Last Update 22 Mar 26

SDY: Stable Outlook For Margins And New CFO Will Support Re Rating

Analysts have reset their price target on Speedy Hire to £0.55, reflecting updated assumptions on discount rate, revenue growth, profit margin and future P/E. These assumptions broadly align with prior estimates while fine tuning the valuation framework.

What's in the News

- Speedy Hire appointed Judith Cottrell to the Board as Chief Financial Officer, effective July 1, 2026, following an external selection process that concluded earlier than initially expected (Key Developments).

- Current Chief Financial Officer Paul Rayner plans to retire from his executive role by the end of 2026 and will step down from the Board and as CFO on July 1, 2026, after delivering the results to March 31, 2026 (Key Developments).

- Paul Rayner will remain with Speedy Hire after July 1, 2026 to support a handover and assist with ongoing initiatives, indicating a phased transition rather than an abrupt change (Key Developments).

- Incoming CFO Judith Cottrell brings experience from previous senior financial and operational positions, including Chief Financial Officer of Ricardo Plc and Group Finance Director at RPS Group Plc, and is a member of the Institute of Chartered Accountants in England and Wales (Key Developments).

Valuation Changes

- Fair Value: Modelled fair value remains effectively unchanged at £0.55 per share.

- Discount Rate: The discount rate is stable at around 13.21%, indicating no material adjustment to the risk assumption.

- Revenue Growth: Forecast revenue growth remains steady at about 9.88%.

- Net Profit Margin: The expected net profit margin is broadly unchanged at roughly 9.46%.

- Future P/E: The assumed future P/E multiple is consistent at about 6.99x.

Key Takeaways

- Investment in eco-friendly solutions and hydrogen partnerships positions Speedy Hire for sustainable growth amid increased demand for reduced emissions.

- Enhancements in logistics, service centers, and infrastructure contracts are set to boost operational efficiency, revenue, and strengthen market position.

- Increased debt and rising expenses without revenue growth could stress financial health, while competitive market conditions may hinder earnings stability and future growth.

Catalysts

About Speedy Hire- Provides tools and equipment hire, and services to the construction, infrastructure, and industrial markets in the United Kingdom and Ireland.

- The implementation of the second year of the Velocity strategy, including digital transformation and system upgrades like CRM and order management systems, is expected to optimize operations, improve customer services, and increase revenue.

- The ongoing investment in carbon eco-friendly hire fleet and partnerships in renewable energy sectors, such as the collaboration with AFC Energy on hydrogen solutions, positions Speedy Hire for future growth and sustainability, potentially enhancing net margins as customers focus on reducing emissions.

- The expansion and optimization of logistics and service centers, including the centralization of stock and data-driven route planning, are anticipated to improve operational efficiency and reduce costs, positively impacting net margins and EBITDA.

- Continued growth in the Lloyds British test, inspection, and certification business, along with new opportunities in infrastructure projects like rail and energy sectors, are expected to drive revenue growth.

- The successful execution and early mobilization of the Amey contract, along with potential new contract wins in infrastructure and energy sectors, are expected to augment revenue and strengthen market position, supporting earnings growth.

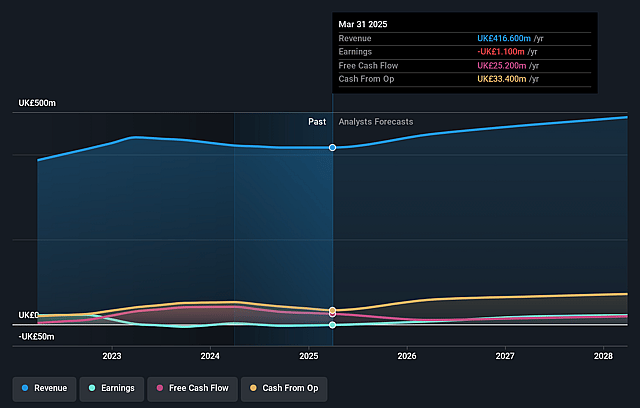

Speedy Hire Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Speedy Hire's revenue will grow by 9.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from -2.8% today to 9.5% in 3 years time.

- Analysts expect earnings to reach £52.5 million (and earnings per share of £0.06) by about March 2029, up from -£11.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting £71.8 million in earnings, and the most bearish expecting £44.1 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 7.0x on those 2029 earnings, up from -8.0x today. This future PE is lower than the current PE for the GB Trade Distributors industry at 15.3x.

- Analysts expect the number of shares outstanding to grow by 0.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.21%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The slight decrease in revenue could be a concern as it may imply difficulties in maintaining sales levels, which could impact overall earnings and profit margins.

- The reported increase in net debt, partly due to the acquisition of Green Power Hire, might create financial stress if revenues do not grow as expected to offset the debt, impacting net margins.

- The challenging and competitive market conditions, particularly in the non-residential or commercial construction space, could hinder revenue growth and pose a risk to future earnings.

- Fluctuations in the joint venture earnings, especially in a sector like oil and gas which is noted for its volatility, could unpredictably affect net income, impacting the stability of earnings.

- Increases in payroll and overhead costs without corresponding increases in revenue could lead to tighter net margins and reduced profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £0.55 for Speedy Hire based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £0.79, and the most bearish reporting a price target of just £0.36.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £554.8 million, earnings will come to £52.5 million, and it would be trading on a PE ratio of 7.0x, assuming you use a discount rate of 13.2%.

- Given the current share price of £0.2, the analyst price target of £0.55 is 63.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Speedy Hire?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.