Last Update 17 Jun 26

PEN: Pulmonary Embolism Trial And Merger Approval Will Support Stronger Outlook

Analysts have maintained their Penumbra price target at approximately $363, noting only minor adjustments to factors such as the discount rate, assumptions about long-term revenue growth and profit margins, and the projected future P/E multiple.

What’s in the News for Penumbra

- Boston Scientific announced plans to acquire Penumbra, with Artisan Partners highlighting the deal as confirmation of its prior investment thesis in Penumbra stock and using the transaction to exit its position. [Source: recent news reports]

- Penumbra received FDA clearance for its THUNDERBOLT device, described as the first computer assisted vacuum thrombectomy system tailored to treat acute ischemic stroke and powered by the Penumbra Engine. [Source: recent news reports]

- THUNDERBOLT also secured CE Mark approval in Europe, supporting Penumbra’s plans to launch the device globally as part of its broader neuro thrombectomy portfolio. [Source: recent news reports]

- Penumbra shareholders recently approved a merger with Boston Scientific Corporation, which is expected to combine Penumbra’s catheter and CAVT technology with Boston Scientific’s scale and distribution. [Source: recent news reports]

- Penumbra reported 90 day results from the STORM PE randomized controlled trial, where patients with intermediate high risk pulmonary embolism treated with computer assisted vacuum thrombectomy plus anticoagulation showed greater functional improvement than those receiving anticoagulation alone, with similar safety through 90 days. [Source: company event disclosures]

Valuation Changes for Penumbra Stock

- Fair Value: The modeled fair value remains unchanged at approximately $363.36 per share.

- Discount Rate: The discount rate has fallen slightly from 7.57% to about 7.48%.

- Revenue Growth: The long-term annual dollar revenue growth assumption is effectively unchanged at around 12.75%.

- Net Profit Margin: The modeled net profit margin remains effectively stable at roughly 14.96%.

- Future P/E: The assumed future P/E multiple has edged down slightly from about 58.04x to 57.89x.

Key Takeaways

- New clinical trials and innovative product launches are expected to drive market adoption, improve margins, and accelerate growth in large, underpenetrated therapy areas.

- Expanding globally with an enhanced sales force and continued investment in data and technology supports sustainable earnings, better pricing, and long-term competitive strength.

- Heavy product and geographical dependencies, intensifying competition, and regulatory pressures threaten margins and revenue growth despite ongoing investment in R&D and sales expansion.

Catalysts

About Penumbra- Designs, develops, manufactures, and markets medical devices in the United States and internationally.

- The soon-to-be-released STORM-PE randomized trial is poised to provide Level 1 evidence comparing Penumbra's thrombectomy technology to standard anticoagulation for pulmonary embolism; a positive outcome could expand guideline adoption, significantly accelerate procedure volumes, and drive substantial revenue growth by rapidly increasing penetration in a very underpenetrated, large market.

- Penumbra's new product launches (notably RUBY XL in embolization and the planned Thunderbolt in neurovascular thrombectomy) and the expansion of specialized sales teams are set to improve product adoption and support higher-margin product mix, which should meaningfully impact gross margins and overall earnings as these innovations take share from open surgery and older alternatives.

- As global demographics shift-driven by rising stroke and vascular disease rates and an aging population-Penumbra's focus on minimally invasive therapies addresses a growing clinical need, positioning the company to benefit from secular increases in procedure volumes and supporting sustained, long-term revenue and earnings growth.

- International business is recovering following prior headwinds in China and other markets, and with recent launches of products like Flash 2.0 and Bolt lines abroad, Penumbra expects broader global demand, diversified revenue streams, and increased operating leverage as its expanded sales infrastructure matures.

- Ongoing investment in high-quality clinical data generation and further technology integration enables Penumbra to stay ahead of evolving reimbursement frameworks, which are increasingly favoring advanced, outcome-driven therapies-ultimately supporting premium pricing, improved net margins, and a durable competitive advantage over less-innovative peers.

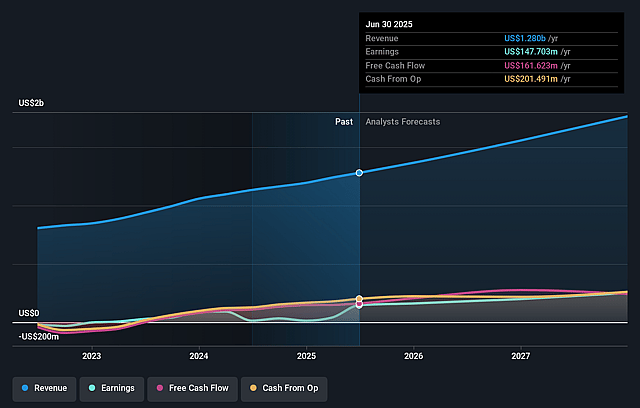

Penumbra Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Penumbra's revenue will grow by 12.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.8% today to 15.0% in 3 years time.

- Analysts expect earnings to reach $311.7 million (and earnings per share of $7.93) by about June 2029, up from $171.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $381.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 58.4x on those 2029 earnings, down from 73.2x today. This future PE is greater than the current PE for the US Medical Equipment industry at 24.9x.

- Analysts expect the number of shares outstanding to grow by 0.85% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.48%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition from both large medtech companies and agile startups could drive commoditization of thrombectomy and embolization devices, leading to margin compression and limiting Penumbra's pricing power-potentially impacting long-term revenue growth and profitability.

- Heightened product concentration risk is evident, as Penumbra remains heavily reliant on its neurovascular and vascular intervention franchises; any technological innovation by competitors or adverse data from pivotal clinical trials (such as STORM-PE or Thunderbolt) could materially disrupt future revenue streams.

- Increasing international regulatory scrutiny and recent headwinds in China point to ongoing vulnerability in global markets; prolonged approval timelines, trade-related barriers, or recurring regional setbacks could hinder international expansion and suppress revenue growth.

- Elevated SG&A expenses and high ongoing investments in sales force expansion and R&D may pressure operating margins-particularly if anticipated revenue synergies from new hires or product launches (such as RUBY XL and the split Embo/thrombectomy sales teams) are slower to materialize than projected.

- Industry trends toward value-based healthcare and cost-containment may push hospitals and payers to negotiate lower prices and reimbursement for intervention devices, which could erode Penumbra's gross and net margins and limit earnings growth even as procedures increase.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $363.36 for Penumbra based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $374.0, and the most bearish reporting a price target of just $326.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.1 billion, earnings will come to $311.7 million, and it would be trading on a PE ratio of 58.4x, assuming you use a discount rate of 7.5%.

- Given the current share price of $318.46, the analyst price target of $363.36 is 12.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Penumbra?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.