Last Update 25 Jun 26

PRTA: Fast Track ATTR Cardio Program And Tau Data Will Support Upside

Analysts kept their fair value estimate for Prothena steady at $21.40 while making only minimal model tweaks, citing broader enthusiasm around tau-targeting Alzheimer's therapies following the CELIA Phase 2 data as a key support for the updated price target framework.

What’s in the News for Prothena

- U.S. FDA granted Fast Track Designation to coramitug, an amyloid depleter antibody in Phase 3 development for treating ATTR cardiomyopathy (ATTR-CM), according to Prothena’s update on the Novo Nordisk partnered program.

- Coramitug is being evaluated by Novo Nordisk in the ongoing Phase 3 CLEOPATTRA trial in approximately 1,280 participants with ATTR-CM. Primary completion is currently expected in 2029, as reported in the company’s program summary.

- Under Novo Nordisk’s acquisition of Prothena’s ATTR amyloidosis business in July 2021, Prothena remains eligible for up to US$1.2b in potential payments tied to clinical and sales milestones, with US$150 million reported as earned so far.

- In a Phase 2 trial conducted by Novo Nordisk, coramitug 60 mg/kg was reported to reduce and improve NT-proBNP from baseline and was associated with improvements in several echocardiographic measures in ATTR-CM patients already receiving standard of care, while being described as well tolerated.

- Prothena reported that from February 27, 2026 to March 31, 2026, the company repurchased 788,990 shares, representing 1.47% of its shares, for US$7.3 million, completing the buyback program announced on February 27, 2026.

Valuation Changes for Prothena

- Fair Value: The fair value estimate for Prothena is unchanged at $21.40 per share, indicating no shift in the overall valuation anchor.

- Discount Rate: The discount rate has risen slightly from 7.58% to 7.64%, which modestly increases the required return applied to Prothena’s projected cash flows.

- Revenue Growth: The long term revenue growth assumption is effectively unchanged at 20.30%, reflecting a stable outlook in the current model.

- Net Profit Margin: The projected net profit margin remains stable at 8.32%, suggesting no material change in expected profitability assumptions.

- Future P/E: The future P/E multiple has edged up slightly from 152.39x to 152.66x, indicating a small adjustment in how much investors are modeled as willing to pay for Prothena’s future earnings.

Key Takeaways

- Successful clinical trials for Birtamimab and Alzheimer's treatments could significantly boost Prothena's revenue through large market opportunities.

- Strategic partnerships and a strong financial position support pipeline advancement and potential long-term earnings growth.

- Uncertainty in FDA approval and potential competition may delay birtamimab commercialization and impact Prothena's financial resources and revenue growth prospects.

Catalysts

About Prothena- A late-stage clinical biotechnology company, focuses on discovery and development of novel therapies to treat diseases caused by protein dysregulation in the United States.

- Prothena's wholly-owned drug candidate, Birtamimab, is nearing a significant inflection point with expected top-line results from the Phase III AFFIRM-AL trial in mid-2025. If successful, it could lead to a substantial revenue boost upon its potential U.S. launch in the second half of 2026 due to its large multi-billion dollar market opportunity for treating Mayo Stage IV AL amyloidosis patients.

- The potential first-in-class treatment for Alzheimer's disease, PRX012, might offer a unique once-monthly subcutaneous administration, reducing treatment burden and potentially gaining market share upon effective Phase I trial results in 2025. This innovation could lead to substantial revenue increases given the large, underserved Alzheimer's market.

- Prothena's second Alzheimer's program, PRX123, a dual A-beta and tau vaccine, has the potential of targeting the large presymptomatic segment of the Alzheimer's market, potentially accelerating future revenue growth if it progresses successfully through clinical stages.

- Strategic partnerships with major pharmaceutical companies, including BMS and Roche, leverage resources and expertise to advance Prothena's pipeline, potentially increasing long-term earnings through shared profits from partnered programs' successes, particularly in diseases like Parkinson's and ATTR amyloidosis.

- Prothena's solid financial position, with $472.2 million in cash and no debt as of 2024, provides a strong foundation for advancing its clinical trials and supporting future earnings growth through successful product launches and commercialization efforts.

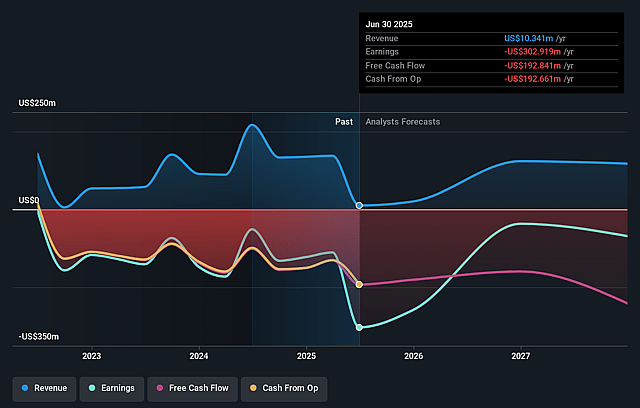

Prothena Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Prothena's revenue will grow by 20.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -260.9% today to 8.3% in 3 years time.

- Analysts expect earnings to reach $8.4 million (and earnings per share of $0.08) by about June 2029, up from -$151.2 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $76.8 million in earnings, and the most bearish expecting $-98.5 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 153.2x on those 2029 earnings, up from -3.3x today. This future PE is greater than the current PE for the US Biotechs industry at 16.8x.

- Analysts expect the number of shares outstanding to decline by 2.74% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.64%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Uncertainty around FDA approval for birtamimab, particularly if Phase III AFFIRM-AL results do not meet predefined statistical significance, could delay commercialization and impact Prothena's future revenue projections.

- Potential competition in the treatment of AL amyloidosis from other emerging therapies, like daratumumab, might limit birtamimab’s market share, affecting anticipated revenue growth.

- Relatively high clinical development costs and net losses projected for 2025 could strain financial resources before birtamimab or other therapies can generate significant earnings.

- The lack of demonstrated early mortality impact by existing plasma cell-targeting therapies like daratumumab sets a high bar for proving the market need and commercial viability of birtamimab, potentially impacting its uptake and, subsequently, net margins.

- Dependence on successful partnerships with large pharmaceutical companies and the outcome of clinical trials involving partnered products, such as prasinezumab and coramitug, introduces execution and collaboration risks that could influence long-term earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $21.4 for Prothena based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $36.0, and the most bearish reporting a price target of just $8.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $100.9 million, earnings will come to $8.4 million, and it would be trading on a PE ratio of 153.2x, assuming you use a discount rate of 7.6%.

- Given the current share price of $9.4, the analyst price target of $21.4 is 56.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Prothena?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.