Last Update 21 May 26

Fair value Decreased 10%SQNS: Revised P/E Assumptions Will Shape Long Term Earnings Repricing

Analysts have trimmed their price targets on Sequans Communications by $2 to $3, citing updated assumptions around fair value, discount rate, revenue growth, profit margin and future P/E that collectively support a lower but still valuation-focused target range.

Analyst Commentary

Recent research updates on Sequans Communications focus on refining assumptions for fair value, discount rate, revenue growth, profit margin and future P/E. Even with lower price targets, analysts frame these changes as adjustments to their models rather than a wholesale shift in how they view the stock.

Bullish Takeaways

- Bullish analysts continue to rely on valuation models that still support upside potential relative to current trading levels, even after trimming targets by US$2 to US$3.

- The updated assumptions around future P/E suggest that, under their revised scenarios, Sequans could still screen as reasonable on earnings-based metrics once profitability goals are met.

- Adjustments to revenue growth and margin inputs are presented as fine tuning, which implies analysts still see a path to scaling the business model, even if it takes longer or is less aggressive than previously assumed.

- The focus on fair value and discount rate indicates that analysts are continuing to underwrite a long term thesis rather than abandoning prior expectations around execution or market opportunity.

Bearish Takeaways

- Bearish analysts point to lower revenue growth assumptions as a key reason for reducing price targets by US$2 to US$3, which directly pressures valuation outcomes in their models.

- Reduced profit margin expectations suggest concerns that the company may face ongoing cost or pricing headwinds, which could limit earnings power versus earlier forecasts.

- Higher or more conservative discount rate assumptions reflect greater caution around execution risk and cash flow visibility, leading to a lower present value in discounted cash flow style work.

- Recalibrated future P/E assumptions indicate less willingness to assign premium multiples without clearer evidence of consistent profitability and growth delivery, which restrains target prices.

What's in the News

- Completed share repurchase of 1,516,973 shares, representing 9.73%, for US$9.31 million under the buyback announced on September 30, 2025 (Key Developments).

- Reported a period from September 30, 2025 to September 30, 2025 with no shares repurchased and no cash deployed under the same buyback authorization (Key Developments).

- Announced on April 30, 2026 that the company will be unable to file its next Form 20 F with the SEC by the required deadline (Key Developments).

Valuation Changes

- Fair value was reduced from $12.50 to $11.25, indicating a modest step down in the modeled equity value.

- The discount rate moved slightly higher from 13.43% to 13.56%, reflecting a small increase in the required return used in the models.

- Revenue growth was adjusted from 46.40% to 55.47%, pointing to a higher projected top-line expansion rate in the updated assumptions.

- The net profit margin was revised from 2.46% to 16.55%, implying a materially higher expected earnings contribution per dollar of revenue in the new scenario.

- The future P/E was cut from 142.47x to 15.96x, showing a substantial reduction in the multiple applied to projected earnings.

Key Takeaways

- Accelerating IoT product launches, new RF transceivers, and 5G platform development are positioning Sequans for revenue growth and expansion into high-margin, diversified markets.

- Increased focus on IP monetization and disciplined cost control could improve margins and earnings quality, reducing concerns about sustained losses.

- Sequans' shift to a Bitcoin-focused treasury strategy raises earnings volatility, shareholder dilution, heightened financial risk, and uncertainty around profitability and future cash flow.

Catalysts

About Sequans Communications- Engages in the fabless designing, developing, and supplying of cellular semiconductor solutions for massive and broadband internet of things markets.

- Product revenue from the IoT business is expected to ramp significantly through the second half of 2025 and into 2026, as a large pipeline of design wins (~$250 million) transitions to mass production-this dynamic aligns with robust adoption of connected devices across industries, set to drive meaningful revenue growth.

- Sequans' launch of new RF transceiver products targeting high-value markets such as defense, drones, and automotive, combined with strong early design win momentum, supports long-term expansion into diversified verticals with premium gross margins and higher earnings potential.

- Ongoing development of next-generation 5G IoT platforms (eRedCap 5G), with customer interest fueled by seamless upgrade paths from 4G, positions Sequans to capture additional share in the accelerating 5G/IoT buildout, expanding its addressable market and future revenue base.

- Expanded focus on monetizing the company's intellectual property portfolio through licensing and royalty arrangements-including new agreements and anticipated recurring royalties starting in 2026-has the potential to boost high-margin income streams, improving net margins.

- Management's continued discipline in cost containment, government R&D support, and progress toward expected operational cash flow breakeven in the second half of 2026 could catalyze a re-rating of earnings quality and reduce perceived risk around sustained losses.

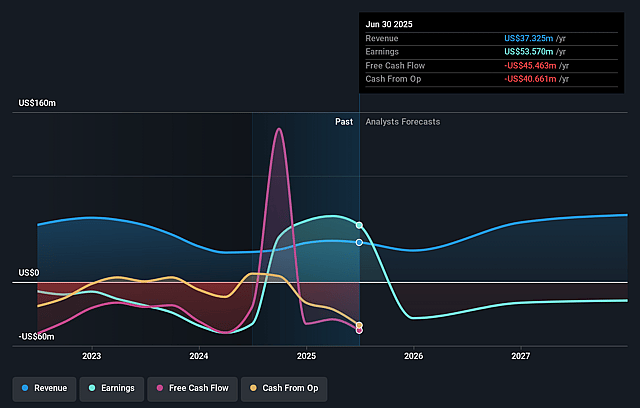

Sequans Communications Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Sequans Communications's revenue will grow by 55.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -81.6% today to 16.5% in 3 years time.

- Analysts expect earnings to reach $19.6 million (and earnings per share of $1.2) by about May 2029, up from -$25.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.0x on those 2029 earnings, up from -2.5x today. This future PE is lower than the current PE for the US Semiconductor industry at 63.0x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.56%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Sequans' heavy pivot to a Bitcoin treasury strategy introduces significant earnings volatility and risk of impairment losses, as its financials will become exposed to Bitcoin price swings and accounting rules limit the recognition of unrealized gains, increasing potential for reported net losses and reducing predictability for shareholders.

- The company plans to continue growing its Bitcoin holdings through ongoing equity and debt issuance, resulting in repeated shareholder dilution, higher interest costs, and growing leverage-all of which could erode EPS, compress net margins, and heighten financial risk in the long term.

- Reliance on monetizing intellectual property and future licensing income to support both its operating business and Bitcoin strategy creates uncertainty; if anticipated licensing and royalty revenues fail to materialize, Sequans may face cash flow constraints, impairing its ability to fund operations and further Bitcoin purchases, which would affect overall revenue and margins.

- Sequans' IoT business, while showing some growth and design win momentum, remains relatively small compared to larger competitors, with recent quarterly net losses and shrinking cash balances; persistent inability to achieve sustained profitability and cash-flow breakeven could undermine investor confidence and pressure future earnings.

- Long-term industry trends of accelerating integration and custom silicon by major device makers, coupled with intensifying competition from larger, vertically integrated semiconductor firms, pose a risk of margin compression and loss of market share, negatively impacting both revenue growth and long-term earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $11.25 for Sequans Communications based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $7.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $118.5 million, earnings will come to $19.6 million, and it would be trading on a PE ratio of 16.0x, assuming you use a discount rate of 13.6%.

- Given the current share price of $4.3, the analyst price target of $11.25 is 61.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Sequans Communications?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.