Last Update 14 Apr 26

Fair value Decreased 0.50%LICHSGFIN: Upcoming Board And Budget Decisions Will Support Confidence In Future Earnings

Analysts have trimmed their price target for LIC Housing Finance by about ₹3 to roughly ₹594, reflecting slightly higher discount rate assumptions and fine tuned expectations for revenue growth, profit margin and future P/E.

What's in the News

- A board meeting is scheduled for Jan 30, 2026 at 14:30 Indian Standard Time to review the unaudited standalone and consolidated financial results for the third quarter and nine months ended Dec 31, 2025, along with the limited review report (company filing).

- A special or extraordinary shareholders meeting will be held on Mar 13, 2026 via postal ballot in India to consider the reappointment of Smt. Jagennath Jayanthi (DIN: 09053493) as an independent director (company filing).

- A board meeting is set for Mar 25, 2026 at 14:30 Indian Standard Time to consider and approve the budget for the 2026 to 2027 financial year, including funding through loans and or issues of redeemable non convertible debentures (company filing).

Valuation Changes

- Fair Value: Trimmed slightly from ₹597.08 to about ₹594.08 per share, a cut of roughly ₹3.

- Discount Rate: The assumption was raised marginally from 13.02% to about 13.09%, implying a modestly higher required return in the model.

- Revenue Growth: The forecast was adjusted slightly from 9.45% to about 9.44%, indicating a very small recalibration of growth expectations.

- Net Profit Margin: The margin assumption was nudged up from 57.97% to about 58.09%, reflecting a minor tweak to profitability inputs.

- Future P/E: The forward P/E multiple in the model inched down from 7.39x to about 7.36x, pointing to a slightly more conservative valuation multiple.

Key Takeaways

- Lower funding costs, government support, and ongoing digitization are expected to drive margin stability, recurring income, and future profitability.

- Asset quality improvement and expansion into affordable housing suggest stronger long-term growth potential despite current competition.

- Conservative approach amid rising competition and asset quality concerns may constrain growth, profitability, and market agility, while cautious lending limits diversification and revenue opportunities.

Catalysts

About LIC Housing Finance- A housing finance company, provides loans for the purchase, construction, repair, and renovation of houses/buildings in India.

- Lower interest rates, government incentives for affordable housing, and ongoing urbanization in India are expected to drive a sustained increase in mortgage demand, which could boost LIC Housing Finance's loan disbursements and revenue over the coming quarters.

- The company's funding costs have declined meaningfully due to recent liquidity infusions and rate cuts by the RBI, while further reductions are expected; this funding advantage, when paired with a strong parent brand (LIC), should help support stable net interest margins and improve future profitability.

- Expanded use of digitized processes, monthly and quarterly loan repricing, and improved customer retention mechanisms (such as internal interest rate rewriting programs) position LIC Housing Finance to defend its loan book, limit balance transfers, and support recurring income, aiding both revenue growth and margin stability.

- Asset quality continues to improve, as seen in lower Stage 3 NPAs YoY, with management focused on intensified recovery operations and prudent, phased project finance disbursal-a trend that, if sustained, should result in lower credit costs and provision expenses, thus aiding net earnings.

- With rising financial inclusion and greater mortgage penetration in tier 2/3 cities and semi-urban/rural locations, coupled with the company's cautious expansion into high-margin affordable housing, there is material long-term potential for loan book growth and higher future earnings if current competitive pressures subside.

LIC Housing Finance Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

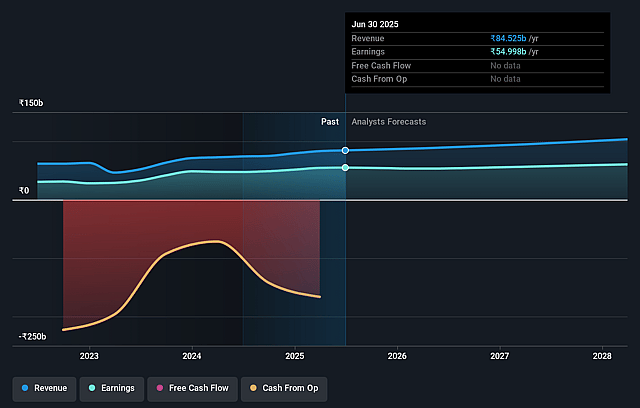

- Analysts are assuming LIC Housing Finance's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 65.1% today to 58.1% in 3 years time.

- Analysts expect earnings to reach ₹64.1 billion (and earnings per share of ₹116.21) by about April 2029, up from ₹54.8 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 7.4x on those 2029 earnings, up from 5.2x today. This future PE is lower than the current PE for the IN Diversified Financial industry at 22.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.09%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition from both public sector and private sector banks, which can offer home loans at similar or even lower interest rates due to direct repo rate linkage, is pressuring LIC Housing Finance's loan growth and requiring rate cuts; sustained rate wars may squeeze net interest margins and limit revenue growth.

- Management's explicit prioritization of protecting margins over loan growth-in the face of strong competition and balance transfer pressures-could result in below-industry-average loan book growth over the long term, impacting top-line revenue expansion and overall earnings trajectory.

- Asset quality, particularly in the retail/Individual Home Loan segment, showed signs of stress with increased NPAs and Stage 3 assets in Q1, and despite management's optimism, persistent collection inefficiencies or a weaker macro environment could lead to elevated credit costs, higher provisioning, and reduced net profits.

- The company remains cautious and slow on project finance lending due to past high NPAs (over 50% at one point in that segment), which, while limiting risk, may also constrain future growth opportunities relative to peers venturing more aggressively into this potentially higher-margin segment, thus impacting revenue diversification.

- LIC Housing Finance's slower adoption of riskier but growing segments like affordable housing (despite industry tailwinds here) and ongoing reliance on wholesale funding-versus granular retail deposits-could leave it less agile in capturing market share and more vulnerable to funding cost volatility, thereby affecting long-term profitability and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹594.08 for LIC Housing Finance based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹940.0, and the most bearish reporting a price target of just ₹410.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹110.4 billion, earnings will come to ₹64.1 billion, and it would be trading on a PE ratio of 7.4x, assuming you use a discount rate of 13.1%.

- Given the current share price of ₹520.35, the analyst price target of ₹594.08 is 12.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on LIC Housing Finance?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.