Last Update 26 Jun 26

Fair value Increased 40%IBE: Premium To Peers Will Face Test From Data Center Demand

The updated analyst price target for Iberdrola has shifted from €12.36 to €17.30, with analysts citing the company’s exposure to rising electricity demand in the U.S. and UK, as well as expectations for relatively stronger earnings supported by data center related demand and sector tailwinds.

Analyst Commentary

Recent research on Iberdrola highlights a mix of optimism around demand for electricity in the U.S. and UK and caution around how much of that story is already reflected in the share price. Several firms have updated ratings and price targets, giving investors more detail on how they view Iberdrola’s growth profile and valuation trade off.

One group of analysts flags that Iberdrola trades at a near 30% premium to the STOXX Europe 600 Utilities Index. In their view, this premium leaves less room for error and depends heavily on the company consistently delivering earnings growth over time. Any shortfall in execution, project delivery, or returns on new investments could put that premium under pressure.

On the more positive side, some research points to Iberdrola’s exposure to rising electricity demand, especially linked to data centers and related infrastructure. These analysts argue that stronger demand and sector tailwinds support higher price targets in the low €20s, with one setting a target of €21.10 and another at €22.60. They frame Iberdrola as relatively well positioned within European utilities for data center related load growth.

Upgrades in recent months, including moves to more positive ratings and increased targets, also reflect confidence in Iberdrola’s earnings outlook tied to these demand trends. At the same time, changes in stance over time, including earlier downgrades and trimmed targets, show that sentiment has not been one way and that analysts have adjusted their views as conditions and expectations shifted.

Bearish Takeaways

- Bearish analysts point out that Iberdrola’s near 30% premium to the STOXX Europe 600 Utilities Index increases the risk that any miss on earnings delivery or project execution could lead to valuation pressure.

- The reliance on consistent earnings growth to justify that premium creates a tighter margin for error, especially if demand linked to data centers or other projects does not materialise as expected.

- Past bearish adjustments, including downgrades and more cautious target changes, underline concern that Iberdrola’s growth story might be fully or largely priced in, leaving less upside if growth turns out to be only in line with peers.

- Some cautious views also highlight execution risk around large investment programs, where cost overruns, delays, or regulatory changes could affect the earnings trajectory that current price targets assume.

What’s in the News for Iberdrola

- Iberdrola plans to invest nearly US$5b in Brazil's northeastern state of Bahia by 2030 through its subsidiary Neoenergia Coelba, according to recent reports.

- The Bahia plan includes 54 new substations, over 2,000 kilometers of high voltage transmission lines, and 42,000 kilometers of medium voltage distribution networks.

- Iberdrola's Brazilian subsidiary intends to invest a total of 50 billion reais in network infrastructure across Brazil following the recent renewal of its distribution concessions, as reported in the same source.

Valuation Changes for Iberdrola

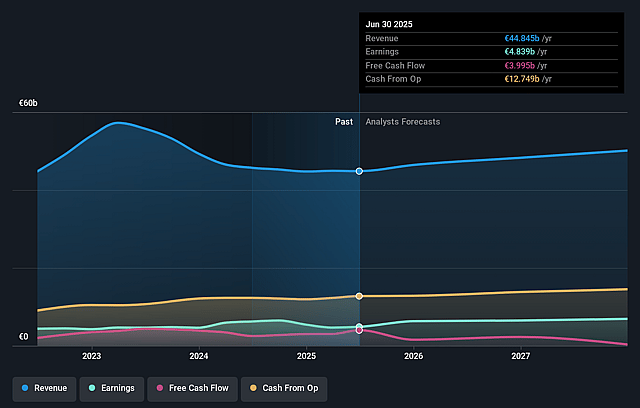

- Fair Value: updated from €12.36 to €17.30, a rise of roughly 40%, indicating higher assessed upside in the Iberdrola stock based on the latest assumptions.

- Discount Rate: adjusted slightly lower from 7.65% to 7.32%, which increases the present value of projected future cash flows in the Iberdrola model.

- Revenue Growth: shifted from an assumed increase of about 1.47% to an assumed decline of about 0.60%, implying a more cautious view on future € revenue expansion.

- Net Profit Margin: moved from 15.29% to 17.83%, indicating a higher expected share of € earnings retained from each euro of revenue.

- Future P/E: updated from 18.36x to 21.91x, reflecting a higher implied valuation multiple for Iberdrola on expected earnings.

Catalysts

About Iberdrola

Iberdrola is a global utility focused on regulated electricity networks and large scale renewable generation, including onshore and offshore wind, hydro and storage.

What are the underlying business or industry changes driving this perspective?

- Accelerating grid investment needs in the U.S., U.K. and Brazil risk colliding with tighter regulatory returns and draft determinations that may not fully remunerate higher capex and operating complexity. This would compress returns on the growing regulated asset base and slow net profit growth.

- Heavy capital allocation to offshore wind projects under construction in the U.K., U.S., Germany and France exposes Iberdrola to potential delays, cost overruns and auction budget constraints. These factors could erode project economics and weigh on future EBITDA and earnings despite the current build out momentum.

- Rapid electrification from data centers and new industrial demand in the U.S. could outpace timely network upgrades and renewable additions, leading to congestion, curtailment and reliance on higher cost generation. This would pressure margins in both Networks and Renewables rather than delivering the smooth revenue uplift implied by current valuations.

- Growing dependence on asset rotation, partnerships and capital increases to fund a record multi year capex plan heightens execution and refinancing risk. Any slowdown in disposals or partner appetite would force higher leverage or reduced investments, constraining future cash flow growth and dividend expansion.

- Rising system stability requirements and ancillary service costs in Iberia following recent blackouts highlight structural challenges of integrating variable renewables at scale. If cost pass throughs lag contractual commitments, this could structurally drag on net margins in the Renewables and Customers business even as volumes grow.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Iberdrola compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Iberdrola's revenue will remain fairly flat over the next 3 years.

- The bearish analysts assume that profit margins will increase from 12.6% today to 17.8% in 3 years time.

- The bearish analysts expect earnings to reach €7.6 billion (and earnings per share of €1.14) by about June 2029, up from €5.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 21.9x on those 2029 earnings, down from 26.1x today. This future PE is greater than the current PE for the GB Electric Utilities industry at 17.9x.

- The bearish analysts expect the number of shares outstanding to grow by 4.93% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.32%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Networks now drive most of Iberdrola's EBITDA, with a 26% increase supported by a 12% rise in the regulated asset base and tariff increases of around 10% in the United States and 8% in Brazil. If this regulated growth trajectory continues under supportive frameworks, it could sustain higher revenue and earnings than implied by a bearish view.

- A record EUR 9 billion of investment in 9 months, 5,500 megawatts under construction and a further 8,500 megawatts of advanced pipeline, including high visibility offshore projects like Vineyard Wind, East Anglia and Baltic Eagle, position Iberdrola to capture long term electrification demand. This could structurally lift revenue and operating margins.

- Strong balance sheet trends, including a 10% increase in operating cash flow to EUR 9,752 million, EUR 8 billion of asset rotation and partnerships, a EUR 3.2 billion reduction in net debt and leverage already below three times EBITDA, may reduce financial risk and funding costs. This could support resilient net profit growth.

- Growing demand from data centers and industry, particularly in the United States where power prices are rising and 30% of the fleet is merchant, creates an opportunity to reprice PPAs at higher levels and expand a 10,000 megawatt portfolio. This could drive stronger long term revenue and earnings than expected.

- Management is guiding to double digit adjusted net profit growth to around EUR 6.6 billion in 2025, already EUR 1 billion above the previous 2026 target, and is backing this with an 8.2% increase in interim dividend. If delivered, this would indicate a sustained positive earnings and cash flow trajectory inconsistent with a prolonged share price decline.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Iberdrola is €17.3, which represents up to two standard deviations below the consensus price target of €19.94. This valuation is based on what can be assumed as the expectations of Iberdrola's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €22.6, and the most bearish reporting a price target of just €17.3.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be €42.7 billion, earnings will come to €7.6 billion, and it would be trading on a PE ratio of 21.9x, assuming you use a discount rate of 7.3%.

- Given the current share price of €21.46, the analyst price target of €17.3 is 24.0% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Iberdrola?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.