Last Update 10 Jul 26

Fair value Increased 16%IBE: Data Center Power Demand And Grid Resilience Will Drive Future Upside

The analyst fair value estimate for Iberdrola has been raised from €20.50 to €23.80, reflecting higher price targets around €21 to €22.60 and analyst views that the company can support its premium valuation with earnings growth tied to electricity demand and data center related tailwinds.

Analyst Commentary

Recent research on Iberdrola points to a cluster of higher price targets and rating upgrades, with several bullish analysts highlighting earnings execution and exposure to growing electricity demand as key supports for the current valuation premium.

Price targets in the low €20s are a common reference point, with one large bank moving from €16.90 to €22.60 and others setting targets around €21 to €22. This range helps frame where bullish analysts see Iberdrola trading if the company continues to deliver on its growth plans and maintains its earnings profile.

Rating changes also reflect this more positive stance. Iberdrola has recently seen upgrades to more favorable ratings such as Overweight and Buy, alongside Neutral views that still acknowledge its premium pricing versus the STOXX Europe 600 Utilities Index. For investors, the mix of views underscores both the perceived quality of the business and the execution risk that comes with a premium valuation.

Bullish analysts often tie their optimism to Iberdrola's exposure to rising electricity demand in the U.S. and the UK and to data center related demand, which they see as supportive for earnings. These themes sit at the core of the argument that the stock can justify trading above the broader utilities benchmark, provided the company continues to deliver consistent results.

Bullish Takeaways

- Higher price targets in the €21 to €22.60 range signal that bullish analysts see room for Iberdrola's valuation to be supported if earnings execution stays on track.

- Upgrades to more positive ratings, including Overweight and Buy, reflect confidence in Iberdrola's ability to capitalize on its current project pipeline and demand trends.

- Exposure to rising electricity demand in the U.S. and the UK is viewed as a key growth driver that can help sustain Iberdrola's premium versus the STOXX Europe 600 Utilities Index.

- Analysts highlighting Iberdrola's link to data center demand and supply tailwinds see this as an additional catalyst for earnings strength and support for the current premium valuation.

What’s in the News for Iberdrola

- Iberdrola selected ICEYE to run a 12 month innovation project in Spain that uses near real time geospatial data to strengthen its electricity grid against extreme natural events, with rapid wind damage assessment also planned for assets in the United States and Australia (source: ICEYE project announcement).

- The ICEYE collaboration is designed to help Iberdrola anticipate risks, quickly assess infrastructure damage and reduce potential supply disruptions during severe weather events (source: ICEYE project summary).

- Iberdrola opened the 243MW Fénix photovoltaic plant in Sicily, Italy, a solar facility sized to supply electricity annually to more than 140,000 households and support Italy’s clean energy transition (source: Fénix PV plant news).

- Most of the Fénix plant’s output is allocated through long term power purchase agreements with multiple Italian companies, which are intended to provide more stable energy costs and support supply security (source: Fénix PV plant news).

- Iberdrola has a stock split or significant stock dividend planned with a 1 to 2.89126 ratio dated Jul 6, 2026, categorized as a Stock Split & Significant Stock Dividend event (source: Key Developments).

Valuation Changes for Iberdrola

- Fair Value: Raised from €20.50 to €23.80, indicating a higher central estimate of what Iberdrola's stock may be worth based on current assumptions.

- Discount Rate: Adjusted from 7.646% to 7.324%, reflecting a slightly lower rate used to bring future cash flows back to today.

- Revenue Growth: Assumption revised from 13.63% to 7.95%, pointing to a more moderate expected pace of future euro revenue expansion.

- Net Profit Margin: Updated from 11.66% to 14.98%, indicating a higher assumed share of earnings retained from each euro of revenue.

- Future P/E: Tweaked from 28.43x to 28.01x, showing a marginally lower multiple applied to Iberdrola's expected earnings.

Catalysts

About Iberdrola

Iberdrola is a global electricity company focused on regulated networks, renewable power generation and customer supply across Europe and the Americas.

What are the underlying business or industry changes driving this perspective?

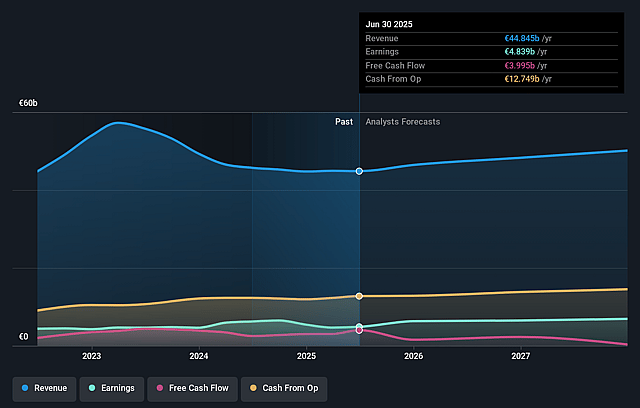

- Large scale investment in regulated networks, with €9b invested in the first 9 months of 2025 and a regulated asset base of about €49.3b, positions Iberdrola to grow allowed revenues and potentially support earnings from a larger, inflation linked asset base.

- Expansion of the offshore wind portfolio, including East Anglia THREE and TWO in the U.K., Vineyard Wind 1 in the U.S. and Windanker in Germany, along with 5,500 megawatts under construction, provides visibility on additional generation capacity that can contribute to revenue and EBITDA once fully commissioned.

- Supportive regulatory moves in key markets, such as higher tariffs in New York and Maine, rate updates in Brazil and evolving RIIO frameworks in the U.K., create a backdrop where allowed returns can help sustain EBITDA and support cash flow visibility.

- Partnership and asset rotation activity, with about €8b of transactions signed and co investment commitments with Norges Bank, Kansai and Masdar, can recycle capital into higher priority projects, potentially improving returns on invested capital and supporting net profit.

- Growing demand for clean electricity from data centers and electrification, supported by more than 12 terawatt hours a year of PPAs with technology companies and a strong U.S. and European pipeline, can support long term contracted volumes and contribute to revenue and cash flow stability.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Iberdrola compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Iberdrola's revenue will grow by 7.9% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 12.6% today to 15.0% in 3 years time.

- The bullish analysts expect earnings to reach €8.2 billion (and earnings per share of €1.23) by about July 2029, up from €5.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 28.0x on those 2029 earnings, up from 25.6x today. This future PE is greater than the current PE for the GB Electric Utilities industry at 17.2x.

- The bullish analysts expect the number of shares outstanding to grow by 4.93% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.32%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- A large share of Iberdrola's earnings is tied to regulated Networks, and future regulatory reviews in key markets like Spain and the U.K. could result in lower allowed returns or tighter remuneration. This would directly cap growth in the regulated asset base and put pressure on revenue and net profit over time.

- The Iberia blackout and the shift to more synchronous generation are already increasing ancillary service costs. If system operators continue to require more stability services as renewables grow, Iberdrola may keep absorbing part of these costs on multi year contracts, which would drag on margins and EBITDA longer than expected.

- The company is committing large amounts of capital to long lead offshore and onshore projects, with around 5,500 megawatts under construction and a sizeable pipeline. Any delays, cost overruns, auction outcomes that do not clear at acceptable prices, or weaker PPA terms could reduce the returns on this invested capital and weigh on earnings and cash flow.

- The plan relies heavily on continued tariff uplift and supportive frameworks in the U.S. and Brazil. Slower or less favorable rate case outcomes, or currency weakness in markets such as Brazil, could erode the contribution from these regions and limit growth in revenue and net profit reported in euros.

- Iberdrola is using asset rotations, partnerships and equity issuance to fund record investment while managing around €48.5b of net debt. If future asset sales or partnerships are less attractive, or if funding costs rise faster than expected, the group may face pressure on free cash flow, interest expenses and ultimately earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Iberdrola is €23.8, which represents up to two standard deviations above the consensus price target of €20.39. This valuation is based on what can be assumed as the expectations of Iberdrola's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €23.8, and the most bearish reporting a price target of just €17.3.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be €54.7 billion, earnings will come to €8.2 billion, and it would be trading on a PE ratio of 28.0x, assuming you use a discount rate of 7.3%.

- Given the current share price of €21.06, the analyst price target of €23.8 is 11.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Iberdrola?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.