Last Update 06 Jun 26

Fair value Increased 3.91%IBE: Neutral Outlook As Data Center Power Demand And Storage Projects Shape Returns

The analyst fair value estimate for Iberdrola has shifted from €19.17 to €19.92, as analysts highlight data center driven demand and supply tailwinds, which are reflected in recent price target increases from several firms.

Analyst Commentary

Analysts are split, with some pointing to upside tied to data center exposure and others sounding more cautious on where the stock trades relative to their expectations.

Bullish Takeaways

- Bullish analysts see Iberdrola as well placed to capture data center driven electricity demand, which they view as supportive for earnings forecasts and, in turn, higher valuation ranges.

- The recent move from a neutral to a more positive rating by one large brokerage, paired with a lift in its price target from €16.90 to €22.60, is cited as a sign of growing confidence in the company’s ability to execute on growth projects.

- Price target increases from several firms, including a €0.80 step up at JPMorgan and other upward adjustments, indicate that updated models are incorporating what these analysts see as a more supportive supply backdrop for Iberdrola’s generation and networks portfolio.

- Supportive research commentary presents the stock as a potential beneficiary if data center demand continues to function as a structural driver for power consumption in key markets where Iberdrola operates.

Bearish Takeaways

- Bearish analysts have recently shifted to a more cautious stance, as reflected in at least one downgrade, citing concerns that Iberdrola’s current share price may already reflect much of the data center growth narrative.

- The downgrade highlights some hesitation around the risk and reward trade off, with questions about whether execution on large projects can fully match the more optimistic assumptions used by bullish analysts.

- More cautious research views emphasize that, if earnings or project delivery were to fall short of the higher expectations implied by raised targets, there could be pressure on Iberdrola’s valuation multiples.

- This split in opinion leaves investors weighing upside tied to data center and supply tailwinds against the risk that the share price is already aligned with, or ahead of, some analysts’ fair value estimates.

What's in the News

- Barclays has named Iberdrola as one of its top picks in European utilities, maintaining an Overweight rating and setting a price target of €22.60 per share, according to recent broker research.

- Iberdrola has started up Spain's largest battery energy storage system at the Campo Arañuelo solar complex in Cáceres, with 58 MW of power and 120 MWh of storage capacity, and now operates around 200 MW of battery storage in Spain, based on company announcements.

- Through its subsidiary Avangrid, Iberdrola is set to supply electricity to Microsoft from the Bluebird Solar project in Klickitat County, Washington, with commercial operation expected in 2028 and construction projected to create about 300 jobs and around $11 million in local property tax contributions, according to project disclosures.

- Iberdrola's board meeting on 17 March 2026 includes an agenda item to appoint Marina Freitas Gonçalves de Araújo Grossi as an independent director and to designate her as a member of the Audit and Risk Supervision Committee and the Sustainable Development Committee, based on company governance filings.

Valuation Changes

- Fair Value: The updated analyst fair value estimate has risen slightly from €19.17 to €19.92 per share.

- Discount Rate: The assumed discount rate has moved up modestly from 7.17% to 7.32%, indicating a slightly higher required return in the model.

- € Revenue Growth: The forecast annual € revenue growth assumption has been trimmed from 4.86% to 4.00%.

- € Net Profit Margin: The projected € net profit margin has edged higher from 14.68% to 15.74%.

- Future P/E: The implied future P/E multiple has increased from 23.49x to 24.96x in the updated assumptions.

Key Takeaways

- Expansion of regulated network assets and clean energy projects, backed by supportive policies, drives predictable revenue growth and higher margins.

- Strong financing and operational cash flow support ambitious investments, maintaining reliable dividends and reducing the need for new equity.

- Heavy reliance on regulated markets, partnership funding, and favorable regulation exposes Iberdrola to political, financial, and execution risks that threaten profitability and growth targets.

Catalysts

About Iberdrola- Engages in the generation, production, transmission, distribution, and supply of electricity in Spain, the United Kingdom, the United States, Mexico, Brazil, Germany, France, and Australia.

- Major expansion of regulated network investments in the US and UK, supported by stable and attractive policy frameworks and recently approved regulatory determinations, is expected to nearly triple Iberdrola's regulated asset base to €90bn by 2031. This should drive sustained, predictable growth in revenues and a structural increase in regulated net margins.

- Ongoing acceleration of grid modernization and digitalization-driven by enhanced incentives in the new regulatory regimes-will improve operational efficiency, reduce network losses, and boost EBITDA margins over time as these investments scale across core regions.

- A multi-year pipeline of large offshore wind and renewable projects in the US, UK, and continental Europe, backed by supportive government policies and long-term power purchase agreements, underpins forward-looking growth in clean generation capacity and future revenues.

- The electrification of transport, heating, and industrial sectors in both Europe and the US is expected to steadily raise electricity demand over the next decade, expanding Iberdrola's addressable market and enhancing long-term top-line and EBITDA growth prospects.

- Growing access to green finance, along with robust operational cash flow and a successful equity raise, ensures Iberdrola can fund its ambitious expansion with comfortable leverage and no need for additional equity until at least 2030, supporting sustained investment, future earnings growth, and reliability of dividend policies.

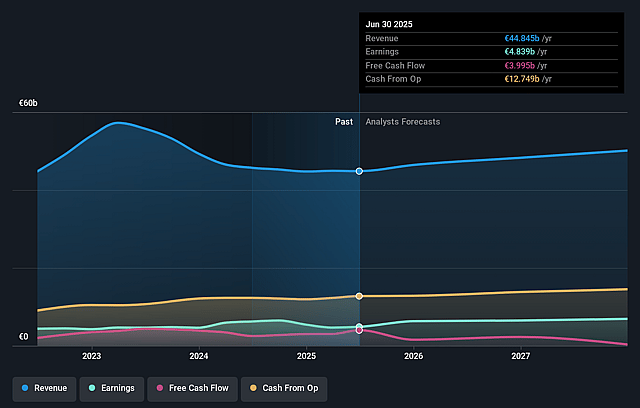

Iberdrola Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Iberdrola's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.6% today to 15.7% in 3 years time.

- Analysts expect earnings to reach €7.7 billion (and earnings per share of €1.16) by about June 2029, up from €5.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 25.0x on those 2029 earnings, up from 24.1x today. This future PE is greater than the current PE for the GB Electric Utilities industry at 16.6x.

- Analysts expect the number of shares outstanding to grow by 4.93% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.32%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Iberdrola's significant reliance on regulated markets-particularly in the U.K. and the U.S., which will account for approximately 75% of the regulated asset base by 2031-increases exposure to potential adverse changes in regulatory frameworks or political intervention, which could negatively impact allowed returns, pricing power, and future net margins.

- The company is undertaking a large €5 billion equity raise to fund an unprecedented acceleration in network investments, indicating heavy dependence on favorable capital market conditions and access to green financing; should macroeconomic conditions shift (e.g., rising interest rates or tighter credit), Iberdrola may face higher financing costs, pressuring future profitability and earnings growth.

- While Iberdrola's focus shifts to networks, growth in renewables investment is largely being maintained only through asset rotation and co-investment strategies; heavy reliance on these partnership and asset sale mechanisms to fund growth could expose the company to execution risk, dilution of returns, or subdued revenue growth if market appetite weakens or partners become scarce.

- Spanish regulatory uncertainty, as highlighted by ongoing concerns regarding investment caps, slow recognition of investment, and unfavorable draft proposals for network remuneration, suggests downside risks for Iberdrola's domestic regulated business, with potential impacts on revenue growth, cost recovery, and regional net margins.

- The group's rapidly expanding asset base and leverage (despite improved ratios post-asset rotation) could become a long-term financial risk if regulatory returns fail to keep pace with cost inflation, future rate hikes, or if investments face delays and overruns-collectively jeopardizing targets for EBITDA growth, net profit, and dividend sustainability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €19.92 for Iberdrola based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €22.6, and the most bearish reporting a price target of just €17.3.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €48.9 billion, earnings will come to €7.7 billion, and it would be trading on a PE ratio of 25.0x, assuming you use a discount rate of 7.3%.

- Given the current share price of €19.85, the analyst price target of €19.92 is 0.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Iberdrola?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.