Key Takeaways

- Growing competition from fintechs and banks, along with slow tech adoption, threatens profitability and customer base due to operational inefficiencies and digital lag.

- Persistent reliance on lower-income segments and rising compliance pressures heighten credit risk and may constrain growth and long-term earnings.

- Strong credit risk management, low funding costs, and favorable housing trends position the company for stable margins, rising earnings, and sustained market growth.

Catalysts

About LIC Housing Finance- A housing finance company, provides loans for the purchase, construction, repair, and renovation of houses/buildings in India.

- LIC Housing Finance faces intense and growing competition from public sector banks and aggressive fintech platforms, which are rapidly gaining market share in prime mortgage lending due to faster rate transmission and digital-first offerings. This will pressure both revenue growth and net interest margins over the medium to long term.

- The company's dependence on traditional branch networks and a slower pace of technology adoption compared to fintech and larger private sector rivals may continue to drive up operating costs and erode cost-to-income ratios, resulting in subdued earnings growth even if disbursements accelerate.

- Prolonged focus on low

- and moderate-income segments without adequate risk diversification exposes the company to higher credit risk, as evidenced by recurring stress in the retail home loan portfolio and rising non-performing assets in adverse cycles, risking future margin compression and higher provisioning requirements.

- Regulatory tightening, including more stringent capital adequacy norms and potential climate-related compliance measures, could constrain lending growth, raise compliance costs, and limit the company's ability to capitalize on formalization and secondary market trends, thereby weighing on long-term revenue potential.

- Demographic shifts, potential urban affordable housing demand stagnation, and shifts in consumer preference toward more flexible or digital housing finance solutions threaten to narrow the addressable market, diminishing top-line growth prospects for traditional lenders such as LIC Housing Finance.

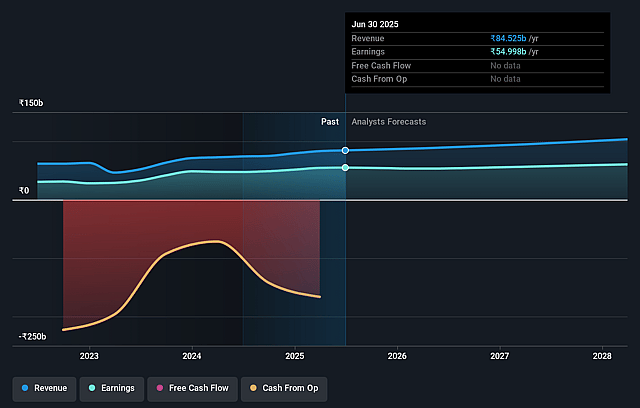

LIC Housing Finance Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on LIC Housing Finance compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming LIC Housing Finance's revenue will grow by 2.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 65.1% today to 59.3% in 3 years time.

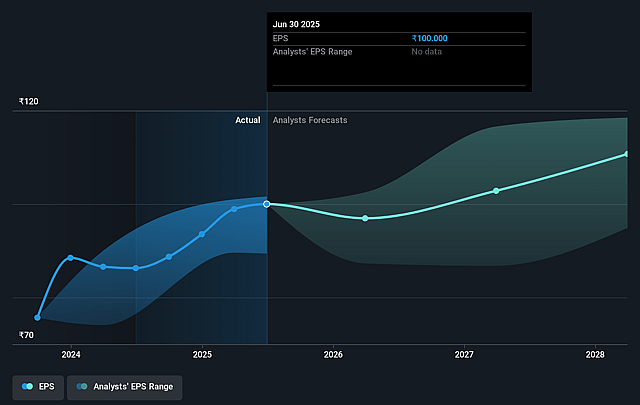

- The bearish analysts expect earnings to reach ₹53.1 billion (and earnings per share of ₹96.31) by about September 2028, down from ₹55.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 7.6x on those 2028 earnings, up from 5.6x today. This future PE is lower than the current PE for the IN Diversified Financial industry at 24.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.33%, as per the Simply Wall St company report.

LIC Housing Finance Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Sustained improvement in asset quality, with Stage 3 exposure default declining from 3.30% to 2.62% year-on-year and a consistent provision coverage ratio around 51%, indicates robust credit risk management which positively impacts net margins and earnings over time.

- The company continues to benefit from a declining cost of funds, with the incremental cost of borrowing falling to 6.97%, supporting stable or improved net interest margins and helping to protect profitability amid competitive loan rates.

- LIC Housing Finance's competitive positioning is aided by access to low-cost funding through its parent, LIC, allowing it to match or beat public sector bank lending rates, which supports revenue and market share resilience.

- Management expects acceleration in disbursement and book growth during the festival and subsequent quarters, targeting a return to double-digit loan growth and increasing revenues and earnings in the medium term.

- Long-term secular trends, including rapid urbanization and government focus on affordable housing, continue to expand the market for organized mortgage lenders like LIC Housing Finance, providing a growth runway that supports sustained improvements in revenues and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for LIC Housing Finance is ₹489.38, which represents two standard deviations below the consensus price target of ₹665.11. This valuation is based on what can be assumed as the expectations of LIC Housing Finance's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹940.0, and the most bearish reporting a price target of just ₹480.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₹89.6 billion, earnings will come to ₹53.1 billion, and it would be trading on a PE ratio of 7.6x, assuming you use a discount rate of 14.3%.

- Given the current share price of ₹560.8, the bearish analyst price target of ₹489.38 is 14.6% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.