Last Update 17 Jun 26

HLI: Lowered Return Assumptions Will Pressure P/E And Future Share Price

Analysts have trimmed their price target on Helia Group shares by A$5, reflecting updated assumptions around discount rates, revenue trends, and future P/E expectations, while keeping fair value estimates broadly unchanged.

Analyst Commentary

Recent research on Helia Group focuses on how updated assumptions flow through to valuation, especially around discount rates, revenue trajectories, and future P/E settings used in models.

Across the latest reports, analysts have revised price targets for Helia Group shares while aiming to keep their overall fair value frameworks aligned with the updated inputs rather than wholesale changes in company thesis.

Bullish Takeaways

- Bullish analysts view the A$5 price target trim as a recalibration to new discount rate and earnings assumptions, rather than a shift in how they see Helia Group’s core business.

- Some point to the use of future P/E multiples that they still consider reasonable for the company’s profile, suggesting they see room for the share price to better reflect their valuation work if execution holds up.

- There is continued emphasis on Helia Group’s ability to align its revenue outlook with the updated models, which supports the view that fair value can remain broadly stable despite the headline target change.

- Adjustments are being framed as a tidy up of models, which signals that bullish analysts still see the current share price as closely linked to their long term valuation range.

Bearish Takeaways

- Bearish analysts highlight that the lower price targets reflect more cautious assumptions on revenue trends, indicating concerns around how future earnings streams may track against prior expectations.

- Higher or more conservative discount rates in models point to a greater focus on risk and the timing of cash flows, which can put pressure on Helia Group’s implied valuation.

- The reset in P/E expectations used for later forecast years suggests some hesitation around how much investors may be willing to pay for Helia Group’s earnings profile over time.

- Target cuts are interpreted by cautious analysts as a signal that, even if fair value is described as broadly unchanged, the margin for error in execution and growth delivery is viewed as tighter than before.

What’s in the News for Helia Group

- Helia Group appointed Mark Senkevics as CEO, with plans for him to join the company before 1 December 2026. He will take over from Interim CEO Michael Cant, who has served in the interim role since 1 July 2025. Source: Key Developments

- Senkevics brings more than 25 years of insurance industry experience, including senior roles at Steadfast Group and Swiss Re Group across Australia and the broader Asia Pacific region, along with board and committee roles at several Australian financial industry bodies. Source: Key Developments

- Helia Group confirmed that Craig Ward will be appointed Chief Financial Officer from 1 July 2026, after serving as Interim CFO since 1 July 2025. Source: Key Developments

- The transition from interim to permanent CEO and CFO roles reflects a planned leadership handover period running from mid 2025 to mid 2026 for Helia Group. Source: Key Developments

Valuation Changes for Helia Group

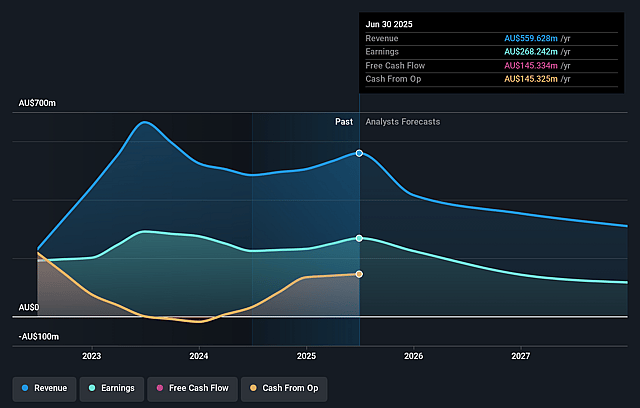

- Fair Value: The A$4.27 fair value estimate is unchanged, indicating no adjustment to the core valuation output in the latest update.

- Discount Rate: The discount rate has fallen slightly to 7.08%, a small tweak from 7.12% that marginally affects how future cash flows are weighted.

- Revenue Growth: Forecast revenue growth remains a decline of 18.71%, with no meaningful change in the projected top line trend for Helia Group.

- Net Profit Margin: The forecast profit margin is effectively unchanged at 43.73%, signalling a stable earnings margin assumption in the models.

- Future P/E: The future P/E multiple has edged down slightly to 12.72x from 12.73x, indicating a minor adjustment to the valuation multiple applied to Helia Group’s projected earnings.

Key Takeaways

- Loss of major clients and government policy changes will sharply shrink Helia's core market and pressure future revenue growth.

- Heavy capital returns risk undermining strategic reinvestment, threatening competitive positioning and future profitability.

- Strong capital management, resilient historical earnings, and adaption to client shifts support Helia's robust market position and profitability amid near-term sector and client pressures.

Catalysts

About Helia Group- Helia Group Limited, together with its subsidiaries, is involved in the loan mortgage insurance business primarily in Australia.

- The loss of two major lender clients (Commonwealth Bank and ING), who represented 61% of recent gross written premium, is expected to sharply reduce Helia's new business volumes from 2026 onward, putting future revenue at risk and increasing earnings volatility.

- The government's expanded Home Guarantee Scheme (removal of caps, higher property price thresholds, and relaxed eligibility) will further displace private mortgage insurance in the first homebuyer segment, removing a market that contributed 25–30% of GWP, which is likely to materially depress premium growth and future revenue.

- Increased prevalence of government-backed and self-insured home loan solutions, combined with waivers by lenders, is set to shrink Helia's addressable market, limiting the runway for long-term top-line growth and amplifying revenue pressures.

- Reliance on exceptionally low claims and favorable investment returns is currently elevating net margins and profits, but these are cyclical and non-sustainable; normalization of claims ratios and investment returns could quickly compress margins and lower future earnings.

- The company's focus on returning excess capital via special dividends and buybacks, while positive for short-term shareholder returns, may inhibit Helia's ability to strategically reinvest in technology and innovation, causing potential long-term erosion in competitive positioning and return on equity.

Helia Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Helia Group's revenue will decrease by 18.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 51.2% today to 43.7% in 3 years time.

- Analysts expect earnings to reach A$112.5 million (and earnings per share of A$0.47) by about June 2029, down from A$244.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 12.7x on those 2029 earnings, up from 5.7x today. This future PE is lower than the current PE for the AU Diversified Financial industry at 14.5x.

- Analysts expect the number of shares outstanding to grow by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.08%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Helia maintains a dominant 50% market share in its in-force LMI portfolio, which provides a substantial buffer of unearned revenue (via LRC and CSM) to underpin future revenues and earnings even as new business volumes face short-term pressure.

- The company's exceptionally strong capital position and capital management discipline, evidenced by ongoing dividends, special dividends, and share buybacks, offer significant financial flexibility for shareholder returns and smoothing of EPS and ROE, mitigating revenue volatility in the near-term.

- Despite the loss of major clients (CBA and ING) and government scheme pressures, Helia has achieved a 28% YoY increase in gross written premium from new and renewed customer activity, demonstrating an ability to grow market share among regional/second-tier lenders and adapt its client risk settings, which may partially offset top-line declines.

- The long duration and seasoning of Helia's back book-with revenue recognition extending up to 15 years-means historical premium earnings will continue to support reported revenues and profit generation, providing a multi-year runway for strategic business adjustment and cost transformation.

- Current favorable macro trends-such as low unemployment, rising house prices nationwide, persistent low claims, and resilience in household balance sheets-support continued low loss ratios and strong bottom-line profitability, insulating Helia's margins and NPAT against immediate sector headwinds.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$4.27 for Helia Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$4.9, and the most bearish reporting a price target of just A$3.7.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be A$257.1 million, earnings will come to A$112.5 million, and it would be trading on a PE ratio of 12.7x, assuming you use a discount rate of 7.1%.

- Given the current share price of A$5.13, the analyst price target of A$4.27 is 20.2% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Helia Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.