Last Update 28 Apr 26

Fair value Decreased 10%RATO B: Recalibrated Multiples And Dividend Commitment Will Support Future Upside

Analysts have reduced the Ratos price target from SEK 48 to SEK 43, reflecting a more cautious stance following recent research that takes into account updated assumptions on the discount rate, revenue growth, profit margin, and future P/E multiples.

Analyst Commentary

Bullish Takeaways

- Bullish analysts see the lower price target as aligning expectations more closely with current assumptions on the discount rate and P/E multiples. They view this as a cleaner entry framework for long term investors.

- Some highlight that valuation work now reflects more conservative revenue growth and margin assumptions. They argue this reduces the risk of further sharp target changes if execution tracks these updated inputs.

- Supportive views also point to the idea that, with a reduced target, there may be less reliance on aggressive multiple expansion and more focus on operational delivery to justify any future upside.

- For bullish analysts, the recalibrated target is seen as a way to keep expectations grounded while still leaving room for better than modelled execution on profitability or capital allocation.

Bearish Takeaways

- Bearish analysts view the cut in the price target as a sign that risks around revenue growth, margin delivery and valuation are more front and center than before. They note this may weigh on near term sentiment.

- The more cautious stance on future P/E multiples is seen as a reflection of reduced confidence in the company securing a premium valuation without clearer evidence on consistent execution.

- There is concern that if revenue growth and profit margins only meet the updated, more conservative assumptions, upside to the new target may be limited, with less room for error in future quarters.

- Some bearish analysts see the downgrade and lower target as an indication that the risk reward profile has shifted. In their view, investors may need to pay closer attention to how management delivers against these tighter assumptions.

What's in the News

- Ratos AB (publ) announced an annual dividend of SEK 1.4000 per share, with payment scheduled for April 1, 2026, an ex-dividend date of March 26, 2026, and a record date of March 27, 2026 (Key Developments).

Valuation Changes

- Fair Value: Target moved from SEK 48 to SEK 43, a reduction of roughly 10% in the modelled fair value per share.

- Discount Rate: Assumption adjusted from 7.42% to 7.59%, a small increase that generally raises the required return in the valuation model.

- Revenue Growth: Long term revenue growth input shifted from 2.55% to 2.73%, a slight uplift in the expected growth rate expressed in the model.

- Net Profit Margin: Margin assumption moved from 6.23% to 6.22%, effectively unchanged in the updated work.

- Future P/E: Forward P/E multiple reduced from 15.18x to 13.61x, indicating a lower valuation multiple applied to future earnings in the revised analysis.

Key Takeaways

- Strategic focus on sustainable infrastructure and high-growth sectors, supported by acquisitions and operational efficiency, is driving profitability and margin expansion.

- Stable demand for core services and portfolio streamlining are delivering recurring revenue, improved earnings quality, and sustainable long-term growth.

- Currency volatility, weak core markets, restructuring risks, external dependencies, and rising leverage all threaten margins, earnings stability, and the company's long-term shareholder value.

Catalysts

About Ratos- A private equity firm specializing in buyouts, turnarounds, add on acquisitions, and middle market transactions.

- Accelerated shift towards sustainable and energy-efficient solutions, especially in construction and energy services, is increasing demand and expanding project backlogs for Ratos' critical infrastructure holdings (supports future revenue growth).

- Massive long-term investments required to upgrade and maintain aging European infrastructure are driving stable demand for Ratos' services in construction, maintenance, and industrial segments (favors stable, recurring cash flows and revenue).

- Ongoing portfolio streamlining toward more profitable sectors and deliberate exit from lower-performing or volatile businesses are improving earnings quality and supporting higher net margins.

- Active bolt-on acquisition strategy within stable, high-growth platforms is generating operational synergies and scale benefits, underpinning EBITDA margin expansion and longer-term topline growth.

- Implementation of operational excellence and cost efficiency programs across the group is boosting profitability, enhancing return on capital employed (ROCE), and supporting sustainable EPS growth.

Ratos Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Ratos's revenue will grow by 2.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from -4.7% today to 6.2% in 3 years time.

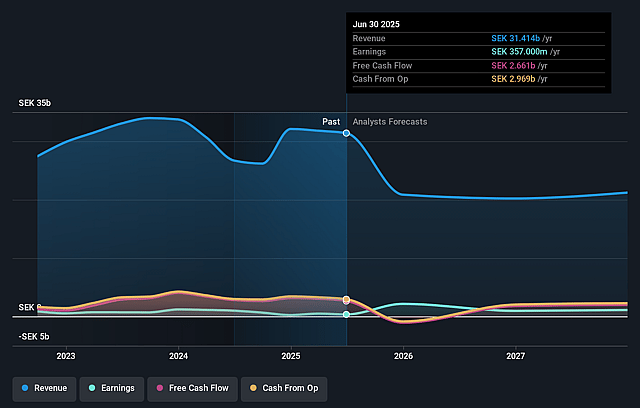

- Analysts expect earnings to reach SEK 1.3 billion (and earnings per share of SEK 3.92) by about April 2029, up from -SEK 901.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 13.6x on those 2029 earnings, up from -11.9x today. This future PE is lower than the current PE for the GB Capital Markets industry at 18.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.59%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Exposure to currency volatility, particularly the strengthening of the Swedish Krona against the Norwegian Krone, has negatively impacted margins and sales; persistent FX headwinds could continue to erode earnings and dampen revenue growth.

- Continued soft market conditions in core segments like Industrial Services and subdued performance in slowing end-markets such as biotech signal possible stagnation or even decline in underlying organic growth, which could weigh on consolidated revenue and long-term earnings momentum.

- Execution risk from ongoing restructuring, divestments (e.g., airteam, potential future Consumer exits), and reliance on bolt-on acquisitions to drive growth may lead to lower-than-expected synergies or integration challenges, risking lower net margins and future profitability.

- Dependence on external factors such as unpredictable weather (noted in Plantasjen performance) and calendar effects can significantly impact sales and margins for key portfolio businesses, creating earnings volatility and limiting the reliability of margin expansion targets.

- A rise in gearing (leverage up from 1.2 to 1.7) despite claims of a strong balance sheet, combined with the uncertainty around future deployment of proceeds from divested assets, introduces financial risk; if capital is not invested or returned accretively (e.g., unprofitable M&A, delayed buybacks), shareholder value and EPS growth could suffer.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of SEK43.0 for Ratos based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be SEK20.7 billion, earnings will come to SEK1.3 billion, and it would be trading on a PE ratio of 13.6x, assuming you use a discount rate of 7.6%.

- Given the current share price of SEK32.86, the analyst price target of SEK43.0 is 23.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Ratos?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.