Last Update 23 Jun 26

Fair value Decreased 4.40%LAND: Gas IoT Expansion And Higher Future P E Support Bullish Outlook

Analysts have trimmed their price target on Landis+Gyr Group to CHF 55 from CHF 59. This reflects updated views on fair value, discount rate, growth, margins and future P/E assumptions cited in recent research.

Analyst Commentary

Recent research on Landis+Gyr Group, including the revised CHF 55 price target from JPMorgan, gives a clearer view of how analysts are weighing the company’s execution, valuation, and growth profile.

Bullish Takeaways

- Bullish analysts see the maintained Neutral stance alongside the CHF 55 target as a signal that Landis+Gyr Group is still viewed as reasonably valued relative to current fundamentals, even after adjustments to key assumptions.

- The updated target reflects refreshed views on growth, margins and future P/E, which suggests that earnings visibility and business mix are still viewed as supportable within the revised fair value range.

- The relatively modest cut from CHF 59 to CHF 55 points to continued confidence that Landis+Gyr Group’s core business can justify a P/E that aligns with sector norms reflected in the new target.

- Investors may take comfort that analysts are actively recalibrating their models, which can help keep the share price more closely tied to current expectations for cash flows and profitability.

Bearish Takeaways

- Bearish analysts may view the repeated reductions in the price target as a signal that prior expectations for growth, margins or achievable P/E were too optimistic, prompting a more conservative stance.

- The lower fair value estimate suggests there could be less upside than previously thought if Landis+Gyr Group does not deliver on execution or if margin assumptions prove difficult to reach.

- The Neutral rating paired with a reduced target can be read as a sign that, at current levels, the risk and reward profile appears more balanced than compelling.

- Some investors might interpret the multiple target cuts as a warning that valuation now depends more heavily on disciplined cost control and stable earnings rather than strong growth acceleration.

What’s in the News for Landis+Gyr Group

- Landis+Gyr partnered with Origin Energy to digitise parts of Australia’s gas network using large scale IoT solutions. The project includes an 18 month rollout of intelligent modules, communications technology, and a data platform across existing metering assets, while maintaining LPG supply to customers. [Source: Company client announcement]

- The Origin project is described as one of the first large scale efforts in Australia to fully digitise gas operations across an entire customer base. Management indicates the approach could later be applied to around 2,000,000 existing Landis+Gyr gas meters across the country. [Source: Company client announcement]

- Landis+Gyr received New York Public Service Commission approval for its SurentT G480 ultrasonic gas meter, the first ultrasonic gas meter authorized for use in New York State after testing at National Grid’s standards laboratory. [Source: Product related announcement]

- The SurentT G480 meter combines solid state ultrasonic measurement, integrated communications via the Gridstream Connect IoT network, an integrated shutoff valve that exceeds ASME B16.33 gas tightness requirements, and a stated 2 year battery life. It is already being deployed by utilities across the Midwest and surrounding regions. [Source: Product related announcement]

- Landis+Gyr joined EPRI’s Open Power AI Consortium, which aims to develop open source AI and GenAI models, datasets, and an AI Sandbox focused on electric utility use cases such as operational efficiency, resiliency, reliability, cost management, and customer experience. [Source: Company client announcement]

Valuation Changes for Landis+Gyr Group

- Fair value revised from CHF 64.87 to CHF 62.01, implying a modest downward adjustment to the intrinsic value estimate used in the model.

- Discount rate increased from 5.93% to 6.40%, indicating a slightly higher required return being applied to Landis+Gyr Group’s projected cash flows.

- Revenue growth moved from a prior assumption of declining 5.76% to an updated assumption of growing 4.38%, reflecting a shift from a contraction scenario to a modest expansion in revenue expectations.

- Profit margin reduced from 16.20% to 8.75%, pointing to a materially lower assumed earnings margin on future sales in the refreshed model.

- Future P/E raised from 12.50x to 21.49x, meaning the valuation framework now applies a significantly higher earnings multiple to Landis+Gyr Group’s projected profits.

Key Takeaways

- Strategic focus on Americas and expanding software revenue may drive growth in revenue and EBITDA margins through integrated energy management solutions.

- U.S. listing and operational improvements in EMEA and APAC aim to enhance capital access, margins, and regional profitability.

- The company's financial performance is threatened by regional revenue declines, uncertain restructuring, cash flow issues, and instability from key executive departures.

Catalysts

About Landis+Gyr Group- Provides integrated energy management solutions to utility sector in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

- The strategic focus on the highly profitable Americas business could lead to enhanced revenue growth and adjusted EBITDA margins, driven by stronger emphasis on integrated edge-to-enterprise energy management solutions.

- Increasing software revenues, which now represent 24% of total revenues, and the strategic transformation investments signal potential for higher revenue growth and improved net margins through more recurring revenue generation.

- The potential listing in the U.S. may increase access to a larger pool of capital and facilitate comparisons with peers, possibly leading to increased investor interest and potentially impacting earnings positively.

- Supply chain improvements, operational efficiencies, and regional optimization in EMEA could result in higher net margins and increased profitability in the region.

- Expansion in APAC with growing software and services offerings, especially in high-potential markets like Australia and India, is likely to support future revenue and earnings growth.

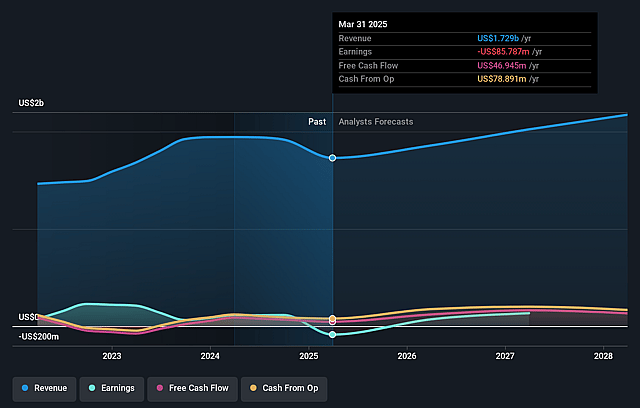

Landis+Gyr Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Landis+Gyr Group's revenue will grow by 4.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.3% today to 8.7% in 3 years time.

- Analysts expect earnings to reach $116.0 million (and earnings per share of $4.24) by about June 2029, up from $38.9 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $140.7 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 21.6x on those 2029 earnings, down from 43.0x today. This future PE is lower than the current PE for the GB Electronic industry at 66.2x.

- Analysts expect the number of shares outstanding to decline by 1.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.4%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The decline in the EMEA region's revenue, due to timing of large project rollouts, market softness in key areas like the U.K. and Turkey, and reduced demand for EV solutions, could negatively impact overall net revenue and profitability.

- The strategic review of the EMEA region, which considers options such as selling parts or all of the business, introduces uncertainty and potential restructuring costs that could affect earnings and margins.

- Challenges in the APAC region, such as project timing issues leading to revenue declines, might continue to strain the company's revenue generation capability.

- Elevated inventory levels impacting free cash flow, which was reported as negative, indicate a risk to liquidity and could affect earnings if not normalized as expected.

- The departure of key executives, like the Group CFO and regional heads, poses execution risk that could impact strategic initiatives and financial performance by creating instability within management.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CHF62.01 for Landis+Gyr Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF76.36, and the most bearish reporting a price target of just CHF51.47.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.3 billion, earnings will come to $116.0 million, and it would be trading on a PE ratio of 21.6x, assuming you use a discount rate of 6.4%.

- Given the current share price of CHF47.55, the analyst price target of CHF62.01 is 23.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Landis+Gyr Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.