin stable cash generation over time.

- These analysts see room for the stock to track in line with their updated earnings models if management delivers consistently on operational targets that are already communicated to the market.

Bearish Takeaways

- Bearish analysts, including those behind recent downgrades at JPMorgan and another large global bank, flag concern that current P/E expectations leave limited room for error if growth or margins come in below existing assumptions.

- They question whether Brava Energia can execute fully on its planned projects without pressure on returns, which could weigh on how investors are willing to price the stock.

- Some caution that mixed ratings across the Street increase the risk of further estimate revisions if upcoming data points do not clearly support current profit and margin forecasts.

- These more cautious views frame the stock as sensitive to any setbacks in operational delivery, given that the new target price already incorporates updated, but still relatively optimistic, assumptions on earnings resilience.

What's in the News

- Ecopetrol Investimentos do Brasil LTDA proposed to acquire a 24.99% stake in Brava Energia S.A. (BOVESPA:BRAV3) for BRL 2.7b at BRL 23 per share in cash on April 23, 2026, according to M&A transaction announcements.

- In a related agreement, Ecopetrol Investimentos do Brasil LTDA entered into a Share Purchase Agreement on April 23, 2026 to acquire a 26.01% stake, equal to 120,813,490 shares, in Brava Energia S.A. from Bloco Somah Printemps Quantum, Jive Investments Consultoria Ltda, Yellowstone and others, according to M&A transaction filings.

- Ecopetrol Investimentos do Brasil LTDA intends, after these transactions, to hold a 51% controlling stake in Brava Energia S.A., subject to the purchase of enough voting shares to reach that threshold, based on the disclosed deal terms.

- The transactions are subject to customary conditions, including approval by Brazil's Administrative Council for Economic Defense (CADE), required waivers and consents related to Brava Energia's financing instruments and commercial agreements, and completion of the share purchases within the Ecopetrol Group, according to the deal documentation.

- As of May 26, 2026, the tender offer for the additional 24.99% stake had commenced and is scheduled to remain open until June 25, 2026, based on the latest M&A announcements.

Valuation Changes

- Fair Value: R$22.25 to R$22.80, reflecting a small upward adjustment in the modeled target level for the stock.

- Discount Rate: 21.17% to 20.91%, reflecting a slight reduction in the rate used to discount future cash flows.

- Revenue Growth: 2.19% to 2.73%, reflecting a modest increase in the assumed growth rate for R$ revenue.

- Net Profit Margin: 21.35% to 13.56%, reflecting a significant reduction in the projected profitability on future earnings.

- Future P/E: 7.33x to 10.73x, reflecting a higher multiple now applied to forward earnings in the valuation framework.

Key Takeaways

- Increased production, cost reductions, and efficient capital allocation enhance Brava Energia's profitability, resilience, and ability to generate steady free cash flow.

- Diversification into natural gas and export-oriented strategies positions the company to capture global energy demand shifts and benefit from favorable market dynamics.

- Exposure to declining fossil fuel demand, operational risks, regulatory pressures, and oil price volatility threaten profitability, asset value, and long-term financial stability.

Catalysts

About Brava Energia- Engages in the exploration and production of oil and natural gas in Brazil.

- Sustained increases in production from key assets (notably Atlanta and Papa-Terra), driven by new wells coming online and higher operational efficiency, position Brava to capitalize on rising energy demand in emerging markets and support potential export revenue growth; this directly benefits future revenues and EBITDA.

- Continuous reductions in lifting and operating costs-via technology adoption, asset integration, and strong operational execution-are structurally improving Brava's net margins and enabling steady free cash flow generation even in variable pricing environments.

- Optimized capital allocation (with a sharp focus on deleveraging, disciplined CapEx, and capturing synergies from recent mergers) strengthens balance sheet resilience and lowers net financial expenses, ensuring greater earnings stability and supporting future dividend capacity.

- Expansion into natural gas processing and partnerships (e.g., with PetroReconcavo and improved access to Manati capacity) aligns the company with the global movement toward cleaner transitional fuels, safeguarding long-term demand and diversifying revenue streams as hydrocarbon consumption patterns evolve.

- Enhanced capability for flexible, export-oriented commercial strategies (greater autonomy over sales contracts, improved pricing spreads, and ability to access multiple markets) allows Brava to benefit from tightening global supply and persistent underinvestment in upstream oil & gas, increasing the likelihood of structurally higher realized prices and stronger profitability.

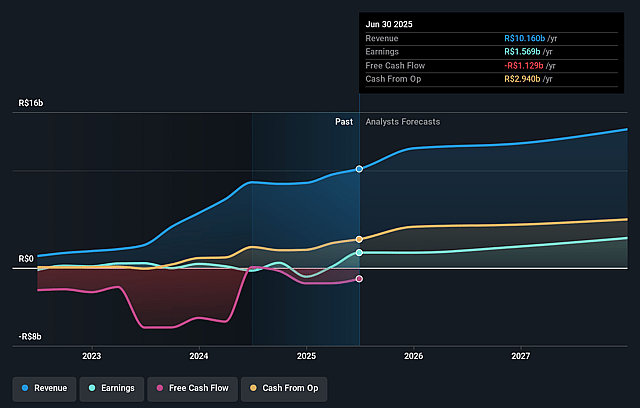

Brava Energia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Brava Energia's revenue will grow by 2.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.0% today to 13.6% in 3 years time.

- Analysts expect earnings to reach R$1.7 billion (and earnings per share of R$3.94) by about June 2029, up from R$232.4 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting R$2.9 billion in earnings, and the most bearish expecting R$903.5 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 10.7x on those 2029 earnings, down from 41.5x today. This future PE is lower than the current PE for the BR Oil and Gas industry at 12.7x.

- Analysts expect the number of shares outstanding to grow by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 20.91%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The energy transition and accelerating decarbonization policies globally could reduce long-term demand for fossil fuels, leaving Brava Energia exposed to declining hydrocarbon demand and potentially shrinking revenues and EBITDA in the coming decade.

- The company's asset base, particularly in mature onshore and offshore fields like Papa-Terra and Atlanta, remains vulnerable to natural depletion and production decline; despite current stability, any future unexpected decline could drive up lifting costs and erode net margins and earnings.

- Significant growth relies on successful execution of large, capital-intensive drilling campaigns and EOR projects; cost overruns, delays, or underperformance in these initiatives could compress free cash flow and reduce expected future profitability.

- Brava's business is highly sensitive to oil price volatility and relies on favorable spreads and hedges-market downturns, narrowing spreads, or policy-driven price pressure could quickly weaken revenues and operating cash flows.

- Increasing ESG constraints, regulatory and environmental compliance requirements, as well as the risk of higher future taxes or penalties specific to oil and gas in Brazil, could inflate costs, raise the cost of capital, and put sustained pressure on net income and overall share valuation.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of R$22.8 for Brava Energia based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$27.0, and the most bearish reporting a price target of just R$17.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be R$12.9 billion, earnings will come to R$1.7 billion, and it would be trading on a PE ratio of 10.7x, assuming you use a discount rate of 20.9%.

- Given the current share price of R$20.75, the analyst price target of R$22.8 is 9.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Brava Energia?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.