Last Update 25 Mar 26

Fair value Decreased 0.75%NEOGEN: Raised Guidance And Cost Actions Will Support Higher Future Earnings Quality

Narrative Update Overview

The revised analyst price target for Neogen Chemicals edges slightly lower to ₹1,756.25 from ₹1,769.57. This reflects updated assumptions around the discount rate, revenue growth, profit margin, and future P/E, while staying broadly aligned with recent Street research that has cited better revenue and EBITDA prints, higher guidance, and early benefits from cost actions.

Analyst Commentary

Recent Street updates around Neogen Chemicals and its global peer Neogen point to a mixed but generally constructive backdrop, with positive reactions to recent earnings, higher guidance, and the early impact of cost actions, balanced against measured expectations for how durable these trends may be.

Bullish Takeaways

- Bullish analysts highlight that Neogen delivered revenue and EBITDA outcomes that were ahead of their expectations, which they view as supportive of current valuation assumptions tied to operating execution.

- The decision to raise guidance is seen by bullish analysts as a sign of management confidence in the earnings trajectory, which they factor into higher modeled earnings power and, in turn, higher price targets.

- Cost actions are described as clearly starting to take hold, and bullish analysts see this as an important driver for margin resilience and potential upside to profitability assumptions if efficiencies sustain.

- Recent price target increases, such as to US$10 and US$12 for Neogen, indicate that bullish analysts are willing to underwrite stronger execution and earnings delivery, even while many still maintain balanced ratings such as Neutral.

Bearish Takeaways

- Bearish analysts, or more cautious voices, stress that one quarter does not make a trend, so they are reluctant to extrapolate the latest revenue and EBITDA beat into long term growth assumptions without further proof of consistency.

- The retention of more neutral ratings alongside higher price targets suggests some concern that a portion of the good news around guidance and cost actions may already be reflected in current prices.

- Cautious analysts flag execution risk around sustaining cost benefits and operational improvements, which, if they fade, could challenge margin expectations and justify more conservative valuation multiples.

- There is an implicit caution that higher guidance raises the bar for future quarters, which could introduce downside risk to sentiment if subsequent results do not align with these updated expectations.

What's in the News

- The board approved a preferential private placement of 1,000,000 equity shares at ₹1,610 per share, with gross proceeds of ₹1,610,000,000 and participation from new investor Cadamba Solutions Private Limited, subject to shareholder and regulatory approvals including SEBI and stock exchange clearances (Key Developments).

- Post issue, Cadamba Solutions Private Limited is expected to hold 1,000,000 equity shares, representing 3.65% ownership, with the issue price set 17.02% above the SEBI floor price of ₹1,375.82 and subject to lock in periods of 18 months for up to 20% of total capital and six months for any excess as per SEBI ICDR Regulations (Key Developments).

- The board meeting on March 7, 2026 considered and approved the proposal to raise funds via equity issuance through one or more tranches by preferential issue and approved convening an Extraordinary General Meeting along with a record or cutoff date of March 20, 2026 for e voting eligibility (Key Developments).

- An Extraordinary General Meeting is scheduled for March 29, 2026 at 11:30 Indian Standard Time for shareholder approval related to the preferential issue and associated matters (Key Developments).

- An earlier board meeting on February 11, 2026 reviewed unaudited standalone and consolidated financial results for the quarter and nine months ended December 31, 2025 and considered broader fund raising options including equity shares, various instruments and warrants through public issue, qualified institutional placement, preferential issue or private placement in one or more tranches (Key Developments).

Valuation Changes

- Fair Value: Revised slightly lower to ₹1,756.25 from ₹1,769.57, indicating a modest reset in the central valuation estimate.

- Discount Rate: Trimmed marginally to 13.84% from 13.94%, reflecting a small adjustment to the required rate of return used in the model.

- Revenue Growth: Kept broadly similar at 48.63% from 48.69%, signaling very limited change to top line growth assumptions in ₹ terms.

- Net Profit Margin: Edged up to 6.57% from 6.54%, implying a slightly stronger earnings conversion assumption on future ₹ revenue.

- Future P/E: Lowered modestly to 38.14x from 38.67x, pointing to a small reset in the multiple applied to expected earnings.

Key Takeaways

- Expansion into lithium-ion battery materials and global supply diversification is driving strong growth opportunities in electric vehicle and renewable energy storage sectors.

- Strategic partnerships and rising custom manufacturing demand are enhancing technological capabilities, supporting sustainable margins and resilient earnings.

- Delays in approvals, erratic lithium demand, concentrated product risk, and rising sustainability requirements threaten revenue growth, margin stability, and long-term financial health.

Catalysts

About Neogen Chemicals- Engages in the manufacture and sale of specialty chemicals in India.

- Neogen is accelerating its entry into lithium-ion battery materials, with large-scale capacity expansions for lithium salts and electrolytes coming online. This positions the company to capture outsized growth driven by the surging electric vehicle and renewable energy storage sectors, directly contributing to long-term revenue and earnings growth.

- Global customers are increasingly seeking non-China supply chains for battery chemicals due to stricter localization requirements and new subsidy frameworks in the U.S. and Europe. As one of the very few qualified non-Chinese suppliers, Neogen is attracting interest from global battery and EV makers-potentially enabling robust export-led revenue growth and higher-margin international contracts.

- Strong demand visibility is emerging from both EV battery and stationary energy storage markets, with Indian giga-factories (Ola, Exide, Reliance, Tata, etc.) commencing production between 2025–2027 and solar energy storage sharply picking up. This underpins a multi-year volume ramp-up, providing a structural tailwind to Neogen's advanced chemical segment revenues and asset utilization.

- Strategic technology partnerships (such as the JV with Morita of Japan) are deepening Neogen's technological moat, enabling backward integration, improved efficiencies, and access to proven production know-how. This should support sustainable margin expansion and enhanced return on capital over the medium

- to long-term.

- Secular China Plus One dynamics and stricter environmental compliance requirements globally are prompting pharma, agrochemical, and advanced industrial customers to diversify supply-driving rising recurring business for Neogen's custom synthesis and contract manufacturing business, which stabilizes earnings and increases gross margin resilience.

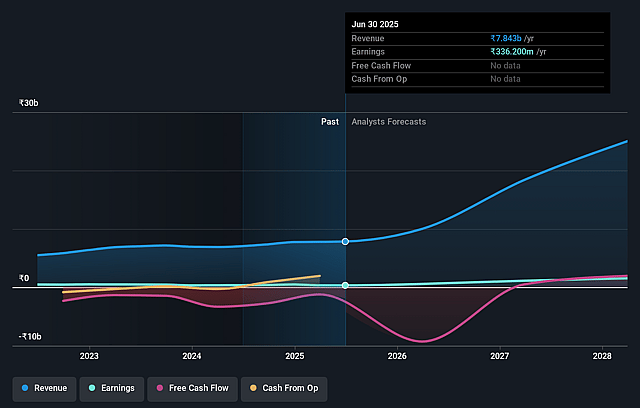

Neogen Chemicals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Neogen Chemicals's revenue will grow by 48.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.4% today to 6.6% in 3 years time.

- Analysts expect earnings to reach ₹1.8 billion (and earnings per share of ₹76.62) by about March 2029, up from ₹197.4 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹2.6 billion in earnings, and the most bearish expecting ₹1.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 38.6x on those 2029 earnings, down from 172.7x today. This future PE is greater than the current PE for the IN Chemicals industry at 20.0x.

- Analysts expect the number of shares outstanding to decline by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.84%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Delays in customer product approvals and plant audits, particularly from major international clients, have slowed the ramp-up of export revenues in battery chemicals (notably lithium salts and electrolytes), risking underutilization of expanded capacity and potentially impacting both revenue growth and EBITDA in the near-to-medium term.

- Ongoing softness in lithium chemical demand and price volatility-exacerbated by global tariff and subsidy uncertainties, especially in the US-may result in erratic sales and margin pressures, with significant risk to revenue and net margins if Neogen cannot consistently pass through input cost increases.

- The company's substantial capital expenditure programs (₹1,500+ crore) are being financed in part by insurance proceeds and new debt issuances, creating execution risk if project timelines slip or there are further delays in insurance receipts, which could increase interest costs and strain free cash flow and net earnings.

- Heavy reliance on a limited product set-mainly bromine and lithium-based compounds-exposes Neogen to concentration risk; any cyclical downturn or increased competition in these segments (including from larger global or low-cost Chinese players) can directly hurt revenue and compress margins.

- Intensifying global movement towards greener and more sustainable (biobased or next-gen) chemicals, together with rising regulatory scrutiny and environmental compliance costs in India, could erode demand for traditional specialty chemicals, drive up operating expenses, and threaten Neogen's long-term profitability and investor appeal.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹1756.25 for Neogen Chemicals based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹2761.0, and the most bearish reporting a price target of just ₹1335.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹26.9 billion, earnings will come to ₹1.8 billion, and it would be trading on a PE ratio of 38.6x, assuming you use a discount rate of 13.8%.

- Given the current share price of ₹1201.4, the analyst price target of ₹1756.25 is 31.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Neogen Chemicals?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.